Summary

Coastal Cabana is a 748-unit Executive Condominium (EC) located along Jalan Loyang Besar in Pasir Ris, positioned as a large-format, seaside-adjacent upgrade option for East-side HDB households. It combines rare coastal proximity for the EC segment with a full-scale, resort-style site plan and a Deferred Payment Scheme (DPS) structure that materially shapes buyer behaviour.

Rather than competing on transport integration or town-centre immediacy, Coastal Cabana is anchored around lifestyle differentiation, payment flexibility, and first-mover positioning within a long-dormant EC supply zone in Pasir Ris. This framing has driven strong initial absorption, but also introduces clear trade-offs around pricing sensitivity, MRT accessibility, and long-term exit expectations.

The project therefore functions less as a universal EC solution and more as a filtering development: it works well for buyers who value space, sea-adjacent living, and cash-flow flexibility, while becoming less compelling for those prioritising walkable transport, tighter price discipline, or short-cycle upside.

Coastal Cabana should be evaluated as a lifestyle-oriented, owner-occupier-led EC with structural strengths at entry, but with pricing and liquidity considerations that require expectation alignment rather than optimism.

Coastal Cabana is a large-scale, seaside-adjacent Executive Condominium designed for East-side HDB upgraders who prioritise lifestyle space and deferred payment flexibility over MRT proximity and short-term exit performance.

For buyers assessing whether Coastal Cabana aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

99-year leasehold Executive Condominium

Jalan Loyang Besar, Pasir Ris Planning Area

Outside Central Region (OCR)

Large, full-facility residential development (748 units)

Positioned primarily for owner-occupiers using DPS rather than investors

Project Factsheet

| Item | Details |

|---|---|

| Official Project Name | Coastal Cabana |

| Location | Jalan Loyang Besar (Nos. 2–32) |

| District / Planning Area | District 17 / Pasir Ris |

| Region | Outside Central Region (OCR) |

| Tenure | 99-year leasehold |

| Site Type | GLS |

| Developer | Qingjian Realty, China Communications Construction Co., ZACD Group |

| Development Type | Pure residential Executive Condominium |

| Site Area | 28,405.50 sqm |

| Plot Ratio | 2.5 |

| Total Residential Units | 748 |

| Block Configuration | 16 blocks (mostly 12 storeys; selected blocks at 11 storeys) |

| Height Control | Up to 49m SHD |

| MRT Access | Pasir Ris MRT (mixed walk + bus) |

| Launch Status | Launched |

| Launch Absorption | Approximately 68% |

| Expected TOP | 31 March 2029 |

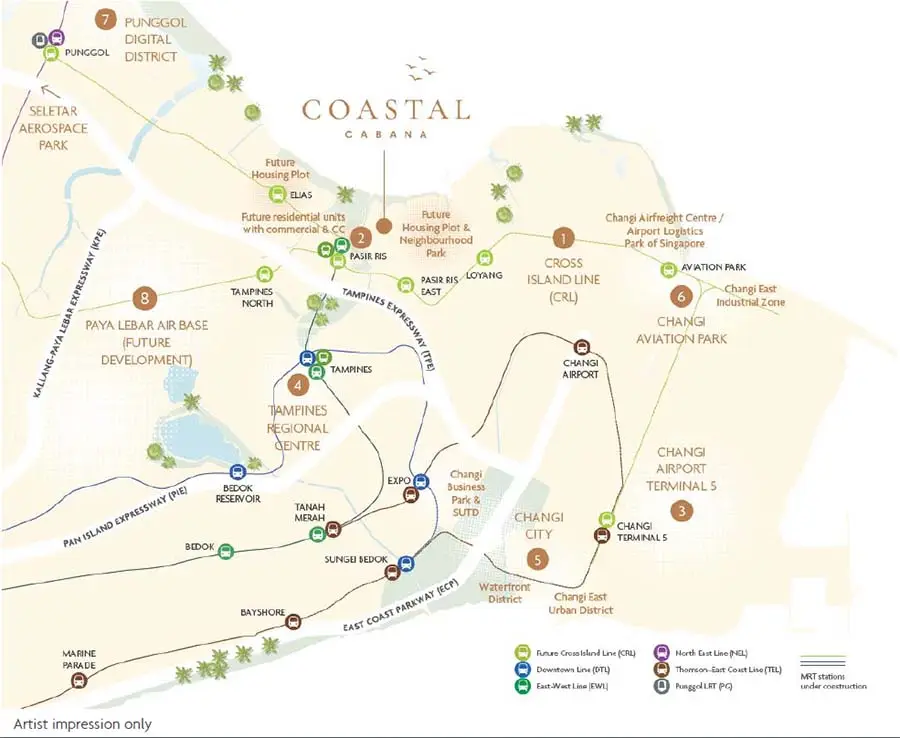

Location Context: Pasir Ris as a Lifestyle-Led, Not Transport-Led Choice

Pasir Ris has always occupied a distinct position within the OCR. Unlike Tampines or Punggol, it is less defined by rail-centric commuting efficiency and more by recreational space, coastal access, and low-intensity residential character.

Coastal Cabana sits closer to the eastern recreational spine than to the Pasir Ris town centre. Daily convenience is anchored around Downtown East, Pasir Ris Park, and surrounding leisure infrastructure rather than a traditional commercial core. This orientation is intentional: the project is designed around lifestyle adjacency rather than transit immediacy.

In practical terms, MRT reliance requires a combination of walking and bus usage. For drivers, expressway connectivity via TPE and PIE is straightforward. For car-lite households, however, the absence of doorstep MRT access is not a marginal inconvenience but a core trade-off that must be consciously accepted.

Over the medium to long term, Pasir Ris will see incremental enhancement through town-centre rejuvenation and broader regional upgrades. However, Coastal Cabana’s value proposition is not predicated on near-term transformation. Buyers should assess the location based on current liveability rather than future narratives.

Development Scale and Site Planning: Resort Logic at EC Density

With 748 units on a 28,405.50 sqm site, Coastal Cabana is unambiguously a large EC. Density is managed through block dispersion and north–south orientation rather than low unit count. This creates a resort-style internal environment but also introduces the realities of scale: shared facilities, peak-hour usage, and higher MCST expectations.

The site design emphasises airflow, internal openness, and communal lifestyle zones rather than exclusivity. This aligns with its target demographic — families upgrading from HDBs who value space, facilities, and outdoor amenities.

Coastal Cabana prioritises breadth of facilities and community scale over quiet, low-traffic living. Buyers should expect an active, family-heavy environment, particularly around shared amenities and during peak hours, rather than a subdued or tightly controlled residential setting.

Buyer Acceptances: Why Demand Concentrated Quickly

Scarcity of Coastal-Facing EC Units

True coastal adjacency is extremely rare in the EC segment. For many buyers, especially those already living in the East, the opportunity to secure sea-facing or park-adjacent stacks within EC eligibility constraints was the primary trigger for action.

High-floor stacks with clearer exposure saw the strongest early demand, reinforcing the idea that view-driven differentiation — rather than pure affordability — was central to buyer decision-making.

Proximity to Downtown East as a Functional Lifestyle Anchor

While not a traditional town centre, Downtown East functions as a self-contained lifestyle hub. Immediate access to supermarkets, dining, entertainment, and family-oriented amenities helps offset the project’s distance from Pasir Ris Central.

For households with young children or multi-generational living needs, this adjacency materially improves daily convenience despite MRT trade-offs.

Deferred Payment Scheme as a Structural Enabler

The DPS option materially reshaped affordability perception. For existing HDB owners with outstanding loans, the ability to defer major payment outlays until closer to TOP reduced cash-flow stress and allowed buyers to commit earlier than they otherwise might have.

This is not a marginal feature. DPS is central to understanding why absorption moved quickly despite headline pricing that sits at the upper end of historical EC norms.

GFA-Harmonised Layout Efficiency

Buyers responded positively to layout efficiency stemming from harmonised GFA rules, particularly the exclusion of non-usable technical spaces from strata area. For family buyers comparing ECs on livability rather than psf optics alone, this translated into a perception of better functional value.

Buyer Objections: Where Resistance Emerges

Record Land Cost and Pricing Sensitivity

Coastal Cabana entered the market with a land cost benchmark that inevitably translated into higher entry pricing. Launch pricing averaged around $1,734 psf, with meaningful resistance emerging as three-bedroom units crossed the $1.6M quantum threshold.

For EC buyers accustomed to wider buffers between EC and private pricing, this narrowed gap prompted more deliberate comparison and hesitation among price-sensitive upgraders.

MRT Distance as a Structural Constraint

The mixed walk-and-bus commute to Pasir Ris MRT is workable but not seamless. For households reliant on public transport, this becomes a daily friction point rather than a theoretical drawback.

While future rail enhancements may improve connectivity, buyer decisions today are anchored on present-day commuting realities.

Noise and Activity Spillover from Downtown East

Stacks facing Downtown East and adjacent leisure zones may experience higher ambient noise, particularly during weekends and school holidays. For buyers expecting a tranquil coastal environment, this requires careful stack selection rather than assumption.

Ongoing Cost Expectations

A large facility set and high unit count raise expectations of above-average MCST fees. For households already stretched by MSR limits, ongoing costs become as important as purchase price in long-term affordability calculations.

Pricing Context: Entry vs Decision-Stage Reality

Launch Pricing (Entry Benchmark):

Average launch pricing was approximately $1,734 psf. Three-bedroom units started from about $1.438M, with four-bedroom units from about $1.623M. Five-bedroom units were fully taken up early, reflecting pent-up demand for larger family layouts.

This pricing should be treated strictly as an entry-phase reference, not as an indicator of current availability.

Balance Unit Pricing (Decision-Stage Context):

Remaining units are positioned within a higher absolute quantum range, reinforcing the need for buyers to assess affordability based on today’s numbers rather than launch narratives.

The key decision question is not whether Coastal Cabana is “cheap for an EC,” but whether its lifestyle attributes justify its position relative to nearby private alternatives and resale benchmarks.

Buyer Suitability: Alignment Matters More Than Optimism

Most Suitable For

East-side HDB upgraders prioritising space and lifestyle

Families comfortable with deferred payment structures

Buyers valuing coastal proximity over MRT immediacy

Owner-occupiers planning to stay through and beyond MOP

Least Suitable For

Buyers reliant on walk-to-MRT commuting

Highly price-sensitive upgraders

Investors seeking short-cycle capital uplift

Households expecting boutique-style privacy

Buyers comparing Coastal Cabana against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Takeaway

Coastal Cabana is not a universally compelling EC — and that is precisely its point.

It rewards buyers who are clear about why they want seaside-adjacent living, larger family layouts, and deferred payment flexibility, and it filters out those who require transport immediacy or tighter price discipline. Entry success was driven by scarcity and pent-up demand, but long-term satisfaction depends on expectation alignment rather than headline comparisons.

If Coastal Cabana is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

FAQs (Decision-Stage)

1) What is Coastal Cabana’s real positioning among EC launches?

Coastal Cabana is not a transport-led or town-centre EC. Its positioning is built around seaside adjacency, large family-oriented layouts, and the cash-flow flexibility created by the Deferred Payment Scheme (DPS). Buyers evaluating it primarily on MRT proximity or short-term price momentum are likely to misjudge its intent and fit.

2) Why did Coastal Cabana achieve strong initial sales despite higher pricing?

Early absorption was driven by pent-up EC demand in Pasir Ris, the rarity of coastal-adjacent ECs, and DPS reducing immediate financial friction for HDB upgraders. This combination unlocked demand that may not have surfaced under a conventional progressive payment structure. Strong launch sales signal triggered demand, not immunity from longer-term price sensitivity.

3) Is the distance to Pasir Ris MRT a deal-breaker?

