Summary

Meyer Blue is a 226-unit, freehold residential development along Meyer Road in Singapore’s East Coast, positioned firmly at the premium end of District 15. It is not a mass-market family project nor a yield-driven investment play. Instead, it targets buyers who value tenure permanence, architectural branding, and long-term asset preservation over price efficiency or short-cycle upside.

The project’s early sales performance demonstrates that demand for ultra-premium freehold homes in the Meyer enclave remains deep, but selective. Buyers who convert tend to be highly intentional, comfortable with high absolute quantum, and less concerned with near-term appreciation. At the same time, price resistance has emerged for larger units as buyers benchmark against both older freehold neighbours and lower-PSF alternatives elsewhere in the Rest of Central Region.

Meyer Blue therefore operates as a filtering project. It rewards buyers who are clear about why they want freehold in this specific coastal belt, and it penalises those expecting momentum-driven gains, broad resale liquidity, or long-term certainty around sea views.

The project sits within the broader context of East Coast transformation and long-term coastal planning, but its investment logic is anchored more in scarcity and holding power than in any single future catalyst.

Meyer Blue is a high-rise freehold development along Meyer Road designed for buyers prioritising long-term tenure security, architectural pedigree, and coastal address prestige over price efficiency, liquidity, or short-term upside.

For buyers assessing whether Meyer Blue aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

Freehold, high-rise residential development along Meyer Road

District 15 (Marine Parade Planning Area), Rest of Central Region

226 units in a single 26-storey tower

Positioned primarily for long-horizon owner-occupiers and legacy-driven buyers

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Meyer Blue |

| Location | 81, 83 Meyer Road |

| District / Region | District 15 / RCR (Marine Parade Planning Area) |

| Tenure | Freehold |

| Developer | UOL Group Limited & Singapore Land Group Limited |

| Site Type | En-bloc redevelopment (former Meyer Park) |

| Development Type | Pure residential |

| Site Area | 8,981.1 sqm (96,672 sq ft) |

| Plot Ratio | 2.8 |

| Total Units | 226 residential units |

| Nearest MRT | Katong Park MRT (TEL), ~0.3 km, walkable |

| Launch Status | Launched |

| Expected TOP | 31 Dec 2028 |

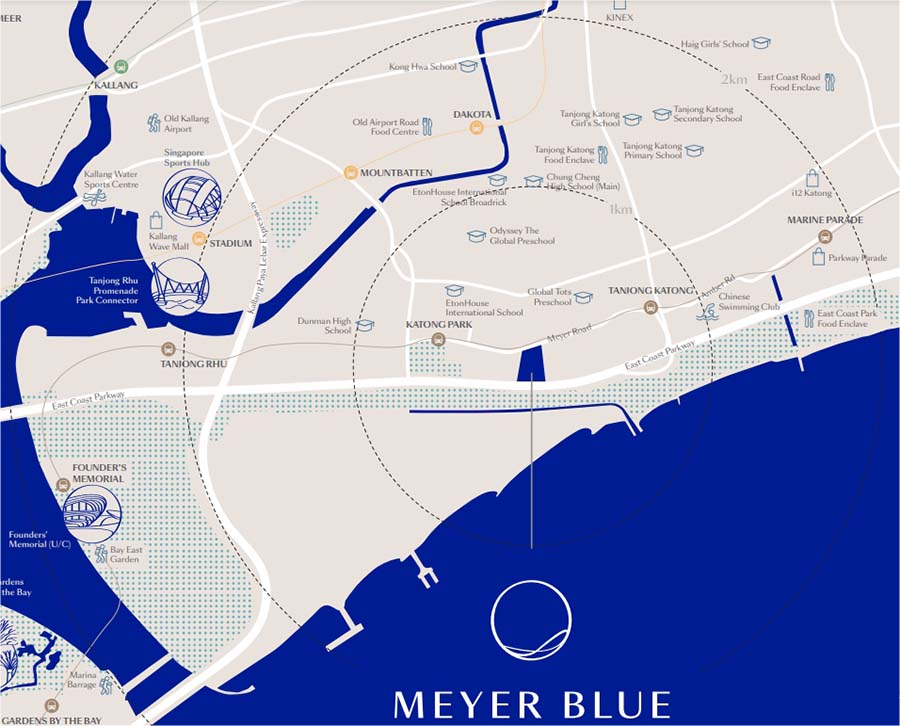

Location Context: Meyer Road as a Legacy Coastal Enclave

Meyer Road occupies a distinctive position within District 15. Unlike lifestyle-centric Katong or Joo Chiat, the Meyer enclave functions as a quiet, low-traffic coastal belt defined by exclusivity rather than vibrancy. Residential developments here are typically large-format, owner-occupied, and oriented toward long-term holding rather than turnover.

