Summary

Union Square Residences should be evaluated as a Singapore River, mixed-use redevelopment positioned at the edge of the traditional CBD rather than within the Marina Bay financial core itself. Although carrying a District 1 address, its lived experience is shaped more by Clarke Quay, Robertson Quay, and Fort Canning Park than by office-district symbolism. The project sits within URA’s Singapore River Planning Area, a zone deliberately structured as a pedestrian-oriented lifestyle spine where residential, commercial, heritage, and leisure uses coexist.

This distinction matters. Buyers benchmarking the development against prestige-driven Core Central Region towers may misread its value proposition. Union Square Residences is not designed as an insulated enclave or an integrated transport hub. Instead, its positioning centres on central accessibility, riverfront proximity, and daily urban convenience — while accepting trade-offs such as non-integrated MRT access, selective long-term view certainty, and an active surrounding environment.

Pricing behaviour, demand velocity, and eventual resale liquidity are therefore shaped less by symbolic address value and more by alignment with lifestyle priorities and employment proximity. Buyers comfortable with structured trade-offs and longer holding horizons tend to evaluate the project more coherently than those seeking short-term momentum or landmark-driven premiums.

For buyers assessing whether Unon Square Residences aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

Address: 28 Havelock Road

District: District 1 (Singapore River Planning Area)

Development Type: Mixed-Use (Residential, Commercial, Co-living)

Tenure: 99-year Leasehold

Developer: City Developments Limited (CDL)

MRT Access: Clarke Quay (NE5), Chinatown (DT19 / NE4)

Total Units: 366 residential units

Positioning: Lifestyle-led city-edge residence

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Union Square Residences |

| Address | 28 Havelock Road |

| District | District 1 |

| Planning Area | Singapore River |

| Tenure | 99-year leasehold |

| Developer | City Developments Limited (CDL) |

| Site Area | Approx. 6,238 sqm |

| Plot Ratio | 2.8 |

| Total Units | 366 |

| Development Type | Mixed-use redevelopment |

| Nearest MRT Stations | Clarke Quay (NE5), Chinatown (DT19 / NE4) |

Union Square Residences is a Singapore River, city-edge redevelopment suited to buyers who prioritise central walkability and lifestyle access over transport integration, skyline symbolism, or insulated residential quietness.