It is a structural trade-off, not a marginal inconvenience. Coastal Cabana relies on a mixed walk-and-bus commute, which works for households comfortable with flexibility but penalises buyers expecting walk-to-station convenience. Buyers must assess this as a permanent daily condition, not something to be “solved later.”

4) Does the Deferred Payment Scheme make the project more affordable?

DPS improves cash-flow timing, not total affordability. It helps buyers manage the transition from an existing HDB, but it does not reduce purchase price, long-term loan exposure, or holding costs. Buyers who rely on DPS to stretch beyond a comfortable budget often feel the pressure later, not at entry.

5) How should buyers think about pricing at decision stage, not launch stage?

Launch pricing should be treated strictly as historical context. Decision-stage buyers must evaluate remaining units based on current absolute quantum, unit availability, and realistic exit options after MOP. The key risk is anchoring to launch narratives instead of today’s numbers and choice set.

6) Is Coastal Cabana more suitable for own-stay or investment?

It is structurally an own-stay-led EC. Layouts, facilities, and buyer mix favour long-term family occupation rather than short-cycle capital turnover. While rental and resale markets will exist post-MOP, this is not a momentum-driven investment vehicle.

7) Will the large scale of the project affect liveability?

Yes — both positively and negatively. Large-scale ECs provide comprehensive facilities and community energy but come with higher shared density, peak-hour usage, and maintenance expectations. Buyers seeking privacy, quiet, or boutique living should recognise this mismatch early.

8) Who is most likely to regret buying Coastal Cabana?

Buyers who treat it as a transport-convenience project, underestimate long-term carrying costs, or rely on DPS to justify an overstretched budget are most at risk. Coastal Cabana rewards clarity and acceptance of trade-offs, not compromise-driven decisions. Regret typically stems from expectation mismatch, not project flaws.

Understood. Below is ENGLISH ONLY — PART 2 + PART 3, written strictly in NLR / Narra style, decision-stage, max authority, and fully aligned with the Part 1 positioning you approved.

No Chinese.

No schema.

No Part 1 repetition.

No sales language.

PRICING LOGIC, URA PLANNING INTENT & BUYER SEGMENTATION

Pricing Logic: Why Coastal Cabana Clears — and Where Resistance Forms

Launch Phase: Scarcity + Payment Structure Unlock Demand

At launch, Coastal Cabana’s pricing sat at the upper end of historical EC norms, with an average around $1,734 psf. On headline comparison alone, this appeared aggressive for an OCR EC located away from immediate MRT access.

What allowed absorption to move quickly was not price attractiveness in isolation, but friction reduction:

DPS materially lowered near-term cash flow stress for HDB upgraders.

Pasir Ris had not seen a new EC launch in over a decade, creating deferred demand.

Coastal adjacency introduced perceived lifestyle scarcity uncommon in the EC segment.

In this phase, buyers evaluated the project less against resale ECs and more against the absence of alternatives that met the same eligibility, space, and lifestyle criteria.

Decision-Stage Reality: Absolute Quantum Becomes the Gatekeeper

As sales moved beyond launch momentum, buyer behaviour shifted. Attention moved away from psf optics and toward absolute unit price, particularly for mainstream three-bedroom configurations.

Clear resistance emerged once three-bedroom units crossed the $1.6M psychological threshold, not because buyers rejected the project, but because:

EC buyers are MSR-constrained and quantum-sensitive by design.

The pricing gap between Coastal Cabana and nearby private alternatives narrowed.

DPS no longer offsets long-term affordability considerations.

At this stage, buyers stop asking “Is this rare?” and start asking “Can I hold this comfortably through MOP and beyond?”

Balance Units: Filtering Rather Than Broad Appeal

Remaining inventory behaves differently from launch stock. Buyers now compare Coastal Cabana against:

resale ECs with lower entry prices but shorter remaining leases, and

private condos offering stronger transport or town-centre integration at higher psf but comparable total quantum.

This naturally narrows the buyer pool to those who:

value lifestyle and space over transport immediacy, and

can absorb both purchase and holding costs without relying on optimistic exit assumptions.

