Summary

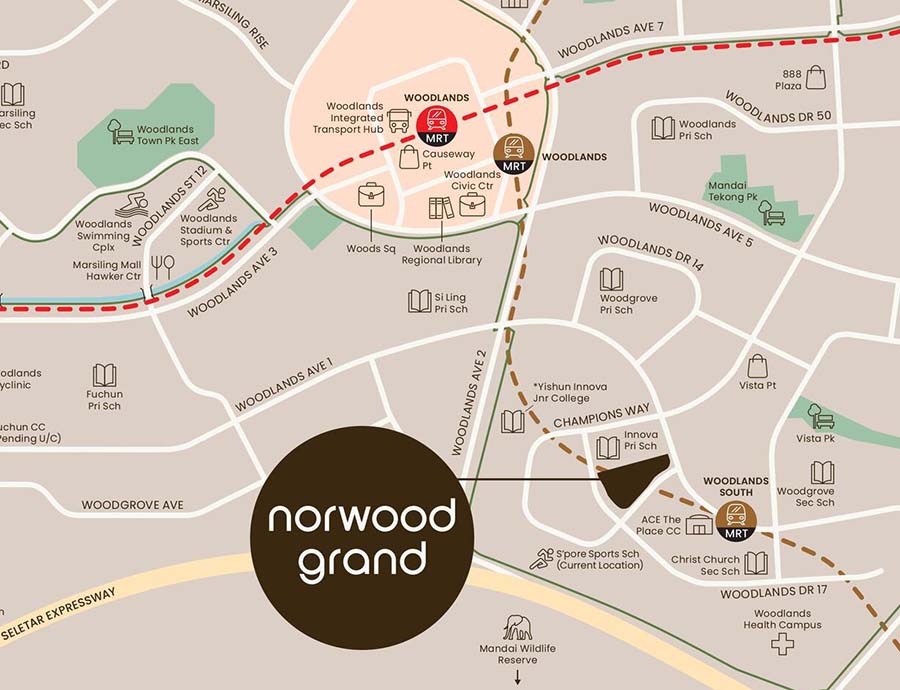

Norwood Grand is a 99-year leasehold condominium located at Champions Way in District 25, positioned as an MRT-linked private development within the Woodlands Regional Centre.

It is best understood as a transport-driven, employment-supported residential project rather than a lifestyle-led condominium. Its value is anchored in direct access to Woodlands South MRT (Thomson–East Coast Line), proximity to Woodlands Health Campus, and limited new private supply within a mature northern HDB catchment.

Pricing at Norwood Grand is supported by MRT adjacency rather than neighbourhood prestige, which creates strong demand for smaller and mid-sized units but more selective absorption for larger, higher-quantum units.

The project is most suitable for North-based HDB upgraders, healthcare professionals, and buyers prioritising commuting efficiency and long-term residential stability. It is less aligned with investors seeking short-term gains, buyers focused on psf-based value comparisons, or those prioritising low-density living.

From an investment perspective, Norwood Grand functions as a defensive, long-hold asset supported by transport accessibility and employment proximity, rather than a growth-driven or speculative opportunity.

Overall, Norwood Grand is a location-conviction project. Buyers aligned with MRT access and regional employment stability are likely to find it coherent, while those driven by lifestyle appeal, pricing optics, or rapid capital appreciation may face misalignment.

Norwood Grand is an MRT-linked OCR condominium tailored for North-rooted families and professionals who prioritise transport certainty and employment proximity over lifestyle scale or density minimisation.

Explore the Full Norwood Grand Analysis

This article is part of the full Norwood Grand cluster:

- Norwood Grand Price Guide – pricing structure, market positioning, and buyer entry analysis

- Norwood Grand Floor Plan Analysis – layout efficiency, unit mix, and stack considerations

- Norwood Grand Showflat Guide – viewing strategy, location context, and buyer evaluation framework

Together, these articles provide a structured analysis of the project’s positioning, pricing framework, lay

If you’re considering this project, you might want to check how it actually compares and what most buyers tend to overlook — before deciding.

Key Details (At a Glance)

-

99-year leasehold private condominium

-

Champions Way, District 25 (Woodlands Planning Area)

-

Outside Central Region (OCR)

-

MRT-adjacent development anchored by the Thomson–East Coast Line

-

Positioned primarily for HDB upgraders and employment-linked owner-occupiers

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Norwood Grand |

| Location | 2, 6, 8 and 10 Champions Way |

| District / Region | District 25 / Outside Central Region (Woodlands Planning Area) |

| Tenure | 99 years leasehold (commencing 18 December 2023) |

| Site Type | GLS (Government Land Sale) |

| Developer | CDL Stellar Pte. Ltd. (wholly-owned subsidiary of City Developments Limited) |

| Development Type | Pure residential with Early Childhood Development Centre (ECDC) |

| Site Area | 14,432.5 sqm |

| Plot Ratio | 2.1 |

| Total Units | 348 residential units |

| Unit Mix | 1- to 4-bedroom variants with study configurations |

| Nearest MRT | Woodlands South MRT (Thomson–East Coast Line) — walk access |

| Expected TOP | 31 March 2030 |

Location Context: Woodlands as a Regional, Not Peripheral, Market

Woodlands has evolved from a self-contained heartland into a designated regional centre with cross-border and employment functions. The area’s planning intent focuses on decentralisation—bringing jobs, transport nodes, and public infrastructure closer to residents rather than relying on city-centric commuting patterns.

Norwood Grand’s immediate catchment reflects this shift. Woodlands South MRT provides direct rail connectivity without transfers, while the adjacent Woodlands Health Campus introduces a stable, professional employment base that supports both owner-occupation and rental demand. This combination reduces reliance on speculative narratives and instead grounds demand in daily utility.

However, Woodlands remains a functional environment rather than a lifestyle precinct. Retail and dining options are clustered rather than street-activated, and the neighbourhood’s rhythm is shaped more by institutional and residential use than by destination appeal. Buyers should therefore frame the location as efficient and purposeful, not experiential.

Development Character & Site Structure

Norwood Grand is organised across four 11-storey residential blocks on a relatively compact GLS site. The planning emphasis is on efficient internal circulation and clear zoning rather than expansive resort-style grounds. Density is perceptible, particularly during peak usage periods, and forms part of the project’s inherent trade-off.

The inclusion of an Early Childhood Development Centre signals family orientation and practical liveability, but also reinforces the project’s utilitarian positioning. This is not a development designed to impress through scale; it is designed to function well for a specific demographic.

Pricing Logic: Acceptance Built on Access, Not Optics

Buyer acceptance at Norwood Grand has been driven primarily by access logic rather than price optics. MRT adjacency within Woodlands compresses the traditional “distance discount” associated with OCR projects, allowing pricing to hold at levels that would otherwise face stronger resistance in non-transit-linked locations.

This resistance is structural rather than cyclical, and typically persists regardless of broader market conditions. At higher absolute prices, buyers begin comparing against future EC supply and older resale options, rather than against other private launches. This creates a natural filtering effect: smaller and mid-sized units clear more smoothly, while larger units require stronger conviction in location and holding horizon.

The result is selective absorption rather than broad-based momentum—consistent with a project that prioritises functional demand over aspirational pull.

For most buyers, the decision is not whether Norwood Grand is priced attractively for Woodlands, but whether MRT access justifies stepping above typical OCR expectations

What Norwood Grand Is — and Is Not

What It Is

-

An MRT-adjacent private condominium in a mature northern estate

-

A demand-absorbing project for HDB upgraders who want to stay in Woodlands

-

Anchored by employment proximity and transport certainty

-

Structured for long-term occupancy rather than short-cycle trading

What It Is Not

-

Not a low-density or lifestyle-led development

-

Not a value-driven OCR bargain

-

Not positioned for rapid repricing or speculative exits

-

Not designed to compete with integrated or waterfront projects

Clarity on this distinction is essential to avoiding expectation mismatch.