Daily convenience is not the primary draw. Amenities such as Parkway Parade, Katong’s dining strip, and Kallang leisure nodes are accessible but not immediately walkable. This shapes the resident profile: buyers tend to be car-owning households, retirees, or high-income professionals who prioritise privacy and address prestige over street-level activity.

Connectivity has improved structurally with the Thomson-East Coast Line. Katong Park MRT provides a direct rail link to the CBD and Orchard corridor, reducing the historic car-dependency of Meyer Road. While this does not transform the area into a transit-oriented lifestyle hub, it materially improves liveability and long-term relevance.

Development Character: High-Rise Density with Luxury Signalling

Meyer Blue is unapologetically vertical.

With 226 units on a 2.8 plot ratio site, the development adopts a high-rise, high-density format relative to some of its low-rise freehold neighbours. This allows the project to deliver elevated sea-facing views and stacked sky greenery, but it also means buyers are trading absolute exclusivity for height, branding, and architectural presence.

The development’s luxury narrative is anchored in three elements: scale, elevation, and design language. High-floor units offer expansive outward views, while the tower configuration enables landscaped sky terraces that reinforce the “coastal high-rise” positioning. This appeals strongly to lifestyle-driven owner-occupiers who value outlook and privacy within their own units more than shared amenity sprawl.

However, higher density also introduces sharper buyer scrutiny. In this price band, buyers are not only comparing tenure and location, but also questioning whether the hardware and internal layouts sufficiently justify the premium over both resale freehold options and newer 99-year launches nearby.

Freehold Logic: Preservation First, Performance Second

Freehold tenure is the cornerstone of Meyer Blue’s positioning.

For buyers planning multi-decade holds, freehold removes lease decay from the equation and provides long-term optionality, particularly relevant in a district dominated by newer 99-year launches. This is the primary reason Meyer Blue is often shortlisted against projects like Tembusu Grand or Grand Dunman, even at significantly higher PSF levels.

However, freehold does not eliminate price sensitivity. At Meyer Blue’s launch pricing, buyers are effectively pre-paying for long-term security. This makes the project less forgiving for those expecting near-term capital appreciation or easy resale liquidity. The trade-off is deliberate: stability and legacy value in exchange for patience.

Greater Southern Waterfront & Long-Island Context: Expectations Must Be Managed

While Meyer Blue benefits from long-term coastal planning narratives, it is not a direct beneficiary of immediate waterfront activation.

The proposed Long Island reclamation introduces both opportunity and risk. Over the very long term, the East Coast is likely to see enhanced coastal protection and new recreational spaces. At the same time, this plan creates uncertainty around view longevity for today’s unblocked sea-facing stacks. Buyers paying a significant premium for southern views must be comfortable with this long-dated ambiguity.

This reinforces a key point: Meyer Blue should be evaluated primarily on its present-day attributes — tenure, design, address — rather than on speculative future transformation.

How Buyers Actually Evaluate Meyer Blue

In practice, buyers rarely assess Meyer Blue in isolation.

One comparison set includes immediate freehold neighbours such as Meyer Mansion or MeyerHouse. These projects offer lower density and, in some cases, lower PSF entry points, but lack the verticality, branding, and scale of facilities that Meyer Blue provides.

Another comparison set comprises new-generation 99-year launches in the broader East Coast and city-fringe. These compete strongly on price efficiency and facilities but lose on tenure and long-term scarcity.

Buyers who convert tend to accept Meyer Blue’s pricing because they are not looking for the “best deal” — they are looking for the “last home” or a long-term family asset.

Buyer Suitability: Who This Project Is — and Is Not — For

Most suitable for

Long-horizon owner-occupiers prioritising freehold tenure

Affluent local families or retirees seeking a quiet coastal address

Buyers comfortable with high absolute quantum and lower liquidity

Least suitable for

Yield-driven or short-cycle investors

Buyers sensitive to PSF comparisons and resale velocity

Those expecting permanent, guaranteed sea views

Buyers comparing Meyer Blue against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Takeaway

Meyer Blue is not a project that needs to be sold — it needs to be understood.

Its value proposition is coherent but narrow: freehold tenure, Meyer Road scarcity, architectural signalling, and long-horizon holding logic. For buyers aligned with these priorities, the pricing can be rationalised as the cost of permanence in a shrinking coastal enclave. For buyers expecting flexibility, momentum, or guaranteed long-term views, the same attributes quickly become friction points.

