Summary

ELTA is a 501-unit, 99-year leasehold residential development along Clementi Avenue 1, positioned for buyers who prioritise school-belt proximity, modern high-efficiency layouts, and limited new-supply dynamics in a mature estate. The project sits at the upper end of OCR pricing benchmarks, reflecting both its educational adjacency and the scarcity of remaining GLS opportunities in this specific Clementi enclave.

Rather than competing as a transport-integrated or lifestyle-led launch, ELTA’s appeal is structural. Demand is anchored by families planning around long-term schooling considerations, academics tied to nearby institutions, and owner-occupiers who value a modern build within a proven residential catchment. This has translated into strong initial take-up despite visible resistance at higher absolute quantums.

The trade-offs are equally structural. Expressway adjacency introduces noise and dust considerations for specific stacks, PPVC construction limits future layout flexibility, and pricing sits meaningfully ahead of older resale benchmarks. ELTA therefore functions as a filtering project: it works for buyers who understand what they are paying for—and what they are consciously giving up.

ELTA should be assessed as a school-anchored, long-horizon own-stay asset with selective liquidity characteristics, not as a momentum-driven or convenience-optimised purchase.

ELTA is a high-rise OCR development designed for school-prioritising families and long-term owner-occupiers who accept expressway adjacency and premium pricing in exchange for modern efficiency and limited new-supply exposure in Clementi.

For buyers assessing whether ELTA aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

99-year leasehold private condominium

Clementi Avenue 1, Clementi Planning Area

Outside Central Region (OCR)

Two high-rise residential towers (39 storeys)

Positioned primarily for school-led owner-occupiers rather than short-cycle buyers

Project Factsheet

| Item | Details |

|---|---|

| Official Project Name | ELTA |

| Location | 10, 12 Clementi Avenue 1 |

| District / Planning Area | District 5 / Clementi |

| Region | Outside Central Region (OCR) |

| Tenure | 99-year leasehold (from 13 February 2024) |

| Site Type | GLS |

| Developer | Joint venture between MCL Land & CSC Land |

| Development Type | Pure residential |

| Site Area | Approximately 13,451.10 sqm |

| Plot Ratio | 3.5 |

| Total Units | 501 residential units |

| Building Configuration | 2 blocks of 39-storey residential towers with podium parking |

| Nearest MRT | Clementi MRT (mixed walk + bus access) |

| Launch Status | Launched |

| Launch Absorption | Approximately 63% sold on launch |

| Estimated TOP | 31 March 2029 |

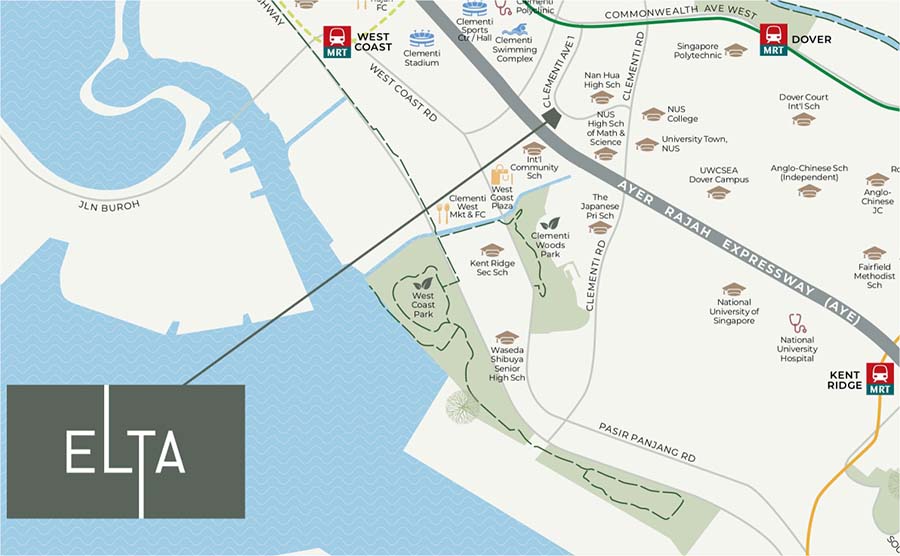

Location Context: Clementi as a School-Anchored Mature Estate

Clementi is a structurally different OCR location. Its value proposition is not centred on lifestyle spectacle or new-town transformation, but on educational infrastructure, institutional employment, and long-established residential demand. Daily convenience is anchored around Clementi Mall, neighbourhood centres, and a comprehensive bus network rather than doorstep MRT access.

ELTA sits along Clementi Avenue 1, within a dense academic and institutional belt that includes NUS, NUH, and multiple secondary and international schools. While Clementi MRT is not doorstep-adjacent, connectivity is functional through feeder buses and arterial road access. For drivers, AYE connectivity is a clear advantage; for car-lite households, this is a known compromise rather than an incidental inconvenience.

Importantly, ELTA’s school narrative must be read accurately. Nan Hua Primary School lies at approximately 1.49km from the site depending on block, placing the entire development within the 1–2km band, not within 1km. This supports long-term resale relevance for families but does not confer enrolment priority.

Development Scale and Configuration: Height as Differentiation

ELTA’s two 39-storey towers are an intentional response to a constrained site with a high plot ratio. Height is used to unlock views, light, and ventilation rather than to create a resort-style sprawl. High-floor units benefit from clearer sightlines toward the Wessex estate and beyond, which is uncommon in a mature Clementi streetscape.

The podium configuration elevates residential units away from road level, serving both as a buffer against traffic conditions and as a practical response to the site’s expressway adjacency. This is a functional design choice rather than a lifestyle flourish, and buyers should read it as such.

Planning Constraints Buyers Must Understand

ELTA’s constraints are explicit and permanent.

Expressway Adjacency:

Stacks facing the AYE will experience higher ambient noise and dust. Mitigation measures—such as acoustic ceilings and blinds—reduce impact but do not eliminate it. Stack orientation is therefore a primary decision variable, not a cosmetic preference.

PPVC Construction:

The project adopts PPVC, resulting in a higher proportion of structural walls. This limits future hacking and layout reconfiguration. Buyers seeking bespoke or highly flexible internal layouts should treat this as a hard constraint rather than a negotiable trade-off.

These factors explain why buyer sentiment is bifurcated: strong interest in well-oriented stacks, visible hesitation elsewhere.

Buyer Acceptances: What Actually Drives Demand

School-Belt Proximity

Demand is anchored by families planning ahead for primary and secondary education. While ELTA is not within 1km of Nan Hua Primary School, being within the 1–2km band remains a durable resale support factor in Clementi, particularly when paired with modern layouts and new-build condition.

Final GLS Opportunity Narrative

Buyers view ELTA as one of the last remaining GLS launches in this specific Clementi Avenue 1 enclave. Whether or not this proves absolute, the perception of tightening supply has clearly influenced early decision-making among long-time West-side residents.

High-Floor, Long-View Appeal

In a high-density district, unblocked or elevated views materially differentiate units. High-floor stacks have attracted stronger interest precisely because this attribute is difficult to replicate in future developments nearby.

Post-Harmonisation Layout Efficiency

GFA harmonisation has improved usable space efficiency. Buyers respond positively to layouts that feel more generous despite compact stated sizes, particularly for smaller and mid-sized units.

Buyer Objections: Where Resistance Is Concentrated

Price Leadership in the Immediate Enclave

ELTA sets a new pricing benchmark for Clementi Avenue 1. Resistance intensifies as psf levels approach the high-$2,000s and absolute quantums cross key psychological thresholds, especially for larger family units.

MRT Convenience Gap

Compared with fully integrated projects, the walk-and-bus commute to Clementi MRT is less seamless. For daily commuters, this becomes a quality-of-life consideration rather than a theoretical drawback.

Fixed Layout Constraints

PPVC-driven structural walls reduce renovation optionality. For buyers who value future reconfiguration, this is a meaningful limitation.

Pricing Context: Entry Validation vs Decision-Stage Reality

Launch Context:

Approximately 63% of units were taken up on launch, validating underlying demand for the location and product type. This reflects school-led and West-side loyalty rather than price softness.

Decision-Stage Reality:

Remaining inventory faces sharper scrutiny. Buyers now benchmark against resale projects such as Clavon and Clement Canopy, as well as newer Pine Grove alternatives. The decision hinge is not psf optics but absolute quantum and long-term holding comfort.

Buyer Suitability: Who This Works For—and Who It Does Not

Most Suitable For

School-prioritising families planning long-term residence

Owner-occupiers seeking a modern build in a mature estate

Academics and professionals tied to NUS, NUH, and One-North

Buyers comfortable paying a premium for location certainty

Least Suitable For

Buyers requiring doorstep MRT convenience

Those seeking flexible, hackable layouts

Short-cycle investors sensitive to near-term repricing

Noise-sensitive households considering expressway-facing stacks

Buyers comparing ELTA against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Takeaway

ELTA is not a compromise project—it is a selective one.

It rewards buyers who understand the value of school-belt proximity and limited new supply in Clementi, and it penalises those who underestimate price leadership, expressway realities, or layout rigidity. For aligned buyers, it offers long-term defensibility in a proven location. For misaligned buyers, it will feel expensive, constrained, and unforgiving.

Clarity of intent matters more here than timing.

If ELTA is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

FAQs (Decision-Stage)

1) Is ELTA considered expensive for OCR standards?

Yes. ELTA prices meaningfully ahead of immediate Clementi resale benchmarks. This premium is justified only for buyers who anchor value to school-belt proximity, new-build condition, and the scarcity of remaining GLS sites in this enclave. For price-led buyers benchmarking purely on psf or quantum, the valuation gap will feel structurally uncomfortable rather than temporarily mispriced.

2) Does ELTA’s proximity to Nan Hua Primary School materially change buyer outcomes?

It supports long-term relevance but does not confer enrolment priority. Being within the 1–2km band helps preserve resale demand among school-planning families, but it does not eliminate competition or guarantee placement. Buyers who treat this as a near-equivalent to a 1km advantage risk over-anchoring on a benefit that is supportive, not decisive.

3) How significant is the AYE noise and dust exposure in real terms?

For expressway-facing stacks, it is a permanent environmental condition rather than a marginal inconvenience. Acoustic treatments reduce impact but do not neutralise it. Buyers must select stacks deliberately; failure to do so affects both liveability and resale liquidity, particularly for family buyers sensitive to environmental comfort.

4) Does PPVC materially limit long-term flexibility?

Yes. PPVC introduces a higher proportion of structural walls, constraining future layout reconfiguration. This is not a cosmetic limitation. Buyers who anticipate hacking, room merging, or open-plan conversions should treat ELTA as misaligned rather than assume flexibility can be engineered later.

5) Why did smaller units absorb faster than larger configurations?

Smaller units sit within more accessible absolute quantums and appeal to investors and academics tied to nearby institutions. Larger family units face sharper resistance once prices cross key psychological thresholds. This pattern reflects affordability ceilings, not weak demand for the project as a whole.

6) Is ELTA suitable as an investment property?

Only selectively. Rental demand exists due to proximity to NUS, NUH, and One-North, but high entry prices cap yield expansion. ELTA functions better as a long-term, stability-oriented hold rather than a yield-maximisation or short-cycle investment.

7) How does ELTA compare with Pine Grove or West Coast alternatives?

ELTA’s advantage lies in its specific Clementi Avenue 1 positioning and school adjacency. Pine Grove and West Coast options offer different trade-offs around greenery, future supply, and pricing. Buyers should compare based on holding horizon and daily lifestyle tolerance, not psf optics alone.

8) Who is most likely to regret buying ELTA?

Buyers who underestimate expressway exposure, over-rely on school proximity without recognising enrolment realities, or expect layout flexibility that PPVC cannot provide. Regret risk here is driven by expectation mismatch rather than project execution.

PRICING LOGIC, URA PLANNING INTENT & BUYER SEGMENTATION

Summary

This section examines how ELTA’s pricing behaves across different market phases, how URA planning intent for Clementi frames long-term outcomes, and which buyer segments are actually converting versus hesitating. The central question is not whether ELTA is expensive, but who the pricing works for and under what holding assumptions.

Pricing Logic: Benchmark Leadership with Narrow Justification

Entry Pricing: Scarcity-Led, Not Convenience-Led

ELTA entered the market at pricing levels that set a new benchmark for Clementi Avenue 1. This was not driven by transport integration or lifestyle intensity, but by a combination of school-belt proximity, modern build condition, and the perception of limited remaining GLS supply in this pocket.

Early buyers were less focused on resale comparables and more anchored to replacement difficulty: the belief that similar new supply in this exact catchment would be rare. This explains the strong launch absorption despite visible price discussion.

Resistance Zone: Absolute Quantum, Not psf Optics

As the sales cycle progresses, resistance emerges primarily at the absolute price level, especially for 4- and 5-bedroom units. Once quantums move beyond psychologically comfortable thresholds, buyers begin cross-shopping against freehold resale options in West Coast and older but larger developments.

This resistance is structural. It is not resolved by time or marketing, but only by alignment with buyer intent.

Price Sustainability: Defensible, Not Accelerative

ELTA’s pricing is defensible for buyers who:

value school adjacency over transport convenience,

prioritise new-build efficiency over layout flexibility, and

plan to hold through a full schooling cycle or longer.

It is not positioned for price acceleration driven by lifestyle transformation or transport catalysts. Price behaviour is therefore more likely to be range-bound with selective liquidity rather than momentum-led.

