Summary

Rivelle Tampines is a 99-year leasehold Executive Condominium (EC) located at Tampines Street 95 in District 18, developed by Sim Lian Group under the Government Land Sales programme. Positioned within a mature suburban estate, the project targets HDB upgraders who prioritise long-term own-stay liveability, MRT accessibility, and future EC privatisation dynamics rather than short-term capital gains or rental yield.

Unlike many ECs that rely on future-town narratives or feeder-bus connectivity, Rivelle Tampines differentiates itself through relatively direct access to Tampines West MRT and integration within Tampines’ established amenity ecosystem. This gives the project higher daily usability but also pushes it toward the upper boundary of EC affordability, especially after a record land bid.

Rivelle Tampines should therefore be evaluated not as a speculative opportunity, but as a long-horizon family residence where affordability discipline, layout efficiency, and holding capacity through the Minimum Occupation Period matter more than launch-phase momentum.

In practical terms, Rivelle Tampines is best understood as a utility-driven EC: one that trades headline discounts for connectivity and town maturity, rewarding buyers who are clear about staying long term and penalising those expecting quick liquidity or outsized upside.

Rivelle Tampines is a large-scale, MRT-accessible Executive Condominium designed primarily for family-oriented HDB upgraders seeking long-term own-stay stability in a mature Tampines location rather than short-cycle investment returns.

For buyers assessing whether Rivelle Tampines aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

-

99-year leasehold Executive Condominium

-

Tampines Street 95, District 18 (Tampines Planning Area)

-

Outside Central Region (OCR)

-

572 residential units

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Rivelle Tampines |

| Address | 51–71 Tampines Street 95, Singapore |

| District / Planning Area | District 18 / Tampines |

| Region | Outside Central Region (OCR) |

| Tenure | 99 years leasehold commencing 5 February 2025 |

| Site Type | GLS (New Launch EC) |

| Developer | Sim Lian Group |

| Development Type | Executive Condominium (Pure Residential) |

| Site Area | 22,488.9 sqm |

| Plot Ratio | 2.5 |

| Total Units | 572 residential units |

| Unit Mix | 3- to 5-Bedroom configurations (No 1- or 2-Bedroom units) |

| Nearest MRT | Tampines West MRT (Downtown Line), walk access |

| Launch Status | Preview / Pre-launch |

| Expected TOP | 30 June 2030 |

Unit Mix Breakdown

| Unit Type | Size (sqft) | Units | % of Total |

|---|---|---|---|

| 3BR Premium | 863 | 88 | 15.4% |

| 3BR Premium + Study | 926 | 153 | 26.7% |

| 4BR | 1044 | 145 | 25.3% |

| 4BR + Study | 1109 | 52 | 9.1% |

| 4BR Flexi | 1184 | 53 | 9.3% |

| 4BR Premium | 1184 | 41 | 7.2% |

| 5BR | 1378 | 40 | 7.0% |

Rivelle Tampines’ unit mix is overwhelmingly family-centric. With no 1- or 2-bedroom units and more than 50% of supply concentrated in four-bedroom formats, the project is clearly structured for upgrader households rather than compact formats typically associated with private-condo investor demand. Approximately 42% of units fall within the three-bedroom segment, which is likely to anchor both absorption and long-term liquidity due to MSR affordability thresholds. The significant allocation of four-bedroom units increases internal competition at resale and makes exit outcomes more sensitive to household income ceilings and prevailing interest-rate conditions, particularly within the regulated EC framework.