This is why Meyer Blue functions best as a filtering decision, not a negotiation exercise. If your intent, holding horizon, and tolerance for trade-offs are clear, the project is defensible. If not, it will always feel expensive — regardless of price movement.

If Meyer Blue is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

The questions below reflect how serious, decision-stage buyers typically pressure-test Meyer Blue before deciding whether it belongs on their final shortlist.

FAQs (Decision-Stage)

1) Is Meyer Blue fundamentally an own-stay project or an investment project?

Meyer Blue reads primarily as an own-stay, long-horizon asset. Pricing and quantum naturally filter out yield-led buyers, and the value proposition centres on tenure permanence, address prestige, and holding power rather than short-cycle return. Buyers whose framework is “rentability plus quick exit” will find the project structurally misaligned.

2) What is the real reason buyers pay a premium here — and when does it stop making sense?

The premium reflects the combination of freehold tenure, Meyer Road scarcity, high-rise coastal outlook, and confidence in execution by established developers. It stops making sense when the purchase relies on assumptions outside the buyer’s control, such as permanent sea views or broad future resale demand at the same quantum. In this segment, defensibility matters more than headline PSF.

3) How should buyers think about the Long Island reclamation when paying for sea views today?

Sea-view value here should be treated as time-sensitive rather than permanent. Buyers are paying for present-day openness and lifestyle enjoyment, not a contractual guarantee of an unchanged seafront. Those stretching budgets primarily for view premiums should be comfortable that the value they derive is realised during ownership, not deferred to resale.

4) How material is East Coast Parkway (ECP) noise, and who should be cautious?

For lower-floor or expressway-facing orientations, ECP noise can be a daily-liveability factor rather than a minor trade-off. Stack selection and elevation are therefore core decision variables, not finishing details. Noise-sensitive buyers, including retirees or work-from-home households, should treat orientation as a first-pass filter.

5) Why do buyers benchmark Meyer Blue against older freehold neighbours like Meyer Mansion or MeyerHouse?

The comparison is driven by freehold pedigree and Meyer address credibility rather than price alone. Older neighbours may look cheaper on a PSF basis and offer lower density, but they trade away new-build condition, modern layouts, and full-facility environments. The real choice is between boutique exclusivity and new-build vertical luxury, not simply “old versus new”.

6) Are larger units harder to exit, and what does that imply for long-term liquidity?

High-quantum 4–5 bedroom units naturally face a narrower resale pool, even in prime-facing enclaves, because affordability is not the only filter — buyer intent is. Many capable buyers will still cross-shop landed, older freehold icons with larger floor plates, or alternative districts with stronger lifestyle completeness. The implication is simple: if you buy big here, plan your exit horizon to be patient and unit-specific rather than assuming broad, fast liquidity.

7) Does the single-tower, higher-density format help or hurt at this price point?

It helps buyers who value elevation, outlook, and modern high-rise living that low-rise developments cannot replicate. It hurts buyers equating luxury primarily with low density and exclusivity, where density becomes a key comparison point. The format is coherent, but only for buyers aligned with what high-rise luxury represents.

8) Who should eliminate Meyer Blue early, even if affordability isn’t an issue?

Buyers seeking price efficiency, quick resale liquidity, or certainty around permanent sea views should step away early. The project is also unsuitable for those relying on broad mass-market resale demand at high quantum. Meyer Blue rewards conviction and long holding horizons, not flexibility or momentum-driven strategies.

PRICING LOGIC, URA PLANNING INTENT & BUYER SEGMENTATION

Pricing Logic: Why Meyer Blue Clears Early — Then Slows

Meyer Blue’s pricing behaviour reflects a two-phase pattern: conviction-led absorption followed by selective resistance. Early buyers accepted high absolute quantum in exchange for freehold tenure, Meyer Road scarcity, and long-horizon asset defensibility. As this cohort was absorbed, subsequent demand became narrower, more unit-specific, and increasingly comparative.

At this stage, Meyer Blue is most often benchmarked against two reference sets:

older freehold neighbours offering lower entry PSF but less new-build clarity, and

newer 99-year launches that provide stronger lifestyle completeness at lower absolute quantum.

This transition marks the natural resistance zone for premium freehold projects. Sales velocity slows not because pricing is indefensible, but because the number of buyers willing to pay for this exact combination of tenure, address, and trade-offs declines sharply once early conviction demand is satisfied.

Launch vs Balance Pricing: What Actually Changes

Launch pricing at Meyer Blue established the project as a top-tier freehold benchmark within District 15 rather than a value-led alternative. Early buyers were effectively paying for certainty — in unit choice, orientation, and long-term holding logic — rather than short-term pricing advantage.

Balance units are evaluated differently. Buyer scrutiny shifts toward:

orientation and expressway noise exposure,

long-term view assumptions tied to coastal planning, and

exit realism at high absolute prices.

As a result, pricing discussions are less about headline PSF and more about whether a specific unit still makes sense relative to the buyer’s holding horizon. Negotiation leverage exists, but it is unit-specific rather than project-wide.

URA Planning Intent: East Coast as Stability, Not a Catalyst

URA planning intent for the Marine Parade Planning Area supports long-term residential stability rather than near-term repricing. Infrastructure upgrades and coastal adaptation initiatives improve liveability and long-term defensibility, but they are not designed to function as investment catalysts.

The area is being shaped around improved connectivity, aging-in-place infrastructure, and incremental quality-of-life upgrades. These changes reinforce residential relevance over time, but they do not introduce discrete events that typically drive sharp repricing.

The proposed Long Island project further reinforces this dynamic. While it enhances long-term coastal resilience and recreational potential, it also introduces uncertainty around future seafront configuration and view permanence. Planning intent here is defensive and adaptive, not speculative.

For Meyer Blue, this means URA context supports preservation rather than acceleration. Long-term value is anchored more to tenure and scarcity than to neighbourhood transformation.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: Long-Horizon Owner-Occupiers

These buyers prioritise freehold tenure, coastal address prestige, and modern living conditions. They are less sensitive to short-term price movements and more focused on whether the home remains suitable across decades. Conversion is driven by alignment rather than urgency.

Secondary Segment: Capital-Preservation Buyers

This group views Meyer Blue as a defensive asset. They accept lower liquidity and modest rental yields in exchange for tenure certainty and long-term optionality. Their concern is downside protection, not outperformance.

Marginal Segment: High-Quantum Upgraders

Upgraders from other prime districts or landed homes evaluate Meyer Blue opportunistically. They convert only when a specific unit aligns with their spatial preferences, noise tolerance, and orientation requirements. This group contributes to intermittent sales rather than sustained momentum.

Largely Absent Segment

Yield-led investors and short-cycle traders are structurally filtered out. Pricing, quantum, and long-dated uncertainty around views make Meyer Blue unsuitable for strategies dependent on fast exits or rental yield optimisation.

EXIT, LIQUIDITY, RISK SCENARIOS & LONG-TERM REALISM

Exit Behaviour: Why Liquidity Is Unit-Specific, Not Project-Wide

Exit behaviour at Meyer Blue is unit-specific rather than project-wide. Liquidity depends on alignment between unit attributes, buyer intent, and holding horizon rather than general market momentum. Freehold tenure supports long-term defensibility, but it does not eliminate time-to-exit risk at high quantum levels.

In early post-TOP years, resale demand is anchored by new-build clarity and limited direct competition. Over the mid-cycle, exit outcomes diverge sharply based on unit attributes. Over the long term, freehold tenure becomes more relevant as leasehold alternatives age, improving structural defensibility but not transaction speed.

Smaller units with favourable orientation are likely to transact more smoothly. Larger units — particularly those affected by noise or view uncertainty — will require patience and realistic pricing expectations.

Time-Phased Exit Scenarios

Early Post-TOP Phase

Limited direct competition from new freehold launches

Buyer interest anchored in new-build condition and clarity

Exit viability strongest for mid-sized units

Mid-Cycle Phase

Increased competition from newer launches in other districts

Buyers become more comparative and value-conscious

Exit outcomes diverge sharply by unit attributes

Long-Term Phase

Freehold advantage becomes more salient as leasehold projects age

Buyer focus shifts toward tenure security and legacy considerations

Liquidity improves structurally, but remains selective

Risk Scenarios Buyers Must Acknowledge

View Longevity Risk

Southern-facing premiums are vulnerable to long-term coastal reconfiguration. This does not invalidate the purchase, but reframes the proposition as use-value first and resale optionality second.

Noise & Liveability Risk

Expressway adjacency is permanent. Units affected by ambient noise will always face a narrower buyer pool, regardless of market cycle.

Quantum Compression Risk

High absolute prices reduce buyer flexibility during resale, particularly in tighter credit environments. This risk manifests as longer holding periods rather than forced repricing.

