Loan Limit and Maximum Tenure

The loan limit and tenure in Singapore is based on a few factors

- Type of Property Purchase

- Number of Outstanding Mortgage Loan

- When you are an individual or a company

- Loan period

- Age of Borrower after full repayment

- Total Debt Servicing Ratio

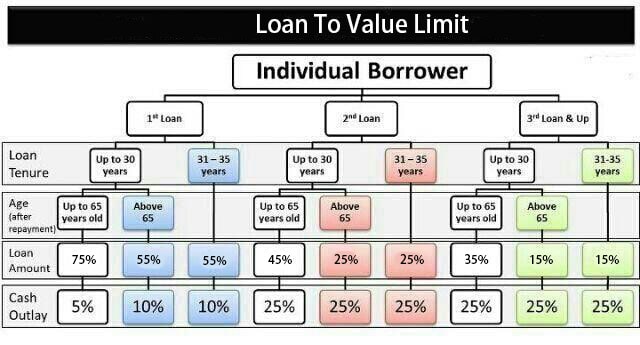

Loan to Value Limit

Loan to value limit is the maximum loan amount you can get from any financial institution.

Loan to Value Limit for Commercial & Industrial Property

Generally, the typically loan to value limit for commercial and industrial property is 75% for own occupancy and 65% for for investment purposes and is applicable for both individuals and companies. The LTV limit is unlikely to exceed more than 75%.

Loan to Value Limit for Private Residential Property (excluding Executive Condominium)

Loan to Value limit will have to depend on the loan tenure, borrower’s age after full repayment, number of outstanding housing loans and when if the borrower is an individual or company. Note that the cash outlay or minimum cash to come up with upon purchasing is also affected by these factors.

For Company and Non-Individual Borrowers

The maximum Loan to Value limit is 15% regardless of any outstanding mortgage.

For Individuals

The below chart gives a simplify and overview of the Loan to Value Limit and Cash Outlay.

Total Debt Servicing Ratio (TDSR) and Income Weighted Average Age

Other than the LTV limit, the loan limit and tenure will also be bounded by the TDSR framework and Income Weighted Average Age (Assuming there are more than 1 borrower on the same property).

TDSR Calculation

This measure states that property loans cannot exceed more than 55% of the TDSR. This framework will use the following to calculate the total loan eligible for borrowers.

- 55% of the total fixed income (for variable there will be a haircut of 30%, meaning 38.5% of the variable income)

- This will then minus of any outstanding mthly installment such as credit card payment, car loan, personal loan, outstanding mortgage, etc.

- The remaining amount will then be used to calculate the maximum mortgage loan using the prevailing market interest rate or 3.5% for residential property loan and 4% for commercial property loan, whichever is higher.

- The eligible loan limit will then be the lower limit between the TDSR calculation and LTV limit.

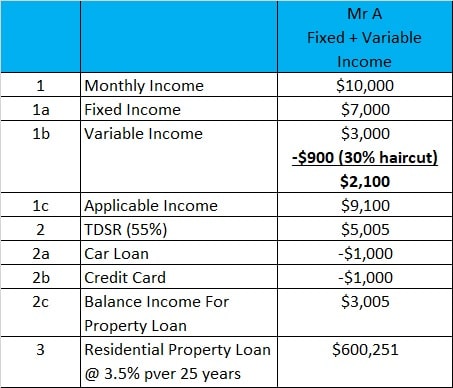

A simple illustration:

Assuming Mr. A is a 1st timer property buyer without outstanding loan. He wants to buy a private property at $1,000,000. According to the LTV limit, his loan amount will be $750,000 (75% of purchase price). And since Mr A is 40 years old and his maximum loan tenure will be 25 years old.

Currently Mr. A draws a gross monthly income of $10,000 which $7,000 is fixed and $3,000 is variable e.g. commission. He is currently servicing a car loan of $1,000 and credit card bill of $1,000 monthly.

The TDSR calculation will be as below:

Given the above, Mr. A will only be eligible to a loan amount of $600,251 instead of $750,000.