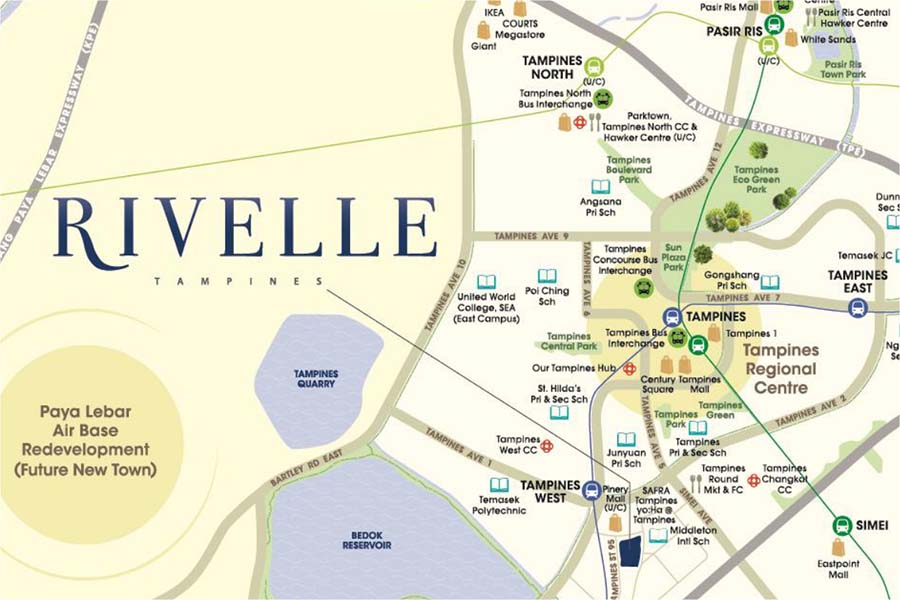

Location Context: Tampines Street 95 as a Mature Suburban Base

Tampines Street 95 sits within one of Singapore’s most established regional towns, offering a depth of amenities that few suburban locations can replicate. Unlike emerging estates that require years of infrastructure catch-up, Tampines already functions as a self-sufficient live-work-play hub anchored by Tampines Regional Centre.

Daily life here is structured around convenience rather than novelty. Residents have access to multiple supermarkets, hawker centres, schools across all levels, sports facilities, and healthcare within a short radius, with major retail nodes such as Our Tampines Hub, Tampines Mall, Century Square, and Tampines 1 forming a consolidated town centre rather than fragmented pockets.

Transport connectivity is a functional strength rather than a marketing gimmick. Tampines West MRT provides Downtown Line access that connects residents efficiently to employment nodes such as Changi Business Park, MacPherson, and the city fringe. Importantly, the project is walk-accessible without being physically integrated into transport infrastructure, which suits families prioritising residential calm over station adjacency.

From a planning standpoint, Rivelle Tampines benefits from URA’s long-term intent to strengthen Tampines as a people-centric regional centre. This supports long-term own-stay relevance rather than speculative appreciation tied to single infrastructure events.

Development Character: Scale, Density, and Family Orientation

Rivelle Tampines is a large-scale EC, and this scale is intentional.

With 572 units across multiple residential blocks, the project is structured to support full-family living rather than boutique exclusivity. This allows for a comprehensive facilities offering, internal circulation efficiency, and unit sizes that cater primarily to three-, four-, and five-bedroom households.

The trade-off is density. Buyers should expect a built-up residential environment rather than a low-density enclave. This is consistent with EC economics, where value is delivered through space efficiency and shared amenities rather than privacy per unit.

What matters more than scale is layout logic. Sim Lian Group’s projects are typically assessed by buyers on internal efficiency rather than architectural spectacle, and Rivelle Tampines is likely to follow this pattern, with practical unit configurations designed to keep absolute quantum manageable despite higher land costs.

Executive Condominium Reality: Why Rivelle Tampines Is Not a Short-Term Play

As an Executive Condominium, Rivelle Tampines operates under a different economic framework from private condominiums.

Buyers must satisfy eligibility conditions and adhere to a Minimum Occupation Period, during which resale and full-unit rental are restricted. These rules structurally remove speculative demand and front-load ownership toward genuine owner-occupiers.

This matters because Rivelle Tampines is priced at a level where the traditional “cheap EC” narrative no longer applies cleanly. Instead, its value proposition rests on long-term affordability relative to private condos, eventual privatisation dynamics, and sustained family demand within Tampines.

For buyers planning to hold through the MOP and beyond, this structure provides discipline and downside protection. For buyers seeking flexibility, liquidity, or early exits, the same rules become constraints rather than safeguards.

Pricing Context: Utility Premium Versus EC Affordability

Rivelle Tampines enters the market following a record EC land bid, which has sharpened buyer sensitivity around pricing and affordability. While indicative pricing has not been released, expectations already cluster around the upper end of historical EC benchmarks.

For EC buyers, the dominant decision variable is not price per square foot, but absolute quantum and monthly mortgage sustainability under the Mortgage Servicing Ratio. This creates natural resistance once family-sized units begin approaching private-condo quantum levels, even if the headline EC discount remains intact.

The key question for decision-stage buyers is therefore not whether Rivelle Tampines is “expensive,” but whether its MRT accessibility, mature-town convenience, and EC framework sufficiently justify the trade-offs relative to resale private condos or alternative ECs.

Buyer Suitability: Who Rivelle Tampines Actually Works For

Rivelle Tampines is best suited for families who understand EC mechanics and are comfortable with long holding horizons under a structured ownership framework.

Primary buyers are HDB upgraders from Tampines, Bedok, and Pasir Ris who value familiarity, school continuity, and proximity to extended family networks. Secondary demand typically comes from income-eligible households who prioritise larger internal space and are prepared to accept EC holding conditions in exchange for structured entry into private-format housing.

Conversely, buyers prioritising near-term liquidity flexibility, boutique positioning, or immediate rental optionality may find the EC framework misaligned with their objectives. For such households, the ownership structure may feel constraining rather than stabilising.

Buyers comparing Rivelle Tampines against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Ultimately, the suitability of an EC depends on how closely the ownership structure aligns with the household’s expected flexibility requirements over the next decade.

For readers assessing whether a nearby private alternative offers materially different liquidity timing within the same Tampines cluster, our Pinery Residences vs Rivelle Tampines comparison explains how exit flexibility and capital structuring diverge between EC and private ownership.

Takeaway

Rivelle Tampines is not designed to impress through novelty or lifestyle branding. Its relevance lies in utility, connectivity, and long-term own-stay logic within one of Singapore’s deepest upgrader towns.

For families planning to live through the MOP and beyond, and who value MRT access within a mature suburban ecosystem, the project’s positioning is coherent. For buyers expecting quick upside or flexibility, the same attributes become limiting rather than supportive.

Clarity of intent matters more here than optimism.

Pending Approval for Sale

If Rivelle Tampines is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

FAQs (Decision-Stage)

1) Is Rivelle Tampines considered expensive for an Executive Condominium?

Rivelle Tampines sits near the upper boundary of EC affordability due to its record land cost and MRT-accessible location. While this compresses the traditional EC discount, pricing must still remain within MSR and income-ceiling constraints, which naturally cap how far prices can go. For buyers aligned with long-term own-stay, the question is less about headline price and more about sustainable monthly commitments. Misalignment typically occurs when buyers benchmark it purely against older ECs without factoring in location and timing differences.

2) How important is MRT accessibility for an EC like Rivelle Tampines?

MRT walkability is relatively rare for ECs and materially improves daily usability, especially for households with one car or none. It also enhances long-term resale defensibility after privatisation, as transport convenience remains a durable buyer criterion. However, MRT access alone does not override EC affordability limits or holding-period constraints. It should be viewed as a quality-of-life enhancer, not a guaranteed value accelerator.

3) Who should avoid Rivelle Tampines despite its location?

Buyers seeking short-term capital appreciation or early exit flexibility should avoid the project. EC rules restrict resale and rental during the MOP, which conflicts with speculative or opportunistic strategies. Additionally, buyers uncomfortable with larger-scale developments may find the density less appealing. Avoidance here is about objective misfit, not project weakness.

4) Does the record land price increase downside risk for buyers?

A higher land cost reduces pricing buffer if the broader market softens, particularly for larger units. However, EC demand is driven primarily by owner-occupiers rather than investors, which tends to stabilise prices during downturns. The risk manifests more as slower absorption and longer holding periods rather than sharp price corrections. Buyers should assess their ability to hold comfortably rather than rely on market momentum. not designed for early exit)

5) Is Rivelle Tampines suitable for families planning to upgrade again later?

It can be, provided the holding horizon comfortably exceeds the MOP and buyers are not financially stretched. ECs reward patience and penalise forced exits, so flexibility is lower in the early years. Families anticipating relocation or lifestyle changes within a short timeframe should be cautious. Those planning stability tend to be better aligned.

6) How does Rivelle Tampines compare with resale private condos nearby?

Resale private condos offer immediate flexibility and rental options but often at higher entry prices for similar space. Rivelle Tampines trades flexibility for value-over-time, with the potential benefit of privatisation expanding the buyer pool later. The better option depends on whether buyers prioritise short-term optionality or long-term affordability. Direct comparison should focus on total quantum and holding intent, not just psf.

7) Will EC privatisation materially change Rivelle Tampines’ value?

Privatisation expands the buyer pool and typically improves liquidity, but it does not guarantee outsized price jumps. Value appreciation remains tied to entry price, unit selection, and broader market conditions. Privatisation should be viewed as removing constraints rather than creating automatic upside. Buyers expecting structural transformation may overestimate its impact.

8) What is the single most important thing buyers should evaluate before committing?

Affordability sustainability through the MOP and beyond. This includes realistic mortgage servicing under MSR, buffer for rate changes, and comfort with long holding periods. Rivelle Tampines rewards buyers who plan conservatively and punishes those who stretch for optionality. Alignment matters more than enthusiasm.

PRICING LOGIC, URA PLANNING INTENT & BUYER SEGMENTATION

Summary

Rivelle Tampines should not be assessed using private condominium benchmarks or momentum-driven launch logic. As an Executive Condominium, its pricing behaviour, absorption pattern, and long-term outcomes are governed by regulated affordability, upgrader household income ceilings, and eventual privatisation mechanics rather than investor demand or rental yield optimisation.

This section examines how Rivelle Tampines’ pricing is likely to behave across its sales cycle, how URA’s long-term planning for Tampines strengthens own-stay demand rather than speculative upside, and which buyer segments are structurally aligned — or misaligned — with the project.

Pricing Logic: Why Absolute Quantum Matters More Than PSF

Record Land Cost, But Not Unlimited Pricing Power

Rivelle Tampines was secured at a record Executive Condominium land rate, which naturally elevates pricing expectations. However, ECs remain constrained by:

-

a household income ceiling,

-

a strict Mortgage Servicing Ratio (MSR), and

-

a buyer pool dominated by owner-occupiers rather than investors.

These constraints mean pricing power is capped not by developer ambition, but by buyer affordability mechanics. Even strong demand cannot override MSR mathematics.

As a result, Rivelle Tampines’ pricing behaviour is more likely to reflect calibrated resistance zones rather than runaway momentum.

EC Buyers Anchor on Total Quantum, Not Headline PSF

Unlike private condominium buyers, EC purchasers evaluate affordability through total purchase price and monthly servicing comfort. This is because:

-

most EC buyers are upgrading families,

-

financing buffers matter more than resale optionality, and

-

ECs are not designed for early exit.

For Rivelle Tampines, the most price-sensitive segments are larger unit types, where absolute quantum begins to overlap with resale private condominiums in the same district. Smaller 3-bedroom units are therefore likely to see stronger absorption, as they sit within psychological affordability thresholds for dual-income households.

Expected Sales Behaviour Across Phases

Early Phase

-

Demand driven by MRT accessibility and Tampines familiarity

-

Strong take-up for lower-quantum family units

-

Buyers less price-sensitive initially

Mid-Cycle

-

Increased benchmarking against resale private condos

-

Heightened scrutiny on affordability and MSR headroom

-

Selective absorption rather than broad momentum

Late Phase

-

Demand driven by genuine own-stay needs

-

Pricing stabilises rather than accelerates

-

Fewer transactions, but less forced discounting

This is consistent with how mature-town ECs historically behave.

URA Planning Intent: Tampines as a Long-Term Demand Anchor

Tampines’ Role in the Master Plan

URA’s Master Plan positions Tampines as a self-sufficient regional centre, not a speculative growth frontier. Planning priorities focus on:

-

pedestrian-friendly town design,

-

integrated transport infrastructure,

-

community-centric amenities, and

-

incremental residential and commercial intensification.

This reinforces Tampines as a stable, family-oriented town rather than a volatility-driven investment zone.

Why This Matters for Rivelle Tampines

For Rivelle Tampines, URA intent supports:

-

sustained own-stay demand,

-

strong school-anchored housing decisions,

-

reduced reliance on CBD commuting,

-

long-term relevance rather than short-term repricing.

Importantly, there is no reliance on a single catalytic event. The project benefits from structural maturity, not transformation risk.

This aligns well with EC buyers, who prioritise predictability over speculative upside.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: HDB Upgrader Families

Profile

-

Currently living in Tampines, Bedok, or Pasir Ris

-

School-driven housing decisions

-

Long holding horizons

Why Rivelle Works

-

Familiar town ecosystem

-

MRT accessibility without city pricing

-

EC pricing advantage over new private launches

This group forms the backbone of sustainable demand.