Amenities & Facilities: What You Actually Get

Norwood Grand’s facilities are designed around functional daily use rather than expansive resort-style living.

The development includes a standard suite of condominium amenities such as a swimming pool, gymnasium, landscaped gardens, and communal spaces for relaxation and social interaction. These facilities are distributed efficiently across the site to support a 348-unit population within a compact layout.

An Early Childhood Development Centre (ECDC) is integrated within the development, reinforcing its positioning toward young families and practical, day-to-day convenience rather than lifestyle-driven living.

However, the facilities offering is not extensive when compared to larger OCR developments. The emphasis is on usability and accessibility rather than scale or thematic design.

For buyers, this translates into:

- Sufficient facilities for daily living

- Functional communal spaces rather than resort-style experience

- Higher utilisation during peak periods due to density

This aligns with the project’s broader positioning — practical, efficient, and infrastructure-driven rather than lifestyle-centric.

Buyer Suitability: Who This Project Works For

Most Suitable For

-

HDB upgraders from Woodlands and nearby northern estates

-

Professionals working at or near the Woodlands Health Campus

-

Buyers who prioritise MRT access and commuting certainty

-

Households planning medium- to long-term occupation

Least Suitable For

-

Buyers seeking low density and expansive facilities

-

Value-driven purchasers comparing strictly on psf metrics

-

Those eligible for and willing to wait for future EC supply

-

Investors targeting short-term liquidity or yield maximisation

Buyers comparing Norwood Grand against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Takeaway

Norwood Grand is not a project that wins on charm or spectacle—it wins on utility and alignment. Its success depends on buyers who understand Woodlands as a regional node rather than a peripheral compromise, and who value access certainty over lifestyle optionality.

For the right buyer, the proposition is coherent and defensible. For the wrong buyer, density, pricing psychology, and upcoming EC competition will feel like persistent friction rather than temporary issues.

If you’re seriously considering this project, it’s worth checking how it actually compares and what most buyers tend to overlook — before deciding.

FAQs (Decision-Stage)

1) Is Norwood Grand worth buying?

Norwood Grand may be worth buying for buyers who prioritise MRT access, commuting efficiency and long-term residential stability in Woodlands. It is less suitable for those seeking lifestyle-driven environments or short-term capital appreciation.

2) Is Norwood Grand a good investment property?

Norwood Grand functions more as a defensive, long-term investment property rather than a high-growth or short-term opportunity. Its value is supported by MRT proximity and employment demand, but price appreciation is expected to be gradual rather than rapid.

3) Who is Norwood Grand most suitable for?

Norwood Grand is most suitable for North-based HDB upgraders, healthcare professionals working nearby, and buyers who prioritise transport connectivity and daily convenience.

4) Why is Norwood Grand priced higher than typical OCR condos?

Norwood Grand pricing is supported by MRT adjacency, which reduces the typical “distance discount” associated with OCR projects. Buyers are effectively paying for transport access rather than neighbourhood prestige.

5) Is Norwood Grand considered expensive?

Norwood Grand sits at the higher end of OCR pricing expectations due to its MRT-linked positioning. Price acceptance is driven by access and convenience rather than value perception alone.

6) Is Norwood Grand suitable for families?

Norwood Grand can support families, particularly those prioritising proximity to schools and healthcare facilities. However, density and layout constraints mean it may not suit buyers seeking spacious, low-density environments.

7) What are the main risks of buying Norwood Grand?

Key risks include density perception, competition from future EC supply, and pricing sensitivity for larger units. These factors affect resale dynamics more than rental demand.

8) Why do buyers choose Norwood Grand?

Buyers typically choose Norwood Grand for its MRT access, proximity to employment hubs, and ability to stay within the Woodlands area while upgrading to private housing.

Is Norwood Grand Worth Buying? (Decision Overview)

Norwood Grand is worth considering for buyers who prioritise MRT connectivity, employment proximity, and long-term residential stability within Woodlands.

It is less suitable for buyers focused on low-density living, lifestyle environments, or short-term investment returns.

The decision ultimately depends on whether transport convenience and location familiarity outweigh density, pricing perception, and future EC competition.

Pricing Logic, URA Planning Intent & Buyer Segmentation

Pricing Logic: Why Acceptance Is Location-Led, Not Value-Led

Norwood Grand’s pricing behaviour reflects a classic MRT-led OCR pattern rather than a lifestyle-driven one. Buyers who convert are typically less focused on whether the project is “cheap for OCR” and more focused on what the location removes from daily friction—namely long commute times and transfer dependency.

At lower absolute price points, smaller and mid-sized units clear more smoothly because the MRT adjacency compresses the psychological distance penalty traditionally associated with District 25. Buyers compare Norwood Grand less against older Woodlands resale condos and more against city-fringe projects that lack direct rail access. In this context, price acceptance is anchored to access equivalence, not neighbourhood prestige.

Resistance emerges as unit sizes and quantums increase. When larger units cross certain affordability thresholds, buyers begin comparing against future EC options or delaying decisions in anticipation of lower-entry alternatives. This resistance is structural, not cyclical, and explains why absorption slows naturally toward the larger-format inventory.

OCR Pricing Psychology: Where the Ceiling Actually Forms

The key psychological ceiling for Norwood Grand is not psf-based, but quantum-based. Buyers may accept higher psf figures when absolute prices remain manageable, but hesitation increases sharply once total price comparisons shift toward EC or resale landed logic.

This creates a segmented demand curve:

-

Smaller units benefit from strong upgrader demand and tenant logic tied to MRT access.

-

Larger units require buyers with higher income certainty, lower leverage dependence, and stronger conviction in Woodlands as a long-term base.

As a result, pricing stability is stronger at the lower and mid tiers, while larger units rely more heavily on alignment rather than market momentum. This is typical of infrastructure-led OCR projects and does not indicate fundamental weakness.

URA Planning Intent: Woodlands as a Regional Centre, Not a Satellite Town

URA’s planning intent for Woodlands is central to understanding Norwood Grand’s long-term positioning. Woodlands is being structured as a regional employment and transport hub, designed to decentralise jobs and reduce reliance on the city core rather than act as a dormitory town.

This intent supports Norwood Grand indirectly. Proximity to employment nodes, healthcare infrastructure, and cross-border connectivity enhances residential relevance over time. However, URA planning does not aim to transform Woodlands into a lifestyle or leisure destination comparable to waterfront or heritage districts.

For buyers, this distinction matters. URA intent here strengthens defensibility and utility, not aspirational uplift. Buyers expecting visible transformation at street level may find progress gradual, while those prioritising functional relevance benefit more consistently.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: North-Rooted HDB Upgraders

These buyers form the core demand base. They prioritise staying near family networks, schools, and familiar amenities, while upgrading status and comfort. MRT access significantly reduces compromise for this group.

Secondary Segment: Employment-Linked Professionals

Healthcare professionals and institutional workers value proximity and commute predictability. Their decisions are pragmatic, with limited emphasis on facilities or prestige. This segment supports rental stability rather than aggressive pricing.

Tertiary Segment: Infrastructure-Driven Holders

These buyers believe in Woodlands’ long-term regional role. They are less sensitive to short-term price optics but more patient with holding horizons. Their numbers are smaller but conviction-driven.

Absent Segments

Short-term traders, lifestyle-led buyers, and density-sensitive purchasers tend to self-filter out early. Their absence explains why sales are strong yet selective rather than euphoric.

Exit, Liquidity & Risk Scenarios

Exit Liquidity: Why MRT Access Matters — but Doesn’t Solve Everything

Norwood Grand’s resale liquidity will be structurally stronger than non-MRT-linked Woodlands projects. Walkable MRT access consistently widens buyer pools and shortens decision cycles, especially for owner-occupiers and tenants. Liquidity advantage exists, but it is uneven across unit types rather than uniform across the development.