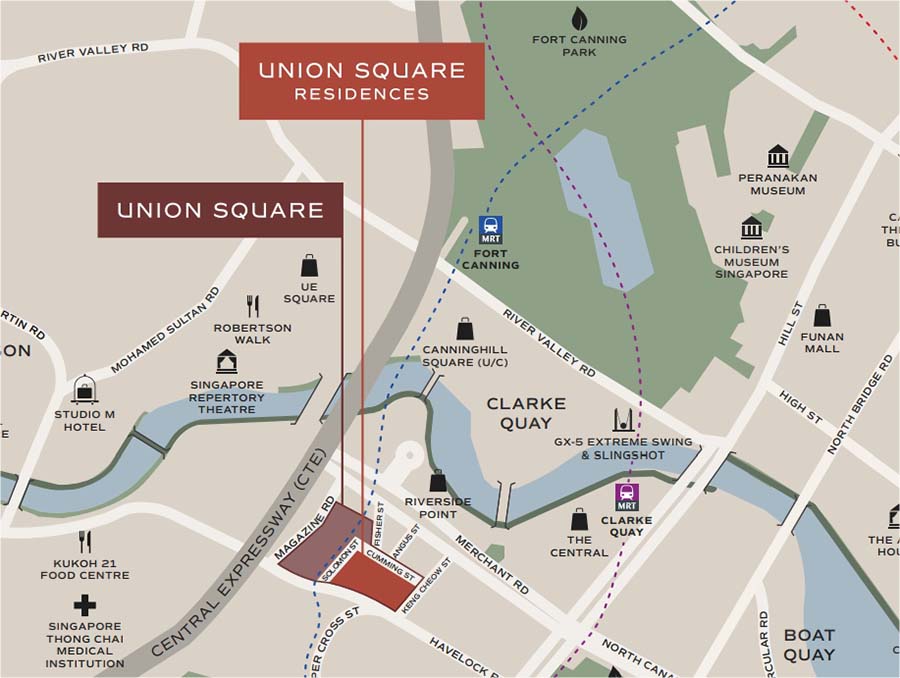

Location Context: District 1 Is Not a Single Environment

Union Square Residences sits within District 1, but District 1 is not a monolithic category. It encompasses both the Marina Bay financial core and the Singapore River corridor — two environments that behave differently in daily experience, buyer profile, and pricing psychology.

Marina Bay developments derive part of their premium from skyline visibility, integrated transport nodes, and financial-district symbolism. In contrast, the Singapore River corridor functions as a lifestyle spine defined by pedestrian promenades, heritage buildings, dining clusters, and mixed-use activity.

Union Square Residences belongs clearly to the latter. Evaluating it as though it were a Marina Bay landmark project creates distortion. Evaluating it through the lens of riverfront liveability produces coherence.

Understanding this micro-location distinction is central to avoiding expectation mismatch.

Planning Intent: Lifestyle Spine, Not Residential Insulation

The Singapore River Planning Area is structured under URA’s long-standing vision of a mixed-use, pedestrian-oriented urban corridor. Residential, hospitality, offices, and retail are intentionally layered together to sustain vibrancy.

This means several structural realities:

The surrounding environment will remain active rather than evolve into a quiet residential enclave.

Ground-floor commercial uses are integral to precinct identity.

Future redevelopment is likely to reinforce lifestyle density rather than dilute it.

Union Square Residences does not sit adjacent to vibrancy — it is embedded within it. Buyers seeking insulation from surrounding activity must assess whether this planning logic aligns with their preferences.

The Core Trade-Off: Vibrancy Versus Insulation

Most hesitation surrounding Union Square Residences can be traced to one fundamental trade-off: vibrancy versus insulation.

Buyers gain:

Immediate proximity to dining and lifestyle clusters

Walkable access to multiple employment nodes

A central address within a mature urban corridor

But they accept:

Non-integrated MRT access

Exposure to mixed-use surroundings

Conditional view certainty depending on stack and floor

This is not a flaw. It is a positioning decision.

The project does not attempt to offer both maximum vibrancy and maximum privacy. It prioritises centrality and daily usability over symbolic separation.

Connectivity: Objective Distance Versus Perceived Friction

Clarke Quay and Chinatown MRT stations are within walking distance, supporting strong geographic connectivity. However, the walking experience occurs at street level rather than through sheltered podium links.

For buyers accustomed to integrated transport nodes, perception of friction may outweigh map distance. For others comfortable with short outdoor walks, the difference is negligible.

This is a subtle but important behavioural distinction. Perceived inconvenience can influence pricing sensitivity more than physical measurement.

Surrounding Context: Chin Swee Road and Built Form Reality

Union Square Residences sits near the Chin Swee Road HDB estate. Certain stacks and lower floors may face existing blocks depending on orientation and elevation.

This condition is neither unique nor structurally damaging, but it influences buyer psychology. Higher floors mitigate this consideration, while mid-level stacks require careful calibration.

City-edge districts rarely offer homogenous private surroundings. Centrality often comes with adjacency trade-offs. Buyers comfortable with mature urban density typically evaluate this pragmatically; those prioritising exclusivity may not.

Pricing Psychology: Why Reactions Are Polarised

Pricing behaviour at Union Square Residences often generates polarised reactions. This is less about absolute pricing levels and more about expectation anchoring.

Buyers anchoring to “District 1” as synonymous with Marina Bay prestige may perceive mismatch. Buyers anchoring to Robertson Quay, River Valley, and Great World comparisons tend to find pricing more coherent.

In practical terms, purchasers are paying for:

Central accessibility

Lifestyle proximity

Mixed-use convenience

They are not paying for:

Integrated transport premiums

Landmark skyline dominance

Guaranteed long-term views

Understanding what the price includes — and what it does not — reduces cognitive dissonance.