Secondary Segment: Income-Capped, Private-Condo Alternatives

Profile

-

Household incomes near the EC ceiling

-

Priced out of new private launches

-

Comfortable with EC timelines

Why Rivelle Works

-

Larger layouts at lower total quantum

-

Potential upside after privatisation

-

Better affordability discipline than CCR/RCR options

Buyer Profiles That Struggle to Convert

-

Short-term investors

-

Yield-driven landlords

-

Buyers expecting boutique density

-

Households with uncertain holding horizons

These buyers face structural misalignment rather than project-specific issues.

Interim Assessment

Rivelle Tampines functions best as:

a long-horizon, family-centric EC supported by Tampines’ maturity and MRT utility, not as a momentum-driven launch.

Its performance will be shaped by:

-

affordability realism,

-

disciplined pricing,

-

and sustained upgrader demand.

EXIT, LIQUIDITY, RISK SCENARIOS, PROS & CONS, AND BUYER FAQs

Summary

Rivelle Tampines’ exit and liquidity behaviour is governed more by EC regulations and family-driven demand than by market cycles. This creates downside stability while naturally limiting short-term flexibility and upside acceleration.

Understanding these mechanics upfront is critical to avoiding expectation mismatch.

Exit & Liquidity Behaviour: ECs Follow a Time-Locked Curve

Liquidity by Phase

During MOP

-

No resale

-

No full-unit rental

-

Liquidity is effectively locked

Post-MOP (Singaporeans / PRs)

-

Buyer pool remains owner-occupier heavy

-

Liquidity improves, but remains selective

Post-Privatisation

-

Buyer pool expands meaningfully

-

Liquidity improves structurally

-

Pricing behaviour becomes more market-responsive

Rivelle Tampines rewards patience, not timing.

Unit-Type Exit Dynamics

- 3-bedroom units (241 units / 42%)

This segment is expected to demonstrate the strongest liquidity. It sits closest to typical dual-income MSR comfort zones and aligns with upgrader family demand. At resale, these units are likely to form the transactional backbone of the project. - 4-bedroom configurations (291 units / 51%)

While attractive for larger households, this is a heavy allocation. Exit success will be highly sensitive to affordability ceilings at the time of resale. Internal competition among similar-sized layouts may moderate pricing differentiation, especially in softer rate environments. - 5-bedroom units (40 units / 7%)

These serve niche multi-generational households. Liquidity will depend more on buyer matching than market timing. Scarcity exists within the project, but absolute quantum remains the dominant constraint.

For Rivelle Tampines, exit performance is shaped less by branding and more by MSR mathematics and household income growth over time.

Unit selection matters more than project branding at exit.

Risk Scenarios Buyers Must Accept

1) MSR Compression Risk

Higher interest rates reduce borrowing headroom, disproportionately affecting EC buyers. This does not usually cause price collapse, but slows transaction velocity.

2) Replacement Cost Risk

High land cost reduces margin for pricing error. If the broader market softens, sellers may need patience rather than price aggression.

3) Liquidity Delay Risk

EC exits depend on buyer eligibility and life-stage alignment. Liquidity manifests as time risk, not sharp volatility.

4) Opportunity Cost Risk

Capital locked during MOP cannot be redeployed. Buyers must be comfortable with reduced flexibility.

Pros & Cons Snapshot

Pros

-

MRT-accessible EC (rare)

-

Mature Tampines ecosystem

-

Strong family and school demand

-

Long-term privatisation upside

Cons

-

MOP restricts flexibility

-

Upper-bound EC pricing

-

Large-scale density

-

Limited appeal to investors

FAQs

1) Is Rivelle Tampines a good long-term asset?

Rivelle Tampines works best as a long-term, own-stay asset rather than a growth-oriented investment. Its value is anchored in EC affordability mechanics, Tampines’ maturity, and eventual privatisation rather than short-term price momentum. Buyers aligned with long holding horizons are more likely to experience stability rather than volatility. Misalignment typically arises when buyers expect private-condo-like performance from an EC structure.

2) How liquid will Rivelle Tampines be after the MOP?

Liquidity improves meaningfully after the MOP, but remains more selective than private condominiums. The buyer pool is still constrained by eligibility rules and affordability considerations. Transactions tend to occur when pricing aligns with upgrader budgets rather than during speculative phases. Liquidity risk manifests as longer selling periods, not sharp price drops.