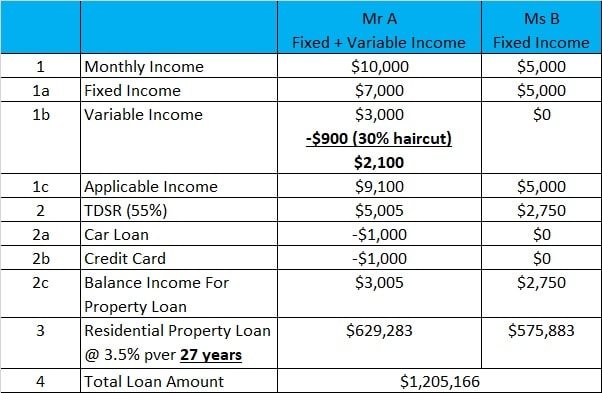

Income Weighted Average Age

Mr. A wishes to purchase with Ms. B who is 22 years old and earning a fixed monthly income of $1,000. The maximum loan tenure for them will be:

The maximum loan tenure for Mr. A and Ms. B for their property loan will be 65 – 38 = 27 years. Ms. B is also a 1st timer property buyer and she does not have any other loan. Their TDSR calculation will be:

Mr. A and Ms. B are eligible for a loan amount up to $1,205,166 and their maximum loan tenure will be 27 years.

Loan Limit for Executive Condominium

- For joint borrowing, the Income Weighted Average Age still applies.

- Buyers can only used up to 30% of their total gross monthly income to service their mortgage which is called the Mortgage Service Ratio (MSR).

- A medium term 3.5% interest in used to calculated the loan limit

- TDSR still apply. Loan amount will be granted based on the lower one calculated by MSR and TDSR.

Example:

- Mr A and Ms B has a total gross monthly income of $10,000; MSR @ 30% i.e. a maximum of $3,000 to service their loan.

- Their Income Weighted Average Age is 40 years old. Therefore maximum loan tenure is 25 years.

- Using 3.5% rate to calculate; their total maximum loan limit will be $599,252 or 75% of the purchase price, whichever is lower.

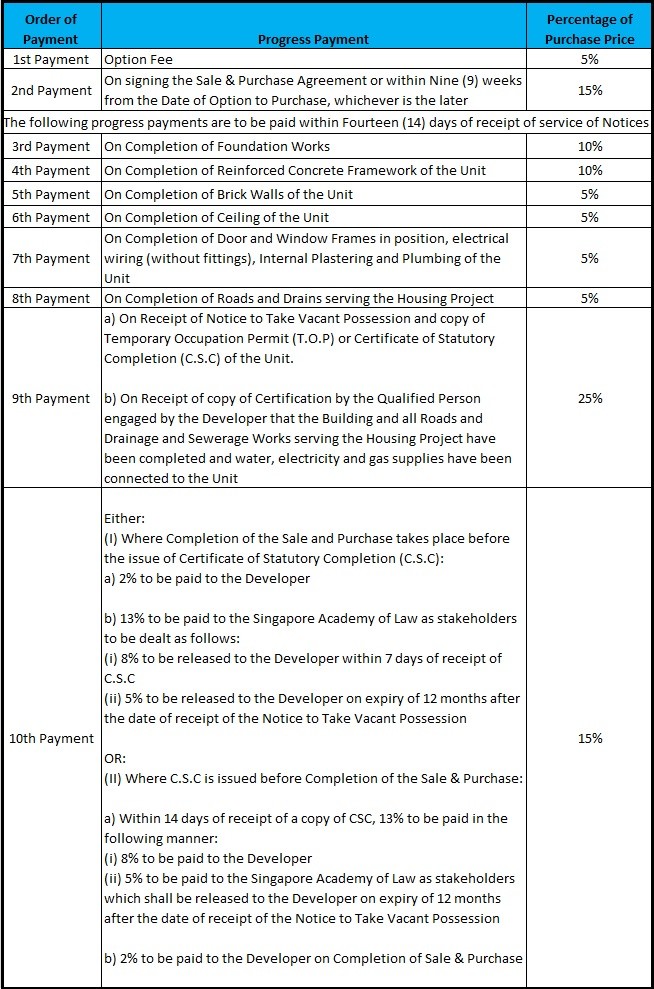

Progressive Payment Scheme

The progressive payment is a payment schedule for properties that are under construction. Buyers are required to pay a certain portion of the purchase price when a particular stage of construction is done. The breakdown as follow: