Summary

UPPERHOUSE at Orchard Boulevard is a 99-year leasehold private residential development located at 22 Orchard Boulevard in District 10, jointly developed by UOL Group Limited and Singapore Land Group under the Government Land Sales (GLS) programme. The project comprises 301 residential units housed within a single 35-storey tower, with limited commercial components at the first storey.

The defining differentiator for UPPERHOUSE is its direct, sheltered access to Orchard Boulevard MRT (TE13) on the Thomson–East Coast Line. In a Core Central Region context where most developments rely on walking proximity rather than integration, this materially alters daily liveability, tenant appeal, and long-term exit behaviour.

Rather than a tenure-led or ultra-luxury freehold proposition, UPPERHOUSE should be assessed as an address- and connectivity-driven CCR project. Its appeal is strongest for buyers who value Orchard proximity, car-lite living, and functional convenience, while accepting 99-year leasehold dynamics, CCR pricing discipline, and supply competition.

This review evaluates UPPERHOUSE from a decision-stage perspective, focusing on buyer fit and structural trade-offs rather than promotional narratives.

UPPERHOUSE at Orchard Boulevard is a 99-year leasehold, GLS-acquired mixed-use residential development in District 10 (CCR) that primarily appeals to buyers who prioritise direct MRT integration and Orchard Boulevard address convenience over freehold tenure, large-scale facilities, or short-term price momentum. Its value proposition centres on connectivity, location efficiency, and day-to-day liveability, while key trade-offs include leasehold tenure considerations, CCR supply competition, and relatively higher ongoing holding costs.

UPPERHOUSE should be assessed as an address- and connectivity-driven CCR project.

Explore the Full UPPERHOUSE Analysis

- UPPERHOUSE Price Guide – pricing structure, market positioning, and buyer entry analysis

- UPPERHOUSE Floor Plan Analysis – layout efficiency, stack considerations, and unit mix

- UPPERHOUSE Showflat Guide – showroom location and what buyers should evaluate during a viewing

If you’re considering this project, you might want to check how it actually compares and what most buyers tend to overlook — before deciding.

Key Details (at a glance)

99-year leasehold | ~301 units | Orchard Boulevard MRT (TE13) doorstep

District 10 (CCR / River Valley Planning Area)

GLS site | Mixed-use (residential with 1st-storey commercial)

Launched | Est. TOP 2029

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Upperhouse at Orchard Boulevard |

| Location | Orchard Boulevard, Singapore |

| District / Region | District 10 (Core Central Region) |

| Tenure | 99-year leasehold |

| Developer | UOL Group Limited & Singapore Land Group |

| Site Type | GLS (Government Land Sales) |

| Development Type | Private Residential (with commercial at 1st storey) |

| Site Area | Approx. 7,031.4 sqm |

| Plot Ratio | 3.5 |

| Total Units | 301 units (single tower) |

| Nearest MRT | Orchard Boulevard MRT (TE13) |

| Launch Status | Launched |

| Expected TOP | 30 June 2029 |

A connectivity-driven CCR residence offering direct MRT integration within the Orchard Boulevard enclave.

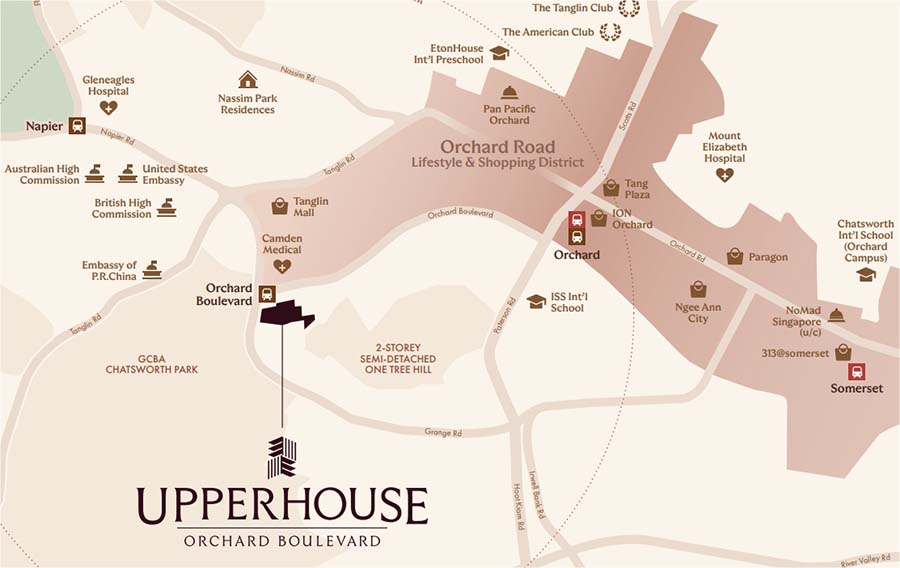

Location Context: Orchard Boulevard Without Orchard Road Intensity

UPPERHOUSE sits along Orchard Boulevard, a quieter residential stretch that functions as a buffer between Orchard Road’s retail spine and the River Valley enclave. Unlike developments embedded directly within the shopping belt, this location offers centrality without constant foot traffic or commercial congestion.

The project’s defining locational advantage is direct MRT integration. Orchard Boulevard MRT provides a one-line connection to Shenton Way, Marina Bay, and the CBD, materially changing commuting dynamics for District 10 residents. Daily conveniences are supported by nearby Orchard and Tanglin-area amenities, while Orchard Road remains easily accessible without being intrusive.

This location profile explains why buyer demand skews toward high-income professionals and owner-occupiers who value efficiency, privacy, and transit convenience over lifestyle buzz.

Buyers comparing UPPERHOUSE against other prime developments may find it helpful to contextualise its positioning within the broader Core Central Region (CCR) new launch landscape, where tenure, density, and buyer intent differ materially across projects.

Structural Value: Address-Driven Pricing Under a 99-Year GLS Model

The defining structural attribute of UPPERHOUSE is not tenure, but its Orchard Boulevard address combined with direct MRT integration.

As a GLS-acquired 99-year project, pricing discipline is anchored by land bid economics rather than redevelopment scarcity. Buyers are paying for location selectivity, transport efficiency, and a quieter residential environment within the Orchard belt — not for tenure-based capital preservation.

This means value justification depends heavily on entry pricing realism and own-stay alignment. Leasehold considerations become increasingly relevant over longer holding periods, particularly for buyers sensitive to exit optionality beyond the medium term.

Scale & Design Reality: Exclusivity Comes With Limits

UPPERHOUSE is a single-tower, low-unit-count CCR development, which delivers:

Greater privacy

Lower resident turnover

A more controlled residential environment

At the same time, buyers must accept:

A limited range of shared facilities

Fewer layout permutations compared to mega projects

Less lifestyle programming than larger CCR developments

This is a conscious design trade-off, not an oversight. Scale here prioritises restraint and privacy, but it does not offset leasehold dynamics or appeal to buyers seeking amenity-heavy living.

Project Positioning: What UPPERHOUSE Is — and Is Not

What UPPERHOUSE Is

A 99-year GLS CCR residential project

Address- and connectivity-driven

Suited for own-stay buyers prioritising Orchard proximity and MRT access

What UPPERHOUSE Is Not

Not a freehold or tenure-led capital preservation asset

Not a lifestyle-heavy or amenity-driven mega development

Not a short-term trading or yield-optimised investment

Clarity here prevents misaligned expectations.

Buyer Suitability: Who UPPERHOUSE Is Really For

Most suitable for

High-income professionals seeking MRT-integrated CCR living

Owner-occupiers prioritising Orchard convenience over scale

Buyers willing to trade freehold prestige for functional connectivity

Buyers who should reconsider

Legacy or multi-generational buyers fixated on freehold tenure

Yield-focused investors sensitive to maintenance costs

Short-term or momentum-driven buyers

These constraints are structural, not temporary.

Buyers Who Should Eliminate UPPERHOUSE Early

UPPERHOUSE should be eliminated early by buyers who are tenure-sensitive or legacy-focused, particularly those who benchmark District 10 purchases primarily on freehold permanence or multi-generational holding value. In a historically freehold-heavy enclave, the 99-year leasehold structure remains a real psychological and resale consideration over longer horizons.

Yield-focused investors should also approach with caution. While MRT integration supports rental demand, higher CCR entry pricing, ongoing supply competition, and relatively elevated maintenance fees limit yield optimisation and compress net returns compared to non-CCR or newer growth corridors.

Finally, buyers seeking large-scale lifestyle developments, extensive facilities, or short-term price momentum are likely to find better alignment elsewhere. UPPERHOUSE is intentionally restrained in scale and activation, and its value proposition is built around connectivity and address efficiency, not excitement or speculative upside.

Buyers comparing UPPERHOUSE against other CCR developments may find it helpful to frame their decision using the New Launch Condo Guide, particularly when evaluating differences in tenure, pricing structure, and buyer intent across projects.

Takeaway

UPPERHOUSE at Orchard Boulevard should be viewed as a connectivity-first, address-driven CCR residence, not as a tenure-led freehold substitute.

For buyers who value direct MRT access and Orchard Boulevard proximity, its positioning is coherent and defensible. For those seeking freehold security, strong yields, or short-cycle upside, expectations should be calibrated early.

If you’re seriously considering this project, it’s worth checking how it actually compares and what most buyers tend to overlook — before deciding.

FAQs (Decision-Stage)

1) Is UPPERHOUSE considered a luxury investment project?

UPPERHOUSE sits below the ultra-luxury freehold tier in District 10. Its appeal is driven more by direct MRT integration, Orchard Boulevard address relevance, and day-to-day convenience than by trophy-asset positioning. Buyers should evaluate it as a functional prime residence rather than a prestige-led luxury collectible.

2) How significant is the direct MRT access in practice?

Direct, sheltered access to Orchard Boulevard MRT is one of UPPERHOUSE’s most meaningful differentiators. In the Core Central Region, many projects offer proximity to MRT stations, but true integration materially improves commuting convenience, daily liveability, and tenant usability. Over time, this can also support broader buyer appeal relative to projects that depend on walking distance alone.

3) Does the 99-year leasehold tenure pose a long-term risk?

Yes, leasehold tenure remains a real consideration, especially within a district where freehold alternatives shape buyer psychology and resale comparisons. Buyers should be comfortable assessing the project on address efficiency, usability, and holding horizon rather than on tenure permanence. For longer-term holders, leasehold dynamics should be acknowledged early rather than rationalised away later.

4) Who is the typical buyer profile for UPPERHOUSE?

The typical buyer is a high-income professional, centrally located owner-occupier, or investor who values Orchard Boulevard proximity and direct MRT access more than freehold tenure or resort-style facilities. The project is best suited to buyers prioritising convenience, privacy, and everyday efficiency within the CCR. It is less naturally aligned with legacy-focused households or buyers seeking large-scale family-oriented living.

5) Is UPPERHOUSE suitable for rental investment?

Rental demand should be supported by its direct MRT access, central location, and proximity to the CBD and Orchard area. However, buyers should not expect unusually strong yields simply because the project sits in a prime district. Entry pricing, ongoing competition within the CCR, and tenant affordability limits mean the investment case is more stability-oriented than yield-driven.

6) How does it compare with nearby freehold projects?

Nearby freehold projects offer stronger tenure appeal and may feel more defensible to buyers focused on long-term capital preservation. UPPERHOUSE competes differently: it offers a more accessible entry into the Orchard Boulevard location profile while adding direct MRT integration, which many freehold alternatives do not provide. The decision depends on whether a buyer values tenure permanence more than transport efficiency and price accessibility.

7) Are maintenance fees a concern?

Maintenance costs should be viewed as part of the broader holding-cost framework rather than as an isolated line item. For owner-occupiers who prioritise location and convenience, this may be acceptable, but yield-sensitive investors should assess ongoing costs carefully because they can affect net returns over time. The more important question is whether the overall ownership cost aligns with the buyer’s intended holding strategy.

8) Should buyers expect strong short-term price appreciation?

UPPERHOUSE is not structured as a momentum-driven launch or a short-cycle trading story. Its pricing logic is tied more closely to address relevance, MRT integration, and own-stay usability than to speculative upside. Buyers are likely to be better aligned if they approach it with medium- to long-term expectations rather than immediate appreciation assumptions.

Pricing Logic, URA Planning Intent & Buyer Segmentation

Summary

UPPERHOUSE at Orchard Boulevard should be assessed as a 99-year, address-driven CCR residence, not as a momentum launch or yield-focused investment. Its pricing logic reflects Orchard Boulevard scarcity, direct MRT integration, and boutique scale under a GLS framework, rather than tenure premium or lifestyle activation. Buyers are paying for connectivity, location efficiency, and liveability, while accepting leasehold tenure dynamics, limited facilities, and more selective exit behaviour.

Pricing Logic: Address and Connectivity First, Everything Else Second

Pricing Context (Launched, Observed Behaviour)

UPPERHOUSE’s pricing reflects Orchard Boulevard address positioning and direct MRT integration within the Core Central Region, anchored by GLS land economics rather than redevelopment or tenure scarcity.

Entry pricing internalises:

Orchard-adjacent CCR location

Direct, sheltered MRT access (TEL)

Boutique, low-density single-tower configuration

Quiet residential frontage away from Orchard Road’s retail spine

At the same time, pricing does not benefit from freehold tenure and must be evaluated against other 99-year CCR alternatives, including newer integrated or larger-scale projects. As a result, upside potential is more constrained, and exit performance depends more on buyer alignment and usability than market momentum.

How Pricing Behaves Over Time

Projects like UPPERHOUSE typically show:

Lower volatility relative to mass-market launches

Muted upside during strong bull runs compared to momentum-led projects

Greater price stickiness during corrections due to own-stay demand

This behaviour is consistent with buyer profiles driven by usage, convenience, and address relevance, rather than speculative trading.

Absolute Quantum vs PSF: The Correct Evaluation Lens

For UPPERHOUSE, absolute quantum matters more than psf optics.

Why:

Buyers are often reallocating wealth or upgrading within CCR

Mortgage efficiency is not the primary decision factor

Comparable alternatives include other CCR homes competing on address and convenience

Using psf alone often leads to false comparisons with larger 99-year developments that offer scale or amenities but lack MRT integration or Orchard Boulevard positioning.

Explicit Pricing Decision Rules

If you value Orchard Boulevard proximity and direct MRT access, pricing is internally consistent.

If you expect rapid price appreciation or yield-driven performance, pricing will feel restrictive.

Buyers comparing purely on psf, facilities, or tenure prestige should eliminate this project early.

URA Planning Intent: Enhancement, Not Repricing

URA’s planning direction for the Orchard and River Valley Planning Areas focuses on:

Improved green connectivity and pedestrian comfort

Incremental public-realm enhancements

Maintaining Orchard Boulevard as a residential buffer rather than a retail hub

There are no large-scale redevelopment catalysts expected to materially reprice the immediate area. UPPERHOUSE benefits from planning certainty and liveability enhancement, not transformation-driven upside.

Buyer Segmentation: Who This Project Really Serves

1. CCR Owner-Occupiers (Primary Segment)

Profile

Medium- to long-term holding horizon

Strong preference for MRT convenience and central accessibility

Less facilities-driven, more usability-focused

Why It Works

Direct MRT access supports daily living efficiency

Orchard Boulevard remains structurally relevant

Boutique scale suits long-term own-stay use

2. Lifestyle-Light Capital Allocators (Secondary Segment)

Profile

Asset reallocation rather than yield chasing

Lower leverage, moderate risk tolerance

Preference for prime location usability

Limitations

Opportunity cost versus growth-oriented markets

Liquidity speed is not a key strength

3. Yield-Driven Investors / Traders

Suitability: Low

Entry pricing compresses yields

Ongoing CCR supply caps rental upside

Better alternatives exist for income-optimised strategies

Interim Assessment

UPPERHOUSE should be viewed as:

A 99-year, MRT-integrated CCR residence designed for long-horizon own-stay use and address efficiency, rather than yield optimisation or tenure-led capital preservation.

Exit & Liquidity, Risk Scenarios, Pros & Cons, and Buyer FAQs

Summary

UPPERHOUSE’s exit behaviour is governed by buyer selectivity rather than market momentum. Liquidity exists, but it is narrower and slower than mass-market CCR projects. Buyers who enter with realistic expectations around holding period, leasehold dynamics, and resale positioning are far more likely to be satisfied.

Exit & Liquidity Analysis

Liquidity Profile of Boutique 99-Year CCR Projects

Typical characteristics:

Smaller but more targeted buyer pool

Longer resale timelines

Less speculative price movement

Success depends on pricing discipline and buyer fit, not urgency.

Unit Type Sensitivity

Smaller units transact more consistently due to broader demand

Larger units appeal mainly to own-stay buyers

Floor height and orientation influence exit speed more than facilities

Timing Sensitivity

More sensitive to:

Interest-rate environment

CCR affordability sentiment

Less sensitive to:

Launch-day hype

Short-term policy noise

Risk Scenarios

Scenario 1: Prolonged High Interest Rates

→ Buyer pool narrows; holding horizon becomes more important

Scenario 2: Strong CCR Rally

→ Underperforms momentum-led mega developments

Scenario 3: Market Correction

→ Price support driven by own-stay demand rather than tenure

Scenario 4: Oversupply in CCR

→ Selectivity increases; differentiation via MRT integration matters

Pros & Cons Summary

Pros

Direct MRT integration (rare in CCR)

Orchard Boulevard address

Boutique, low-density living

Strong own-stay usability

Cons

99-year leasehold tenure

Limited facilities

Narrow buyer pool

Slower resale velocity

FAQs

1) How is UPPERHOUSE priced relative to other District 10 projects?

UPPERHOUSE is priced according to Orchard Boulevard address relevance and direct MRT integration rather than tenure premium or large-scale facilities. It generally sits below ultra-luxury freehold benchmarks in the area, but above more entry-level CCR projects that lack the same locational efficiency. Buyers should judge pricing based on usability, connectivity, and buyer fit rather than on psf alone.

2) Is UPPERHOUSE expensive for Orchard Boulevard?

For a 99-year CCR project with direct MRT integration, pricing is broadly consistent with what buyers would expect in this part of District 10. It may look expensive relative to older resale stock, especially freehold units with larger layouts, but those comparisons can be misleading because they do not offer the same transport convenience or new-launch positioning. The more useful question is whether the pricing matches the buyer’s intended holding horizon and lifestyle priorities.

3) What affects pricing the most for this project?

The main pricing drivers are Orchard Boulevard address relevance, direct sheltered MRT access, unit quantum, and broader CCR affordability conditions. Unlike momentum-led projects, UPPERHOUSE is less dependent on short-term sentiment and more tied to structural location value. Buyers should therefore focus on entry discipline and practical alignment rather than expecting pricing to be driven by hype.

4) Is this suitable for short-term investment?

UPPERHOUSE is not naturally structured for short-term flipping or momentum-based strategies. Its appeal is strongest for buyers who value long-term usability, central access, and a more stable own-stay profile rather than immediate resale upside. Entering with short-term expectations could lead to disappointment if pricing behaviour remains steady rather than explosive.

5) Does MRT integration materially improve resale prospects?

Yes, direct MRT integration is one of the project’s strongest long-term support factors because it improves daily liveability and broadens the pool of future buyers and tenants. In the CCR, many developments offer proximity to stations, but actual sheltered integration remains less common and therefore more meaningful. It does not remove leasehold considerations, but it does strengthen practical desirability over time.