Pricing therefore becomes selective rather than universally compelling, which is normal for ECs entering the mid-to-late sales phase.

URA Planning Intent: Pasir Ris as a Long-Arc Liveability Story

URA’s planning direction for Pasir Ris focuses on gradual town rejuvenation, not dramatic rezoning or catalytic redevelopment. The area is positioned as a recreational and residential sanctuary rather than a high-density employment or commercial node.

Key implications for Coastal Cabana:

Improvements enhance liveability rather than transform pricing dynamics.

Connectivity upgrades unfold over long timelines, not near-term step changes.

The district’s appeal remains family- and lifestyle-oriented rather than commuter-optimised.

For buyers, this reinforces an important point:

Coastal Cabana should be bought for how Pasir Ris lives today and matures steadily — not for a sudden uplift event.

Buyer Segmentation: Who Converts, Who Hesitates

Primary Segment — East-Side HDB Upgraders (Owner-Occupiers)

This group forms the core demand base. They are typically:

already living in Pasir Ris or Tampines,

upgrading for space, facilities, and environment, and

using DPS to manage transition from an existing flat.

Their decision is driven by lifestyle continuity rather than capital optimisation.

Secondary Segment — Family Buyers Seeking Space Over Location Prestige

These buyers prioritise:

larger layouts,

recreational proximity, and

a family-centric environment.

They are less sensitive to MRT distance but highly sensitive to absolute monthly outlay.

Weak or Absent Segments

Short-term investors

Buyers relying on aggressive post-MOP capital appreciation

Car-lite households requiring daily MRT walkability

The absence of these groups explains why demand is strong but not indiscriminate.

EXIT, LIQUIDITY, RISK SCENARIOS & PROS / CONS

Exit & Liquidity: How Coastal Cabana Behaves After MOP

Post-MOP Buyer Pool Characteristics

After MOP, resale demand is likely to come from:

upgrader households priced out of newer private launches, and

families prioritising space and amenities over transport convenience.

This buyer pool exists, but it is price-disciplined. Liquidity is present, but not elastic.

Liquidity Reality

Coastal Cabana’s exit profile is best described as:

transactional but selective, not thin but not fast.

sensitive to interest rate conditions and family affordability cycles.

dependent on unit type, orientation, and remaining lease optics.

Buyers should expect normalised EC resale behaviour, not outperformance.

Time-Phased Exit Scenarios

Early Post-MOP

Resale appeal supported by newness and facilities

Competition limited to older ECs

Liquidity strongest for mid-sized family units

Mid-Cycle

Newer ECs and private launches enter comparison set

Price realism becomes critical

Exit success increasingly unit-specific

Long-Term

Lease decay remains less visible initially but becomes relevant later

Exit increasingly dependent on Pasir Ris’s continued liveability

Lifestyle value matters more than launch-era narratives

Structural Risks Buyers Must Accept

1) Quantum Compression Risk

As EC prices rise, the affordability buffer versus private housing narrows. This caps upside and makes exits more sensitive to broader economic conditions.

2) Transport Friction Risk

MRT distance remains a permanent trade-off. It does not disappear with time and must be priced into exit expectations.

3) DPS Illusion Risk

DPS eases entry but can mask long-term affordability stress. Buyers relying on DPS to stretch budgets face higher risk during holding.

4) Density & Cost Risk

Large-scale facilities raise maintenance expectations. MCST costs are manageable but non-trivial for MSR-bound households.

Pros & Cons (Decision-Stage Framing)

Pros

Rare coastal-adjacent EC positioning

Large family-oriented layouts

Comprehensive facilities and lifestyle environment

DPS improves transition flexibility

Strong owner-occupier demand base

Cons

Not walk-to-MRT

High absolute quantum for EC segment

DPS can distort affordability perception

Exit is selective, not momentum-driven

Large-scale living not suited to privacy seekers

FAQs

1) Will Coastal Cabana outperform other ECs after MOP?

