Summary

Bloomsbury Residences is a 358-unit, 99-year leasehold residential-led development at Media Circle in District 5, positioned as the first large-scale private housing entry into the Mediapolis / one-north innovation precinct. Its appeal is not driven by lifestyle completeness or MRT adjacency, but by first-mover positioning within a long-term employment-anchored district and by space-efficient post-harmonisation layouts that recalibrate buyer expectations of value in this part of Queenstown.

Rather than competing with established residential enclaves like Holland Village or Buona Vista, Bloomsbury Residences targets a narrower but distinct buyer segment: professionals whose daily lives orbit one-north and who prioritise proximity to work, modern internal space efficiency, and long-term rental defensibility over neighbourhood vibrancy or short-term price momentum. This creates a clear filtering effect in buyer response.

The project’s performance reflects that positioning. Approximately 25% of units were absorbed on launch day, with subsequent take-up progressing steadily rather than explosively. This pattern signals conviction-led buying rather than mass-market urgency, and underscores that Bloomsbury Residences is best evaluated as a long-horizon, employment-centric residential asset rather than a lifestyle-first or momentum-driven new launch.

Bloomsbury Residences is a first-mover, employment-anchored residential development in Media Circle designed for buyers who prioritise proximity to one-north, modern space efficiency, and long-term holding logic over MRT immediacy, lifestyle density, and short-cycle price acceleration.

For buyers assessing whether Bloomsbury Residences aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

• 99-year leasehold | Large-scale residential-led development with limited ground-floor retail

• Media Circle, District 5 (Queenstown Planning Area)

• Rest of Central Region (RCR)

• Positioned for professionals, owner-occupiers, and long-term investors linked to one-north employment clusters

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Bloomsbury Residences |

| Location | 51, 53, 55 Media Circle |

| District / Region | District 5 / Rest of Central Region (Queenstown Planning Area) |

| Tenure | 99 years leasehold from 7 May 2024 |

| Developer | Media Circle Development Pte. Ltd. (JV led by Qingjian Realty & Forsea Holdings) |

| Site Type | GLS |

| Development Type | Residential-led development with limited commercial on first storey |

| Site Area | 10,632.10 sqm |

| Plot Ratio | 2.9 |

| Total Units | 358 residential units |

| Launch Status | Launched |

| Expected TOP | 7 February 2029 |

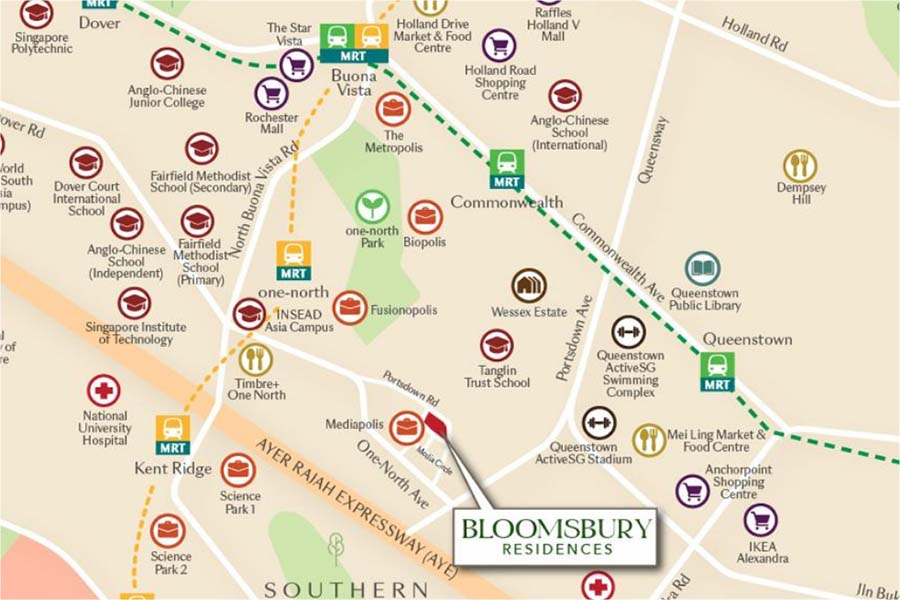

Location Context: Media Circle as an Employment-First Residential Node

Media Circle sits at the edge of Singapore’s one-north ecosystem, a district defined less by residential heritage and more by its concentration of research, technology, biomedical, and media employers. Unlike traditional District 5 neighbourhoods anchored by schools, wet markets, or legacy town centres, Media Circle functions primarily as a workday environment.