6) Is rental demand strong?

Rental demand should be supported by the project’s central location, Orchard proximity, and direct MRT access to major employment districts. However, strong rental demand does not automatically translate into strong rental yield, especially when entry pricing is already elevated. Investors should view the rental case as supportive but not exceptional.

7) How long should buyers realistically hold?

A medium- to long-term holding period is the most sensible approach for UPPERHOUSE. This gives buyers more time to benefit from the project’s usability, location relevance, and stable demand profile rather than relying on short-cycle market movements. The project makes more sense as a hold-and-use asset than as a fast-turnover trade.

8) Does the small scale help or hurt liquidity?

The smaller scale helps create a more private and controlled residential environment, which can be attractive to certain owner-occupiers. At the same time, lower transaction volume and a narrower buyer pool can reduce resale velocity compared to larger projects with broader market visibility. In practice, it supports exclusivity but does not guarantee faster exits.

9) How does it compare with integrated CCR projects?

Integrated CCR projects usually compete on convenience, commercial activation, and a more dynamic live-work-play environment. UPPERHOUSE takes a different approach by focusing more on privacy, address efficiency, and quieter residential living while still benefiting from strong MRT access. The better choice depends on whether the buyer values lifestyle intensity or day-to-day residential calm.

10) Is Orchard Boulevard still relevant long term?

Yes, Orchard Boulevard remains structurally relevant because it sits within a prime district that continues to benefit from central connectivity and enduring address recognition. Its value lies less in dramatic transformation and more in stable urban relevance, accessibility, and proximity to Orchard’s wider amenity belt. Buyers should see it as a durable residential location rather than a speculative growth story.

11) What is the main downside risk?

The main downside risk is entering at a price that assumes too much from a 99-year CCR project, especially if the buyer expects tenure-like capital preservation or strong short-term appreciation. Misalignment between buyer expectations and project structure is the bigger risk than the location itself. Buyers need to be clear whether they are paying for real usability or for assumptions the project was never designed to fulfil.

12) How does it perform in downturns?

In softer market conditions, UPPERHOUSE may benefit from a degree of support from own-stay demand and its practical MRT-linked location. However, recovery may still be measured because CCR buyers tend to be more selective, and leasehold dynamics do not disappear in weaker markets. It is better positioned as a steady-use asset than a defensive outperformer.

13) Are larger units harder to exit?

Yes, larger units generally face a narrower resale audience because higher quantum reduces the number of potential buyers. In CCR projects, these homes tend to appeal more to affluent own-stay households than to broad-based investors or upgraders. That does not make them unattractive, but it does mean exit timing can be more selective.

14) Will future Orchard upgrades materially lift prices?

Future improvements in the Orchard area are more likely to enhance liveability, walkability, and overall environmental quality than to create sudden repricing. For UPPERHOUSE, these enhancements strengthen location quality and residential usability rather than serving as a direct price catalyst. Buyers should treat them as supportive background factors, not as the core investment thesis.

15) Is CCR supply a concern?

Yes, supply always matters in the CCR because buyers often have multiple competing options across different project types, tenure profiles, and pricing bands. This increases the importance of clear differentiation, and UPPERHOUSE’s main differentiator is its direct MRT integration within Orchard Boulevard. Supply does not invalidate the project, but it does make buyer positioning and entry discipline more important.

16) How should buyers evaluate UPPERHOUSE overall?

UPPERHOUSE should be evaluated as a connectivity-first, own-stay-oriented CCR residence rather than as a yield-led or tenure-driven asset. Its strongest case lies in Orchard Boulevard relevance, direct MRT access, and practical day-to-day efficiency within a prime district. Buyers who align with those strengths are more likely to find the project coherent than those approaching it with speculative or legacy-focused expectations.

If you prefer a more structured walkthrough, you can leave your details below and we’ll follow up with you.