URA Planning Intent: Supportive Backdrop, Not a Catalyst

Clementi’s Role in Regional Planning

URA planning for Clementi reinforces its role as a mature residential and educational node rather than a growth-stage transformation area. Enhancements focus on healthcare, green connectivity, and incremental housing additions rather than wholesale redevelopment.

This matters for ELTA because:

the area’s desirability is institutional, not speculative,

demand is recurring rather than event-driven, and

planning intent supports long-term relevance rather than short-term repricing.

Transport Improvements: Incremental Gains

Future transport projects improve regional connectivity but do not materially change ELTA’s immediate convenience profile. Clementi remains a bus-anchored town for most residents, with MRT access requiring a short walk or feeder ride.

Buyers should therefore treat URA and transport plans as defensive support, not upside drivers.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: School-Prioritising Owner-Occupiers

These buyers plan around primary and secondary schooling timelines. They accept pricing premiums and environmental trade-offs in exchange for location certainty and long holding horizons.

Secondary Segment: Academic and Institutional Investors

This group targets stable rental demand from NUS, NUH, and One-North. They are selective, focusing on efficient layouts and acceptable entry prices rather than yield maximisation.

Tertiary Segment: Multi-Generational Families

Families purchasing with long-term legacy considerations value modern layouts and proximity to established amenities. However, high absolute prices limit participation to higher-income households.

Absent Segments

Notably absent are short-term traders and buyers seeking flexible layouts. This absence explains why absorption becomes selective after the initial launch phase.

EXIT, LIQUIDITY & RISK SCENARIOS

Summary

This section models how ELTA behaves across different exit horizons, identifies liquidity constraints, and outlines the key risks buyers must consciously accept. ELTA rewards clarity of intent and penalises expectation mismatch more than most OCR projects.

Exit Behaviour: School-Led Liquidity, Stack-Specific Outcomes

Early Post-TOP (0–3 Years)

Liquidity is strongest for:

well-oriented stacks,

mid-sized units within comfortable quantums, and

layouts appealing to school-planning families.

Exit demand is driven by new-build appeal and school proximity rather than market momentum.

Mid-Cycle (3–8 Years)

Competition increases as newer launches enter the broader West region. Buyer scrutiny intensifies around noise exposure and layout rigidity. Liquidity becomes unit-specific rather than project-wide.

Long-Term (8+ Years)

School adjacency becomes a more meaningful differentiator as newer supply ages. However, resale success depends on realistic pricing rather than tenure or branding alone.

Structural Risks Buyers Must Model

1) Noise and Environmental Exposure

AYE-facing stacks face permanent exposure. This does not self-correct over time and affects both liveability and resale appeal.

2) Layout Inflexibility Risk

PPVC limits reconfiguration. Buyers cannot rely on renovation to “fix” layout dissatisfaction later.

3) Quantum Sensitivity

High absolute prices narrow the buyer pool, particularly during periods of tighter financing conditions.

4) Liquidity Compression Risk

ELTA’s buyer pool is specialised. In weaker markets, this results in longer selling periods rather than sharp price cuts.

5) Interest Rate Sensitivity

Higher rates disproportionately affect larger units, compressing demand among leveraged family buyers.

Final Assessment

ELTA behaves exactly as its structure suggests.

It trades transport convenience and layout flexibility for school adjacency, modern efficiency, and location certainty. Buyers aligned with these priorities are likely to find it coherent and defensible across market cycles. Buyers expecting lifestyle completeness, flexibility, or rapid repricing are likely to encounter friction rather than underperformance.

This is a project that rewards alignment, not optimism.

FAQs

1) Is ELTA a “safe” long-term purchase?

ELTA is safe only for buyers whose expectations align with its structural realities. Safety here means demand continuity from school-prioritising families, not price acceleration or liquidity ease. Buyers expecting flexibility, quiet living, or short-cycle exits will experience friction even if prices hold. The project rewards long holding horizons and clarity of purpose rather than optionality. Misalignment, not market downturns, is the primary risk.

2) How liquid will ELTA be on resale?

Resale liquidity at ELTA will be selective rather than broad-based. Well-oriented stacks with manageable absolute quantums are likely to attract steady interest from families planning around schools. Expressway-facing stacks and high-quantum units will face longer marketing periods, particularly in neutral or weaker markets. Liquidity risk manifests as time-to-exit, not sudden price collapse. Sellers must price realistically rather than rely on headline benchmarks.

3) Does proximity to Nan Hua Primary School guarantee resale demand?