This distinction matters. Daily foot traffic peaks during office hours and tapers significantly after work, creating a quieter residential atmosphere relative to lifestyle hubs such as Holland Village. For some buyers, this absence of vibrancy is a drawback. For others — particularly professionals working nearby — it translates into shorter commutes, less congestion, and a clearer separation between work proximity and residential calm.

Bloomsbury Residences’ value proposition is inseparable from this context. It is not attempting to retrofit Media Circle into a lifestyle precinct. Instead, it positions itself as a residential solution for those already embedded in the one-north ecosystem, where proximity to employment outweighs walk-to-café expectations.

Development Character: Density, Elevation, and Integrated Retail

The project comprises three residential towers of varying heights, elevated above surrounding roads due to the site’s sloping terrain. This elevation has two structural consequences. First, it creates a raised landscaped deck that separates residential spaces from street-level activity. Second, it introduces a clear vertical zoning between retail, parking, and living areas.

The inclusion of limited first-storey retail is not lifestyle-driven but functional. The retail component is sized to support day-to-day convenience rather than destination spending, aligning with the project’s employment-anchored audience. While some buyers express concern about potential noise or foot traffic, the scale of the retail element suggests a supplementary role rather than a dominant activity generator.

From a planning perspective, the project’s density is a direct response to its 2.9 plot ratio. This necessitates a high-rise solution and places Bloomsbury Residences firmly in the category of urban, efficiency-led living rather than low-density or boutique residential formats.

Space Efficiency and Post-Harmonisation Layouts

One of the project’s strongest acceptance points lies in its post-harmonisation layouts. The absence of air-conditioning ledges and the recalibration of balcony treatment result in higher internal usability relative to older District 5 launches.

For decision-stage buyers, this translates into a more tangible value proposition. Rather than comparing headline price per square foot alone, many buyers focus on how much of the unit is genuinely liveable. This is particularly relevant for two- and three-bedroom configurations, which form the bulk of the unit mix and cater to professional households rather than multi-generational families.

This layout efficiency partially offsets concerns around absolute pricing and supports the project’s positioning as a practical, modern housing solution rather than an aspirational lifestyle statement.

MRT Reality: Acceptable for Some, Disqualifying for Others

Bloomsbury Residences does not offer doorstep MRT access. Walking distances to One-North or Commonwealth MRT stations are generally perceived as borderline for fully sheltered, daily commuting, particularly in Singapore’s climate.

This factor acts as a natural filter. Car-lite buyers or tenants who prioritise immediate MRT access often eliminate the project early. Conversely, buyers with flexible commuting patterns, private transport, or hybrid work arrangements are more accommodating of the trade-off, especially when balanced against proximity to workplaces.

Importantly, this is not a marginal inconvenience but a structural attribute. Buyers who proceed do so with eyes open, while those who place MRT proximity at the top of their criteria typically self-select out.

First-Mover Dynamics in Media Circle

As the first major private residential launch in Media Circle, Bloomsbury Residences carries both advantage and risk.

The advantage lies in entry positioning. Early buyers perceive a buffer against future GLS launches that may enter the market at higher land costs, potentially resetting benchmarks upward. This first-mover narrative supports long-term holding logic rather than immediate price uplift.

The risk lies in construction adjacency and future supply. Subsequent GLS parcels in the vicinity will introduce competition, both during the construction phase and at TOP. Buyers must be comfortable with the reality of phased neighbourhood maturation rather than expecting a fully formed residential environment from day one.

This duality explains the project’s steady but measured absorption profile.

Pricing Behaviour and Buyer Resistance

Pricing discussions around Bloomsbury Residences often revolve around relativity rather than absolutes. While launch prices were positioned below some established District 5 benchmarks, resistance emerges as unit quantum increases, particularly for larger configurations.

For many buyers, the psychological threshold is less about price per square foot and more about total outlay. Once pricing approaches levels comparable to mature or more lifestyle-complete alternatives, buyers reassess trade-offs around convenience, amenities, and neighbourhood character.

This does not invalidate the project’s pricing logic, but it narrows the conversion pool to those whose priorities align closely with the project’s employment-centric proposition.

How Buyers Actually Compare Bloomsbury Residences

In practice, Bloomsbury Residences is rarely evaluated against suburban family developments or city-centre luxury projects. Its comparison set is more specific.

One comparison group includes other one-north-adjacent launches that offer stronger MRT integration or more established residential surroundings. Another consists of resale options within Queenstown that provide immediate neighbourhood maturity but lack modern layouts and facilities.

Buyers who choose Bloomsbury Residences typically do so after concluding that proximity to work, modern space efficiency, and long-term rental defensibility outweigh the benefits of lifestyle vibrancy or MRT immediacy.

What Bloomsbury Residences Is — and Is Not

What It Is

• A first-mover residential development within the Media Circle / one-north employment zone

• Designed around modern, space-efficient layouts for professional households

• Anchored by long-term employment demand rather than lifestyle footfall

• Structured for steady, conviction-led absorption rather than rapid sell-outs

What It Is Not

• Not a lifestyle-centric or amenity-rich neighbourhood hub

• Not an MRT-fronting or car-lite-optimised development

• Not positioned for short-term flipping or speculative momentum

• Not a family-first project anchored by schools or community retail

Understanding this distinction early is critical to avoiding expectation mismatch.

Buyer Suitability: Who This Project Works For

Most Suitable For

• Professionals working in one-north, Mediapolis, or adjacent business parks

• Owner-occupiers prioritising commute efficiency and modern internal space

• Long-term investors targeting employment-driven rental demand

• Buyers comfortable with phased district maturation

Least Suitable For

• Buyers requiring doorstep MRT access

• Families seeking lifestyle density or extensive on-site facilities

• Short-term investors focused on rapid price appreciation

• Buyers expecting a fully formed residential neighbourhood at TOP

Buyers comparing Bloomsbury Residences against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Takeaway

Bloomsbury Residences is a filtering project, not a universal one.

It rewards buyers who are clear about why they want to live near one-north and are comfortable trading MRT immediacy and lifestyle vibrancy for commute efficiency, modern layouts, and long-term employment-anchored demand. For aligned buyers, the project offers coherence and defensibility. For misaligned ones, it will feel inconvenient, quiet, or overpriced.

Clarity of intent matters more here than timing or optimism.

If Bloomsbury Residences is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

FAQs (Decision-Stage)

1) What is the real reason buyers choose Bloomsbury Residences?

Buyers choose Bloomsbury Residences primarily for employment proximity and space efficiency, not lifestyle appeal or transport convenience. Its strongest pull comes from being embedded within the one-north / Mediapolis employment ecosystem, where daily commute reduction matters more than neighbourhood vibrancy. The project works when buyers’ work–life geography is already centred around this district. Without that alignment, the value proposition weakens quickly.

2) Why does Bloomsbury Residences feel polarising to some buyers?

Because the project makes explicit trade-offs rather than trying to please everyone. It does not offer doorstep MRT access, a vibrant retail street, or a family-centric environment. Instead, it prioritises modern internal layouts and proximity to work. Buyers who value convenience and lifestyle density often disengage early, while those who accept these trade-offs tend to commit with clearer intent.

3) Is the MRT walking distance a long-term structural weakness?

It is a structural characteristic, not a temporary inconvenience. MRT proximity is unlikely to improve materially, so this factor will continue to filter the buyer and tenant pool over time. However, for occupants working nearby or relying less on rail transit, the impact is reduced. The key is that this limitation does not disappear — buyers must be comfortable carrying it throughout the holding period.

4) Does Media Circle’s current lack of residential maturity pose a risk?

Only if buyers expect immediate neighbourhood completeness. Media Circle is an employment-first precinct, not a traditional residential town, and its residential character will evolve gradually rather than rapidly. For buyers who need established amenities from day one, this is a misalignment. For long-term holders who are comfortable with phased district development, it is a known and manageable condition rather than a hidden risk.

5) Why is layout efficiency such a major talking point for this project?

Because Bloomsbury Residences is evaluated more on usable internal space than on headline price metrics. Post-harmonisation layouts reduce non-livable areas, which materially improves day-to-day functionality for small households. This matters more to professional owner-occupiers than facility scale or façade presence. For this buyer group, how the unit lives often outweighs how the project looks.

6) Is Bloomsbury Residences suitable for short-term investors or flippers?

No. The project is not structured for momentum-driven price acceleration or fast resale turnover. Buyer demand is conviction-led rather than speculative, which supports stability but limits rapid liquidity. Investors considering Bloomsbury Residences should frame it as a long-horizon, employment-anchored asset, not a short-cycle trading opportunity.

7) How do buyers usually benchmark Bloomsbury Residences against alternatives?

Buyers typically compare it against other one-north–adjacent launches or against older resale developments within Queenstown. The decision often hinges on whether modern layouts and work proximity justify giving up neighbourhood maturity or MRT immediacy. When Bloomsbury is chosen, it is usually because buyers conclude that these trade-offs align better with their daily routines and long-term plans.

8) Who should eliminate Bloomsbury Residences early in the search process?

Buyers who require doorstep MRT access, vibrant daily amenities, or family-oriented living environments should exclude the project early. Similarly, those expecting short-term capital appreciation or rapid resale liquidity are likely to be disappointed. Bloomsbury Residences rewards clarity of intent and penalises expectation mismatch more than most District 5 projects.

RICING LOGIC, URA PLANNING INTENT & BUYER SEGMENTATION

Summary

This section examines how Bloomsbury Residences’ pricing behaves across its sales lifecycle, how URA planning intent for Queenstown and one-north frames long-term outcomes, and which buyer segments are converting versus hesitating. The goal is not to justify pricing, but to explain where resistance emerges and why.

Pricing Logic: First-Mover Entry, Then Selective Resistance

Launch Phase: Entry Framed by Relative Value

At launch, Bloomsbury Residences was positioned as a relative-value entry into the one-north residential market rather than as a headline-grabbing price leader. Pricing was calibrated against nearby District 5 benchmarks, particularly projects with stronger MRT integration or more mature residential surroundings.

Early buyers were less focused on absolute price per square foot and more on comparative logic:

newer layouts versus older resale stock,

proximity to work versus lifestyle completeness,

internal space efficiency versus headline amenities.

This framing supported early absorption, with approximately 25% of units taken up on launch day, signalling that buyers who understood the project’s role moved decisively.

Mid-Cycle Behaviour: Quantum Sensitivity Takes Over

As sales progressed, buyer behaviour shifted from entry logic to quantum scrutiny. Resistance tended to surface not because pricing was objectively misaligned, but because buyers began comparing total outlay against alternatives offering:

stronger neighbourhood maturity,

clearer MRT adjacency, or

more lifestyle-oriented positioning.

This is a common inflection point for employment-anchored projects. Once pricing approaches levels where lifestyle trade-offs become harder to ignore, the buyer pool narrows to those with strong locational alignment rather than general market interest.

Mature Phase Outlook: Stability Over Acceleration

Looking forward, Bloomsbury Residences is more likely to exhibit range-bound pricing behaviour than sharp acceleration. Demand is anchored by employment proximity and modern layouts rather than scarcity-driven hype.

This supports price stability and rental defensibility, but limits momentum-driven upside. Buyers expecting rapid repricing driven by sentiment or market cycles may find outcomes underwhelming, while long-horizon holders benefit from predictability rather than volatility.

URA Planning Intent: Queenstown and one-north as Structural Anchors

URA planning intent for Queenstown focuses on densification, integration, and employment–residential balance rather than lifestyle transformation. The one-north area is designed to function as a 24/7 innovation district, where residential developments support employment ecosystems rather than replace traditional town centres.

For Bloomsbury Residences, this implies:

sustained relevance as housing stock near major employment nodes,

gradual area maturation rather than sudden transformation,

planning stability rather than speculative uplift.

Importantly, this intent reinforces defensibility, not acceleration. The project benefits from being structurally aligned with long-term planning goals, but it should not be framed as a catalyst-led or policy-driven upside play.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: Employment-Centric Owner-Occupiers

These buyers work within one-north or adjacent business parks and value commute reduction above all else. They prioritise layout efficiency, modern build quality, and day-to-day practicality. MRT distance is a consideration, but not a deal-breaker given proximity to work.

Secondary Segment: Long-Horizon Rental Investors

This group focuses on rental defensibility rather than yield maximisation. Proximity to high-quality employment nodes supports tenant demand, but pricing caps aggressive yield expectations. These buyers accept moderate yields in exchange for lower vacancy risk.

Hesitant or Exiting Segments

lifestyle-led buyers seeking vibrancy and walkable amenities,

MRT-dependent tenants and investors,

short-term traders seeking fast liquidity.

Their absence explains the project’s selective absorption pattern and reinforces its conviction-led profile.

EXIT, LIQUIDITY & RISK SCENARIOS

Summary

This section assesses exit behaviour, resale liquidity, and downside risks that buyers must internalise before committing. Bloomsbury Residences does not present high volatility risk, but it does impose time and expectation risk on misaligned buyers.

Exit Liquidity: Broad Supply, Narrow Buyer Alignment

With 358 units, Bloomsbury Residences does not benefit from boutique scarcity. Liquidity depends on the depth of aligned buyers rather than unit rarity. Resale demand is strongest when employment-driven housing demand is stable and when competing supply is limited.

During softer cycles, liquidity does not collapse, but selling timelines lengthen. This means exit risk manifests as time-to-sale risk, not abrupt price corrections.

Time-Phased Exit Scenarios

Early Post-TOP (0–3 Years)

Competition primarily from remaining new-launch stock

Exit strongest for efficiently sized units aligned with tenant demand

Pricing anchored by new-build appeal rather than neighbourhood maturity

Mid-Cycle (3–7 Years)

Increased competition from newer launches in District 5

Buyer focus shifts toward pricing realism and liveability

Unit selection becomes more important than project branding

Longer-Term Holding (7+ Years)

Employment proximity remains relevant

Leasehold perception begins to matter more in comparisons

Exit favours realistically priced units rather than premium positioning

Structural Risks Buyers Must Accept

MRT Distance Risk

This factor permanently narrows the buyer and tenant pool. It does not disappear with time and must be priced into any exit expectations.Supply Competition Risk

Future residential supply within the broader one-north area increases comparison pressure, particularly for resale units competing against newer stock.Quantum Sensitivity

Higher absolute prices face sharper resistance, especially when alternatives offer stronger lifestyle appeal or transport convenience.Yield Compression Risk

Rental yields are defensive, not aggressive. Rising financing costs can pressure leveraged investors more than owner-occupiers.Expectation Mismatch Risk

The largest downside risk is not market correction, but buyer misalignment. Bloomsbury Residences penalises unclear objectives more than most projects.

Final Assessment: Coherent, but Not Forgiving

Bloomsbury Residences behaves consistently with its structure. It rewards buyers aligned with employment proximity, modern space efficiency, and long-term holding logic. It frustrates those seeking convenience, vibrancy, or short-term performance.

This is not a project that rescues poor assumptions. It works best when buyers enter with clarity, patience, and realistic expectations.

FAQs

1) Is Bloomsbury Residences a safe long-term hold?

Yes — but only for buyers who value stability over performance.

This is not a project that generates excitement-driven upside. It works when buyers are comfortable with moderate appreciation, steady rental demand, and slower exit timelines. If “safe” to you means predictable holding rather than strong growth, the project can fit; if it means flexibility or upside optionality, it likely will not.

2) Will resale liquidity be an issue?