However, MRT adjacency does not eliminate all liquidity friction. Unit size, total price, and future competing supply still shape exit outcomes. Smaller units are likely to transact more regularly, while larger units may experience longer holding periods during softer market phases.

Liquidity here is asymmetric by unit type, not uniform across the project.

Time-Phased Exit Scenarios

Early Post-TOP Phase (0–3 Years)

-

Competition primarily internal and from nearby resale stock

-

Exit strongest for smaller and mid-sized units

-

Pricing anchored by new-build condition and access convenience

Mid-Cycle Phase (3–8 Years)

-

Increased competition from newer northern projects and ECs

-

Buyers focus more on price realism and liveability

-

Exit outcomes become unit-specific rather than project-wide

Long-Term Phase (8+ Years)

-

MRT adjacency becomes increasingly valuable

-

Leasehold perception begins to matter more relative to older stock

- Exit favours buyers aligned with Woodlands’ regional employment role

Exit outcomes are therefore driven more by unit selection and holding period than by project-level momentum.

Structural Risks Buyers Must Accept

These risks are structural and should be accepted upfront rather than evaluated after purchase.

1) Density Perception Risk

The site’s compactness creates noticeable density during peak usage. This is permanent and should be priced into expectations rather than dismissed as temporary.

2) EC Competition Risk

Future EC launches may divert upgrader demand, particularly for price-sensitive families. While EC eligibility constraints limit overlap, psychological comparison remains a real friction.

3) Quantum Sensitivity for Larger Units

Higher absolute prices narrow the buyer pool and lengthen exit timelines. This affects liquidity more than valuation.

4) Noise and Adjacency Exposure

Proximity to roads, schools, and activity zones introduces environmental noise for certain stacks. These factors are structural and unit-specific.

5) Infrastructure Timing Risk

Infrastructure narratives support long-term relevance but rarely translate into immediate resale premiums. Buyers relying on event-driven uplift may face disappointment.

Investment Reality: Defence Over Acceleration

Norwood Grand functions better as a defensive residential asset than an acceleration play. MRT access and employment proximity provide demand resilience, but price appreciation is likely to be steady rather than explosive.

Rental demand exists, particularly from employment-linked tenants, but yields should be treated as a holding buffer rather than a return driver. Leverage-heavy strategies are more exposed to holding pressure, particularly during slower transaction cycles.

For most buyers, the project works best when expectations are anchored to stability, not outperformance. This is a project where stability comes from usage-driven demand rather than market timing.

Who This Works For

Buyers prioritising MRT access, daily convenience, and long-term residential stability will find Norwood Grand aligned with their needs.

Those seeking low-density living, lifestyle positioning, or rapid capital upside should consider alternatives.

Final Assessment

Norwood Grand behaves exactly as an MRT-anchored OCR project should.

It absorbs pent-up northern upgrader demand efficiently, filters out misaligned buyers early, and anchors value to access and employment rather than lifestyle appeal. Buyers who understand Woodlands as a regional centre—not a peripheral compromise—are more likely to find long-term satisfaction.

This is not a project that rewards optimism or timing. It rewards alignment, patience, and clarity of intent.

Buyers who understand what Norwood Grand is—and just as importantly what it is not—are far more likely to experience a stable and satisfactory outcome.”

FAQs (Deep Decision-Stage Analysis)

1) Will Norwood Grand face strong resale competition in the future?

Yes. Future Executive Condominium (EC) launches and nearby residential supply in Woodlands may introduce competition, particularly for price-sensitive upgrader buyers. While EC eligibility rules limit direct substitution, the psychological comparison remains significant. This tends to affect larger units more than smaller ones due to overlapping quantum ranges.

2) How does Norwood Grand compare to other OCR condos in Singapore?

Norwood Grand differs from typical OCR condos by being MRT-adjacent, which reduces the usual location disadvantage associated with suburban projects. However, it does not compete on lifestyle, density or prestige factors. Buyers are effectively trading off environment for transport efficiency and employment proximity.