3) Does MRT access guarantee better resale outcomes?

MRT access improves daily usability and resale defensibility, but it does not override EC affordability limits. Buyers still benchmark against total quantum, financing comfort, and available alternatives. MRT proximity functions as a support factor rather than a performance multiplier. Overreliance on connectivity alone can lead to unrealistic expectations.

4) Will EC privatisation significantly boost prices?

Privatisation expands the buyer pool and improves liquidity, but does not automatically trigger price surges. Value appreciation still depends on entry price, unit type, and broader market conditions. Privatisation removes structural constraints rather than creating guaranteed upside. Buyers expecting dramatic repricing may overestimate its impact.

5) Are larger units riskier to exit?

Yes, larger units face higher absolute price sensitivity, especially within EC affordability ceilings. While family demand exists, the buyer pool narrows materially at higher quantums. This does not make them poor units, but it increases the importance of pricing realism and patience. Exit success depends more on buyer matching than market timing.

6) How does Rivelle Tampines perform in a high interest-rate environment?

Higher rates compress borrowing capacity under MSR rules, which can slow EC demand. However, ECs often hold value better than private condos due to owner-occupier dominance. Price pressure tends to show up as slower sales rather than forced discounts. Buyers with conservative leverage are structurally advantaged.

7) Is Rivelle Tampines suitable for leveraged buyers?

Highly leveraged strategies are less suitable due to MSR constraints and MOP restrictions. Rental income cannot fully offset financing during early years, increasing holding pressure. The project favours buyers with strong CPF buffers and stable incomes. Leverage amplifies friction rather than returns in ECs.

8) What is the biggest mistake buyers make with ECs like Rivelle Tampines?

The most common mistake is evaluating ECs using private condominium logic. ECs reward affordability discipline and patience, not speculation. Buyers who stretch budgets or rely on early exit optionality often experience stress rather than underperformance. Alignment of intent matters more than optimism.

9) How does the absence of smaller units affect liquidity?

The absence of 1- and 2-bedroom units reduces investor-led churn and volatility. Liquidity will therefore depend almost entirely on genuine upgrader households rather than speculative demand. This creates stability but narrows the buyer pool to family profiles. The project behaves more like a time-locked family asset than a trading instrument.

10) Are 4-bedroom units structurally riskier than 3-bedroom units?

Yes, primarily due to higher absolute quantum under MSR constraints. While demand exists, affordability ceilings compress the eligible buyer pool during tighter interest-rate cycles. This increases time-on-market risk rather than price-collapse risk. Entry discipline becomes especially important for larger layouts.

11) Do affordability limits affect Rivelle Tampines’ resale pricing?

Yes. Although MSR governs new EC purchases, resale buyers are typically assessed under TDSR, which caps overall debt servicing. This means resale pricing is ultimately constrained by upgrader household borrowing capacity rather than developer land cost.

12) Does Rivelle Tampines compete directly with private condos?

Partially. Larger units may overlap with resale private-condo quantum levels, prompting comparison. However, EC restrictions and holding dynamics make the buyer psychology different. It is more accurate to say Rivelle competes on affordability discipline rather than flexibility.

13) Is the high 4-bedroom concentration a structural weakness?

Not inherently. It reflects deliberate targeting of larger upgrader families. The trade-off is heightened sensitivity to household income growth cycles. In stable income environments, this allocation supports depth; in tighter conditions, it slows liquidity.

14) Does scale reduce price upside?

Large-scale developments typically exhibit smoother pricing behaviour rather than sharp spikes. With 572 units, internal supply naturally moderates scarcity-driven appreciation. Stability tends to replace volatility. Buyers seeking explosive upside may find the trajectory measured rather than dramatic.

15) How important is holding beyond MOP?

Holding beyond MOP often improves liquidity conditions, particularly after privatisation. Early exits immediately post-MOP may still face eligibility-driven buyer constraints. A longer holding horizon reduces timing risk and improves optionality.

16) What is the core alignment test before committing?

Buyers must be comfortable with affordability sustainability through MOP, limited early flexibility, and family-driven exit demand. Rivelle Tampines rewards conservative planning and penalises short-term optionality assumptions. Clarity of intent is more important than launch sentiment.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.