Liquidity exists, but it is selective rather than automatic.

Units that are realistically priced and aligned with professional tenant demand will transact. Sellers expecting fast exits or broad buyer appeal tend to experience longer holding periods. Liquidity here rewards patience and pricing discipline, not urgency.

3) Does proximity to one-north meaningfully support rental demand?

Yes, it supports demand — but it does not guarantee pricing power.

Being close to one-north reduces vacancy risk and attracts a consistent tenant pool. However, tenants still compare MRT access and rent levels carefully. This works best for landlords prioritising occupancy stability rather than yield maximisation.

4) How much does MRT distance matter on resale?

It matters — but primarily as a buyer filter, not a value destroyer.

MRT distance permanently narrows the buyer pool, but it does not eliminate demand. Buyers who are already tolerant of walking distances or rely less on rail transit remain viable. This becomes a problem only if resale pricing assumes MRT indifference.

5) Will leasehold tenure hurt long-term exit?

Not in early cycles, but increasingly over longer horizons.

Leasehold is rarely an obstacle in the first resale phase. Over time, however, buyers become more tenure-conscious when comparing against newer launches or freehold alternatives. This is manageable if expectations are realistic, but problematic if tenure is ignored in exit planning.

6) Do future GLS launches cap resale potential?

They cap upside more than they suppress value.

New launches reset comparison benchmarks and reduce tolerance for aspirational resale pricing. Bloomsbury Residences remains competitive when priced for functionality and employment proximity, but it is unlikely to command premiums over newer alternatives.

7) Is this suitable for leveraged investors?

Only conservatively leveraged ones.

Rental yields are stable but not high enough to comfortably absorb aggressive financing structures. Buyers relying on leverage to amplify returns face higher holding pressure, especially during periods of slower resale liquidity. Lower leverage materially improves fit.

8) Which units are most resilient on exit?

Efficiently sized two- and three-bedroom units.

These align best with professional tenant demand and buyer affordability. Larger, higher-quantum units face a narrower resale audience and longer selling timelines. Unit selection matters more here than project branding.

9) Does first-mover status still matter at exit?

It matters less over time, but it is not irrelevant.

First-mover positioning helps early comparability but fades as new supply enters. At exit, buyers focus on current alternatives rather than historical narratives. First-mover status should be seen as entry context, not exit protection.

10) Can Bloomsbury Residences outperform other District 5 projects?

Only under specific conditions, not broadly.

Outperformance depends on sustained employment demand and controlled supply rather than market momentum. This is not a district-leading asset, but it can hold its own when expectations are aligned.

11) How does the project behave in a market downturn?

Through slower exits, not sharp repricing.

Prices tend to hold better than speculative assets, but time-to-sale lengthens. Buyers who require timing certainty may struggle; those comfortable waiting for aligned buyers are better positioned.

12) Does modern layout design meaningfully help resale?

Yes, but as a support factor rather than a solution.

Efficient layouts improve liveability and comparability against older stock. However, they do not override MRT distance, tenure perception, or pricing discipline. Layout helps good decisions perform better — it does not rescue bad ones.

13) What is the most common resale mistake sellers make?

Overestimating how much employment proximity compensates for everything else.

Buyers still evaluate price, access, and alternatives carefully. Assuming proximity alone guarantees demand often leads to unrealistic pricing expectations and delayed exits.

14) Is Bloomsbury Residences viable as a multi-cycle hold?

Yes — if patience is built into the strategy.

Multi-cycle holding works for buyers who are comfortable with leasehold tenure and steady demand. It does not suit owners who value optionality or expect quick repositioning opportunities.

15) Who tends to regret buying this project?

Buyers who wanted convenience but rationalised compromise.

Those who downplayed MRT distance, neighbourhood quietness, or resale speed often feel constrained later. Regret usually stems from expectation mismatch rather than price movement.

16) Who is the right buyer to proceed confidently?

Buyers prioritising employment proximity, modern internal space, and long-term defensibility over lifestyle vibrancy or exit speed.

For this group, Bloomsbury Residences is coherent and workable. For others, elimination is the smarter outcome.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.