3) Is Norwood Grand’s pricing justified by its location?

Pricing is primarily supported by MRT access and proximity to the Woodlands Regional Centre. While this improves demand resilience, it does not fully eliminate price sensitivity associated with OCR locations. Buyers still benchmark against ECs and resale alternatives, particularly at higher quantum levels.

4) Which unit types are likely to have better resale demand?

Smaller and mid-sized units typically have stronger resale demand due to lower entry price and broader buyer pool. Larger units tend to face more limited demand due to higher quantum and competition from ECs or resale options. Liquidity is therefore uneven across unit types rather than uniform across the project.

5) How important is unit selection at Norwood Grand?

Unit selection is critical due to density, site layout and surrounding environment. Factors such as facing, proximity to roads, and internal layout efficiency can significantly impact both liveability and resale performance. Not all units within the same project will perform equally over time.

6) Will rental demand be strong for Norwood Grand?

Rental demand is expected to be supported by proximity to Woodlands Health Campus and MRT connectivity. However, rental yields may remain moderate due to relatively higher entry pricing. The project works more as a rental-supported asset rather than a yield-maximisation investment.

7) What type of tenant profile is Norwood Grand likely to attract?

Norwood Grand is likely to attract healthcare professionals, working professionals and tenants prioritising convenience and commute efficiency. It is less likely to attract family tenants seeking space or school-centric living environments. Tenant demand is therefore functional rather than lifestyle-driven.

8) How does MRT proximity affect long-term value?

MRT proximity improves demand consistency, resale liquidity and tenant appeal over time. However, it does not guarantee price growth or eliminate market cycles. It should be viewed as a stabilising factor rather than a growth accelerator.

9) Will Norwood Grand benefit from Woodlands’ URA transformation?

Woodlands’ development as a regional centre supports long-term residential relevance and employment demand. However, the benefits are gradual and structural rather than immediate. Buyers should not expect rapid price uplift purely from transformation plans.

10) Is Norwood Grand more suitable for holding or short-term exit?

Norwood Grand is more suited for medium to long-term holding strategies. Short-term exit may be challenging due to pricing sensitivity and competing supply. Buyers who enter with longer holding horizons tend to align better with the project’s positioning.

11) What are the key exit risks buyers should consider?

Key exit risks include EC competition, pricing sensitivity at higher quantum, and buyer perception of Woodlands as an OCR location. These factors affect liquidity and resale timelines more than absolute price levels. Exit outcomes depend heavily on unit type and holding period.

12) How does Norwood Grand compare to integrated developments?

Norwood Grand is not an integrated development and does not offer direct retail or transport integration beyond MRT access. Compared to integrated projects, it offers less convenience layering but remains functionally strong due to transport connectivity. Buyer expectations should be adjusted accordingly.

13) Is Norwood Grand affected by surrounding environment factors?

Yes. Surrounding roads, institutional buildings and urban density influence liveability and perception. These factors vary depending on stack and orientation. Buyers should assess unit-specific conditions rather than rely on project-level assumptions.

14) Will Norwood Grand appeal to future resale buyers?

Norwood Grand is likely to appeal to buyers prioritising MRT access, convenience and Woodlands familiarity. However, it may be less attractive to buyers seeking exclusivity, low density or lifestyle-driven environments. Appeal is therefore segment-specific rather than broad-based.

15) How does Norwood Grand perform in long-term positioning?

Norwood Grand’s long-term positioning is supported by transport infrastructure and regional employment growth. Its performance depends on sustained demand rather than speculative drivers. It functions as a stability-led asset rather than a high-growth opportunity.

16) What is the biggest mistake buyers make when evaluating Norwood Grand?

The most common mistake is evaluating the project purely on price or psf without considering buyer pool depth and exit dynamics. Understanding who the next buyer is becomes critical for long-term performance. Misalignment typically leads to slower resale rather than outright loss.

If you prefer a more structured walkthrough, you can leave your details below and we’ll follow up with you.