Outperformance should not be the base case. Coastal Cabana is priced near the upper band of EC affordability, which limits percentage upside even if absolute prices hold. Outcomes will be driven by entry discipline and unit selection, not project-wide momentum or scarcity narratives.

2) Is the current price gap versus private condos still compelling?

The gap exists but is structurally narrower than in past EC cycles. Buyers are no longer buying ECs at a deep discount to private housing, but at a moderated entry point with eligibility constraints. This means value must be justified by liveability and affordability, not by assumed price convergence.

3) Does coastal proximity materially change resale behaviour?

It improves differentiation but does not override core resale drivers such as quantum, financing ability, and transport convenience. Coastal adjacency helps attract attention, but buyers still negotiate on price and practicality. It functions as a support factor, not a premium multiplier.

4) How resilient is resale demand during weaker market cycles?

EC resale demand contracts faster than private housing during downturns because the buyer pool is more leverage-sensitive. In weaker cycles, Coastal Cabana is more likely to experience longer selling periods rather than sharp price collapses. Liquidity risk here manifests as time, not necessarily price.

5) Does the large scale of the project help or hurt resale liquidity?

Scale increases familiarity and visibility, which helps baseline liquidity. However, it also creates internal competition, especially for similar unit types and stacks. Resale outcomes will therefore be unit-specific rather than project-wide.

6) Are larger units safer for exit because families prefer them?

Not automatically. Larger units face higher absolute quantum resistance, even if family demand exists. In many EC resales, mid-sized units clear faster because they sit within a broader affordability band.

7) How does MRT distance affect exit value over time?

It remains a permanent pricing constraint. While buyers may tolerate transport friction during buoyant markets, it becomes a sharper negotiation point during softer conditions. MRT distance does not “fade” as a concern — it reappears whenever buyers gain bargaining power.

8) Will future transport upgrades eliminate this weakness?

No. Connectivity improvements may reduce friction but will not convert the project into an MRT-adjacent development. Buyers should assume the current commute reality persists and price their exit expectations accordingly.

9) Does DPS increase long-term resale risk?

Indirectly, yes. DPS can encourage buyers to commit at higher price points than their long-term affordability comfortably supports. This increases sensitivity during resale if household finances tighten or interest rates rise.

10) Is Coastal Cabana suitable as a rental-hold asset post-MOP?

Rental demand exists, driven by families and professionals working in the East. However, yields are capped by high entry prices and EC design. Rental should be viewed as a holding buffer, not a return driver.

11) How exposed is the project to interest rate changes?

Highly exposed. EC buyers are typically MSR-bound and leverage-dependent, making both purchase and resale demand sensitive to financing conditions. Higher rates primarily reduce buyer pool depth rather than immediately compress prices.

12) Can buyers rely on “first EC in Pasir Ris in many years” as a value anchor?

Only at entry, not at exit. Scarcity matters most when buyers have no alternatives, which is rarely the case during resale. Exit pricing will be benchmarked against newer launches and private alternatives, not historical launch narratives.

13) How does Coastal Cabana compare to resale ECs during exit?

It benefits from newer condition and fuller facilities, but resale ECs often compete aggressively on price. Buyers exiting must be realistic about how much premium “newness” still commands several years after TOP.

14) What is the biggest downside scenario buyers underestimate?

Affordability compression. Even modest changes in interest rates, household income, or market sentiment can significantly narrow the resale buyer pool at higher quantums. This risk does not show up at launch — it emerges later.

15) Who should avoid holding Coastal Cabana long-term?

Buyers who rely on tight cash flow, expect rapid repricing, or need high liquidity flexibility should reconsider. The project rewards stability and patience, not financial stretch or timing-based exits.

16) What is the correct way to think about exit success for this project?

Exit success should be defined as stable resale within a reasonable timeframe, not outperformance. Buyers who enter with conservative assumptions, manageable leverage, and realistic holding horizons are most likely to achieve satisfactory outcomes. Those expecting the project to “carry” their exit will be disappointed.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.