No. School proximity supports demand, but it does not override pricing discipline or environmental considerations. Being within the 1–2km band provides relevance, not entitlement. Buyers still benchmark against newer alternatives, resale options, and noise exposure. School adjacency is a supporting pillar, not a substitute for value alignment. Over-reliance on this factor is a common buyer mistake.

4) Will expressway noise become less relevant over time?

No. Expressway adjacency is a permanent site condition. While traffic patterns may evolve marginally, noise and dust exposure for affected stacks does not disappear with time. Acoustic mitigation reduces impact but does not neutralise it. This affects both liveability and resale appeal consistently across market cycles. Buyers must assume this condition persists for the full holding period.

5) Can renovation overcome PPVC layout limitations?

No. PPVC introduces structural walls that cannot be meaningfully altered. Buyers who assume future renovation can “fix” layout dissatisfaction are likely to be disappointed. This constraint is most visible when family needs change over time. ELTA suits buyers who are comfortable with the original layout rather than those planning significant reconfiguration later.

6) Is ELTA suitable for leveraged buyers?

Only with caution. High entry prices combined with capped rental yields increase holding pressure during higher interest-rate environments. Larger units are especially sensitive, as financing costs scale faster than rental support. ELTA favours buyers with moderate leverage and income resilience rather than highly stretched financing strategies. Leverage amplifies friction more than returns here.

7) How does ELTA compare with freehold resale alternatives in the West?

Freehold resale options often offer lower entry prices and larger layouts but lack new-build efficiency and school-belt immediacy. ELTA trades tenure advantage for modern design, warranty coverage, and location certainty. Buyers must decide whether new-build clarity outweighs freehold optionality. This is a philosophical trade-off, not a numerical one.

8) Are larger unit types riskier at ELTA?

Yes. Larger units face narrower buyer pools due to high absolute quantums and financing constraints. Demand exists, but it is thinner and more price-sensitive. Exit timelines are likely longer, particularly outside strong market cycles. Buyers of larger units must be comfortable with slower liquidity and longer holding periods.

9) Is ELTA likely to outperform other OCR projects?

Outperformance is unlikely in the short to medium term. ELTA is positioned for defensibility rather than acceleration. Returns depend more on holding duration and entry discipline than on timing or market momentum. Buyers expecting ELTA to lead OCR price growth may be misaligned with its fundamentals.

10) Does URA planning materially change ELTA’s exit prospects?

URA planning supports long-term residential relevance but does not introduce catalytic upside for ELTA. Clementi’s evolution is incremental, not transformative. Exit outcomes depend more on unit selection, pricing realism, and buyer alignment than on planning announcements. Buyers should treat URA intent as a stabilising backdrop, not a repricing trigger.

11) How sensitive is ELTA to interest-rate cycles?

ELTA is moderately sensitive, particularly for larger units. Higher rates compress affordability and reduce the pool of leveraged family buyers. This does not usually force sharp repricing, but it extends selling timelines. Interest-rate risk here appears as liquidity drag, not volatility.

12) What is the most common mistake buyers make with ELTA?

Over-anchoring on school proximity while underestimating pricing, noise exposure, and layout rigidity. Buyers sometimes assume one strong attribute compensates for multiple trade-offs. This leads to dissatisfaction even when the asset performs as expected. ELTA demands holistic acceptance, not selective optimism.

13) Is ELTA better suited for own-stay or investment?

ELTA is primarily an own-stay project with secondary investment appeal. Rental demand exists, but yield expansion is capped by high entry prices. It works best as a long-term hold with rental serving as a buffer rather than a return driver. Investors seeking aggressive yield or rapid turnover should look elsewhere.

14) How important is stack selection at ELTA?

Stack selection is critical. Orientation materially affects noise exposure, daylight quality, and resale appeal. Differences between stacks can outweigh differences between unit sizes. Poor stack selection can underperform even if the overall project behaves predictably. Buyers should prioritise orientation over headline size or floor level.

15) Will future launches dilute ELTA’s appeal?

Future launches may dilute attention but not eliminate relevance. ELTA’s school adjacency remains a durable differentiator, but buyers will benchmark more aggressively as alternatives emerge. Pricing discipline becomes increasingly important over time. ELTA competes on clarity and location, not novelty.

16) Who should decisively avoid ELTA?

Buyers requiring doorstep MRT access, flexible layouts, quiet living environments, or short-term capital appreciation should eliminate ELTA early. These expectations conflict with the project’s structural design and pricing logic. Avoidance here is rational, not negative. ELTA rewards alignment, not compromise.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.