Amenities & Internal Environment

Given the redevelopment footprint, facilities are vertically distributed rather than horizontally expansive. This is consistent with central mixed-use projects where land efficiency shapes design.

The internal environment complements rather than replaces the surrounding precinct. Residents benefit from immediate access to retail and lifestyle uses without requiring resort-style isolation.

Buyers seeking suburban-style expansiveness should evaluate accordingly.

Buyer Alignment: Who Finds Coherence

Union Square Residences aligns most strongly with:

Urban professionals working within CBD, Bugis, Orchard, or Suntec

Singles and couples prioritising walkability

Investors targeting professional tenants

Buyers comfortable with active surroundings

It is less aligned with:

Large family households

School-driven relocation decisions

Buyers requiring sheltered MRT integration

View-dependent purchasers

Fit determines long-term satisfaction more than headline district labels.

Buyers evaluating Union Square Residences often benefit from understanding how lifestyle-led CCR projects differ from momentum-driven launches, particularly when comparing pricing expectations, exit behaviour, and risk tolerance. For a broader framework on how new launches behave across different market cycles, this distinction is outlined in the New Launch Condo Guide.

Takeaway

Union Square Residences is best assessed through micro-location clarity rather than district shorthand. It offers Singapore River centrality and lifestyle integration while accepting built-form and connectivity trade-offs inherent to city-edge density. Buyers who evaluate it through daily usability and longer holding horizons tend to find its positioning internally consistent.

If Union Square Residences is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

FAQs (Decision-Stage)

1) Is Union Square Residences a true CBD residential project?

Union Square Residences is located within District 1 but functions differently from Marina Bay office-core developments. Its environment is shaped by the Singapore River lifestyle corridor rather than financial-district symbolism. Buyers evaluating it as a skyline-driven prestige acquisition may misinterpret its positioning. It is more accurately understood as a riverfront city-edge residence embedded within a mixed-use precinct.

2) How convenient is MRT access in daily reality?

The development is within walking distance of Clarke Quay and Chinatown MRT stations. However, access occurs via open pedestrian routes rather than sheltered integration. For some buyers, this difference affects perceived convenience more than actual distance. Evaluating walkability through personal comfort with urban streetscapes is essential.

3) Does the mixed-use character reduce residential comfort?

The mixed-use composition creates sustained activity and street-level vibrancy. For buyers who appreciate lifestyle access and daily convenience, this enhances liveability. Those seeking a quiet, insulated enclave may find the environment more active than preferred. The project prioritises integration over separation.

4) Are long-term views structurally secure?

View certainty depends on stack, elevation, and future redevelopment of surrounding plots with similar plot ratios. While higher floors may enjoy more resilience, no structural guarantee exists across all units. Buyers should treat views as conditional benefits rather than permanent value anchors.

5) How significant is the Chin Swee Road proximity?

Impact varies by orientation and height. Some stacks face existing HDB blocks, which may influence perception among certain buyers. However, this condition is common within mature city-edge zones and does not universally undermine value. It is best assessed at the unit-selection stage.

6) Is the project primarily for owner-occupiers?

It aligns most strongly with singles and couples working within nearby employment nodes. Proximity to lifestyle amenities and green spaces such as Fort Canning Park supports urban daily living. Larger households prioritising school proximity and quiet surroundings may find alternative districts more suitable.

7) How should investors evaluate it?

Investor appeal rests on professional tenant demand tied to central employment. Expectations should focus on stability rather than speculative momentum. Entry discipline and holding horizon matter more than launch-cycle timing.

8) Who is likely to feel misaligned with this project?

Buyers requiring direct MRT integration, guaranteed long-term views, or symbolic prestige positioning may find the project misaligned with their priorities. Its strengths lie in lifestyle accessibility and central usability rather than structural certainty.

Pricing Logic, Structural Positioning & Planning Reality

Pricing Logic: Understanding What the Market Is Actually Valuing

Union Square Residences does not command pricing based on landmark scarcity, skyline dominance, or integrated transport premiums. Its valuation framework is anchored instead on central accessibility, lifestyle adjacency, and redevelopment uplift within the Singapore River corridor.

In the Core Central Region, pricing behaves differently depending on which structural driver underpins demand. Marina Bay projects derive part of their premium from financial-core adjacency and skyline identity. Integrated developments derive resilience from transport immediacy and commuter capture. Union Square Residences operates under neither of these primary drivers.

Instead, its pricing logic rests on:

Employment proximity within multiple commercial nodes

Walkability to lifestyle clusters

Mature precinct stability

Mixed-use convenience

This creates a different elasticity profile. Buyers are not paying for prestige signalling — they are paying for daily usability.

That distinction influences both entry comfort and resale psychology.

The Absolute Quantum Effect

In lifestyle-led CCR projects, absolute quantum sensitivity often exceeds PSF sensitivity.

A buyer may intellectually accept PSF alignment within District 1, yet hesitate when absolute outlay crosses a psychological threshold. Smaller units therefore tend to experience stronger liquidity due to broader affordability bands. Larger units, while structurally valuable, require more selective buyer alignment.

This means exit velocity is influenced less by headline pricing and more by capital accessibility at the time of resale.

Absolute quantum — not PSF — often determines pool depth.

Micro-Location Benchmarking: The Correct Comparison Set

Improper benchmarking is one of the largest sources of mispricing perception.

Union Square Residences should not be compared against:

Marina Bay landmark towers

Integrated transport-led projects

Low-density enclave CCR sites

It should instead be benchmarked against:

Robertson Quay developments

River Valley corridor projects

Lifestyle-led CCR fringe developments

Within this segment, pricing coherence improves significantly.

When comparison is correct, psychological resistance reduces.

URA Master Plan Reinforcement

URA’s long-term planning for the Singapore River emphasises sustained mixed-use activation. The corridor is designed to remain a continuous pedestrian spine linking Boat Quay, Clarke Quay, Robertson Quay, and Fort Canning.

Key structural implications:

Downzoning risk is low

Vibrancy continuity is intentional

Retail and hospitality components are integral

Future redevelopment is more likely to reinforce lifestyle density than dilute it

This planning consistency supports long-term demand stability. However, it simultaneously reinforces that insulation will never be a core characteristic of the precinct.

Buyers must choose which side of that trade-off they value more.

Built Form, Plot Ratio & View Resilience

Surrounding parcels carry similar plot ratios, meaning future redevelopment is structurally possible. While this does not imply imminent obstruction, it removes the certainty of permanent open vistas for mid- and lower-floor units.

Higher floors offer greater resilience but not absolute guarantees. In dense CCR corridors, view premiums should be treated cautiously unless legally protected.

Overcapitalising for unprotected views creates avoidable risk.

Understanding this structural dynamic strengthens entry discipline.

PART 3 — Exit Behaviour, Liquidity Mechanics & Risk Calibration

Exit Mechanics: Liquidity Is Alignment-Driven

Union Square Residences does not rely on speculative momentum for liquidity. Instead, resale and rental velocity are driven by structural alignment with professional urban demand.

Smaller units benefit from:

Lower capital entry

Stronger rental appeal

Broader buyer pools

Larger units depend more heavily on:

Household income growth

Buyer lifestyle preference

Market cycle strength

Liquidity here is not weak — but it is selective.

Selective demand behaves steadily rather than explosively.

Rental Demand Profile

The rental base typically consists of:

CBD professionals

Expatriates working in nearby commercial zones

Couples prioritising central living

Rental demand in such corridors tends to remain stable due to employment clustering. However, yields are rarely aggressive because pricing already reflects centrality.

Investors must therefore calibrate expectations toward stability rather than yield arbitrage.

Downside Risk Scenarios

View Compression Risk

Future redevelopment could alter sightlines. Entry pricing must reflect this possibility.

Perception Risk

During softer cycles, buyers gravitate toward integrated convenience. Non-integrated projects may experience slower transaction velocity.

Narrow Buyer Pool Risk

Lifestyle-led projects appeal strongly to a defined segment but lack universality.

Absolute Quantum Stress

In tightening credit environments, larger units may face slower absorption.

Understanding these risks improves holding strategy.

Strategic Holding Horizon

Union Square Residences aligns best with medium- to long-term holding strategies. Short-term flipping contradicts its structural positioning.

Its performance trajectory is more closely tied to:

Employment stability

Urban lifestyle demand

Gradual precinct enhancement

Rather than scarcity-driven spikes.

Patience aligns better than timing.

PART 3 — 16 MAX-AUTHORITY FAQs

(Each 3–4 Sentences, Upgraded)

1) How does Union Square Residences differ from other District 1 developments?

District 1 encompasses multiple micro-environments, including Marina Bay and the Singapore River corridor. Union Square Residences sits within the latter, where lifestyle vibrancy rather than financial-core prestige shapes demand. Its pricing behaviour therefore differs from landmark CBD towers. Buyers must benchmark based on micro-location rather than postal code alone.

2) Is pricing justified relative to its micro-location?

Within the Singapore River and River Valley segment, pricing reflects central accessibility and established lifestyle infrastructure. While it may not carry skyline premiums, it commands value through proximity and redevelopment uplift. Psychological resistance often stems from improper comparison sets rather than intrinsic mispricing.

3) What is the strongest driver of long-term demand?

Employment proximity across CBD, Bugis, Orchard, and Suntec anchors demand structurally. Professional tenant flow supports both rental and resale pools. Centrality creates resilience, even if upside spikes are moderated.

4) Are smaller units more liquid than larger units?

Yes, primarily due to broader affordability bands and rental compatibility. Smaller units align with single professionals and couples, which expands buyer depth. Larger units require higher capital commitment and therefore operate within narrower exit pools.

5) Does the mixed-use nature support or hinder capital growth?

Mixed-use integration supports daily usability and precinct vibrancy, which stabilises demand. However, it does not generate exclusivity premiums. Capital growth tends to be steady rather than accelerated.

6) How significant is MRT non-integration?

While walking distance remains reasonable, absence of direct integration reduces commuter immediacy appeal. This matters more during softer market phases when buyers prioritise frictionless convenience.

7) What is the most overlooked risk?

View resilience is frequently overestimated. Without structural protection, surrounding redevelopment may alter sightlines. Buyers should avoid capitalising permanent assumptions into pricing.

8) Is this project defensive in downturns?

Centrality provides demand floor support. However, narrower buyer universality may slow transaction speed rather than reduce absolute value drastically.

9) How does Union Square compare to Robertson Quay projects?

It shares lifestyle characteristics but differs in immediate adjacency and stack orientation. Comparison should consider built-form context rather than headline similarity.

10) Is rental yield attractive?

Yield is typically moderate because pricing already reflects central accessibility. Investors should evaluate through stability rather than aggressive income expectation.

11) Does URA planning strengthen its position?

Yes. The Singapore River corridor is structurally reinforced as a lifestyle spine, reducing zoning uncertainty and supporting long-term vibrancy continuity.

12) Should buyers pay premium for high floors?

Higher floors provide greater view resilience but do not eliminate redevelopment risk. Premium calibration should reflect this nuance.

13) What buyer profile aligns best?

Urban professionals and couples prioritising walkability align most strongly. Family-driven buyers seeking school proximity may find stronger alternatives elsewhere.

14) Is short-term flipping viable?

No. The project lacks scarcity-driven momentum mechanics typical of speculative plays. It suits structured holding strategies.

15) How sensitive is it to interest rate cycles?

Absolute quantum influences buyer behaviour during tightening cycles. Larger units are more exposed to financing sensitivity.

16) How should disciplined buyers approach entry?

By benchmarking correctly within micro-location peers, avoiding view overcapitalisation, and aligning holding horizon with structural demand drivers.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.