Policy & Macro Sensitivity

Higher interest rates disproportionately affect high-quantum assets with moderate yields. While this limits speculative volatility, it slows transactional velocity.

Freehold Reality Check: Protection, Not Acceleration

Freehold tenure at Meyer Blue functions as a risk-mitigation attribute rather than a performance driver. It protects against lease decay and supports long-term relevance, but it does not override buyer sensitivity to price, layout efficiency, and liveability.

Buyers who approach Meyer Blue with a use-first mindset are more likely to remain satisfied across cycles. Those expecting tenure alone to drive appreciation are likely to face expectation mismatch.

FAQs

1) How should buyers model resale risk if market conditions soften materially?

Resale risk at Meyer Blue is more about time than price. In softer markets, sellers may need to wait longer rather than cut aggressively, especially for high-quantum units. Buyers should model holding flexibility rather than relying on market recovery to solve exit timing.

2) Does freehold materially widen the future buyer pool at resale?

Over long horizons, yes — but not immediately. Freehold matters most when leasehold alternatives begin facing perceptual decay, which is a gradual process. In the near term, buyer selection remains driven by affordability, unit attributes, and lifestyle fit.

3) Are larger units structurally disadvantaged compared to smaller ones?

They are more sensitive to buyer pool depth, not inherently inferior. Larger units compete not only with other condos, but with landed homes and older freehold icons. Exit success depends heavily on orientation, layout efficiency, and realistic pricing.

4) How does Meyer Blue behave in comparison to older freehold resale stock during downturns?

Older freehold projects may transact more easily at lower price points, while Meyer Blue relies on scarcity and new-build clarity. This can make resale volumes lower but pricing more stable. The trade-off is patience versus price volatility.

5) Is rental a viable holding strategy if resale conditions are weak?

Rental can function as a holding buffer, but not a yield-maximisation strategy. Rental demand exists due to location and prestige, but yields may not fully offset financing costs at high entry prices. Rental works best as a defensive option.

6) How sensitive is Meyer Blue to changes in buyer sentiment around coastal planning?

Sentiment shifts can influence perception of view value, but they rarely trigger immediate repricing. The impact is more subtle, affecting buyer hesitation and negotiation behaviour rather than causing sharp corrections.

7) What distinguishes a “good” exit unit from a “difficult” one in this project?

Orientation, elevation, and noise exposure matter more than floor area alone. Units that minimise permanent trade-offs while preserving liveability will always outperform others at resale. Unit selection is a risk-management decision, not a cosmetic one.

8) Does Meyer Blue become more or less attractive as the project ages?

Attractiveness shifts from “new-build appeal” to “tenure defensibility”. While newer projects will compete on facilities and novelty, Meyer Blue’s freehold status and Meyer Road address gain relative importance over time.

9) How should buyers think about opportunity cost versus other districts?

Buying Meyer Blue means concentrating capital into a single, high-quality asset rather than spreading exposure. This suits buyers who value certainty and permanence over flexibility. Opportunity cost is real, but acceptable for aligned buyers.

10) Is Meyer Blue suitable for portfolio diversification?

Only as a stabilising component, not a return driver. It complements growth-oriented assets by providing tenure security and lower long-term obsolescence risk. It is less effective as a standalone performance play.

11) What happens if future launches nearby undercut pricing?

Short-term sentiment may soften, but undercutting does not negate Meyer Blue’s tenure advantage. The impact is more likely to appear in longer selling periods rather than sharp price drops, especially for well-selected units.

12) How important is financing structure in managing long-term risk here?

Extremely important. Buyers with lower leverage enjoy far more flexibility in both holding and exit decisions. High leverage amplifies time pressure, which is the primary risk in selective-liquidity projects like Meyer Blue.

13) Does Meyer Blue rely too heavily on branding and developer reputation?

Reputation reduces execution risk but does not replace buyer diligence. Branding supports confidence, not resale guarantees. Buyers should treat it as a risk reducer, not a value creator.

14) How should buyers stress-test their own decision before committing?

By asking whether they would still be comfortable owning the unit if resale takes years rather than months. If the answer is yes, the project is likely aligned. If not, the mismatch will surface quickly during ownership.

15) Is Meyer Blue a “safe” buy in absolute terms?

It is safe only for buyers whose expectations align with long holding horizons and selective liquidity. Safety here means stability and defensibility, not performance or flexibility.

16) Who should walk away, even late in the decision process?

Buyers relying on future transformation, guaranteed views, or fast resale should exit early. Meyer Blue rewards clarity and patience; it penalises uncertainty and short-term thinking.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.