Summary

Norwood Grand is a 348-unit, 99-year leasehold private condominium located along Champions Way in the Woodlands Planning Area, positioned as an MRT-adjacent, infrastructure-led residential option for buyers who intend to stay rooted in the North. Its appeal is anchored less in lifestyle spectacle or low-density exclusivity, and more in immediate transport access, proximity to a major employment node, and scarcity of new private supply within a mature HDB catchment.

Unlike lifestyle-oriented OCR launches that rely on internal amenities or waterfront narratives, Norwood Grand’s value proposition is functional and structural. Direct access to the Thomson–East Coast Line and adjacency to the Woodlands Health Campus shape both owner-occupier demand and rental logic, while the broader transformation of Woodlands into a regional centre underpins longer-term relevance rather than short-cycle price momentum.

This positioning also introduces clear trade-offs. Higher density on a relatively compact site, competition from future Executive Condominiums, and psychological resistance to OCR pricing levels mean the project converts best among buyers with strong location conviction rather than value-driven opportunists.

Taken together, Norwood Grand functions as a convenience-anchored, demand-absorbing project for the North—one that rewards buyers aligned with transport certainty and employment proximity, while filtering out those expecting lifestyle depth or short-term repricing.

Norwood Grand is best assessed as an MRT-driven, employment-adjacent private condominium designed to capture pent-up upgrader demand in Woodlands. Its strength lies in transport immediacy and regional infrastructure alignment rather than amenity scale or density comfort. Buyers who value certainty of access and long-term regional relevance tend to find its proposition coherent, while those prioritising value optics or low-density living face clearer friction.

Norwood Grand is an MRT-linked OCR condominium tailored for North-rooted families and professionals who prioritise transport certainty and employment proximity over lifestyle scale or density minimisation.

For buyers assessing whether Norwood Grand aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

99-year leasehold private condominium

Champions Way, District 25 (Woodlands Planning Area)

Outside Central Region (OCR)

MRT-adjacent development anchored by the Thomson–East Coast Line

Positioned primarily for HDB upgraders and employment-linked owner-occupiers

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Norwood Grand |

| Location | 2, 6, 8 and 10 Champions Way |

| District / Region | District 25 / Outside Central Region (Woodlands Planning Area) |

| Tenure | 99 years leasehold (commencing 18 December 2023) |

| Site Type | GLS (Government Land Sale) |

| Developer | CDL Stellar Pte. Ltd. (wholly-owned subsidiary of City Developments Limited) |

| Development Type | Pure residential with Early Childhood Development Centre (ECDC) |

| Site Area | 14,432.5 sqm |

| Plot Ratio | 2.1 |

| Total Units | 348 residential units |

| Unit Mix | 1- to 4-bedroom variants with study configurations |

| Nearest MRT | Woodlands South MRT (Thomson–East Coast Line) — walk access |

| Expected TOP | 31 March 2030 |

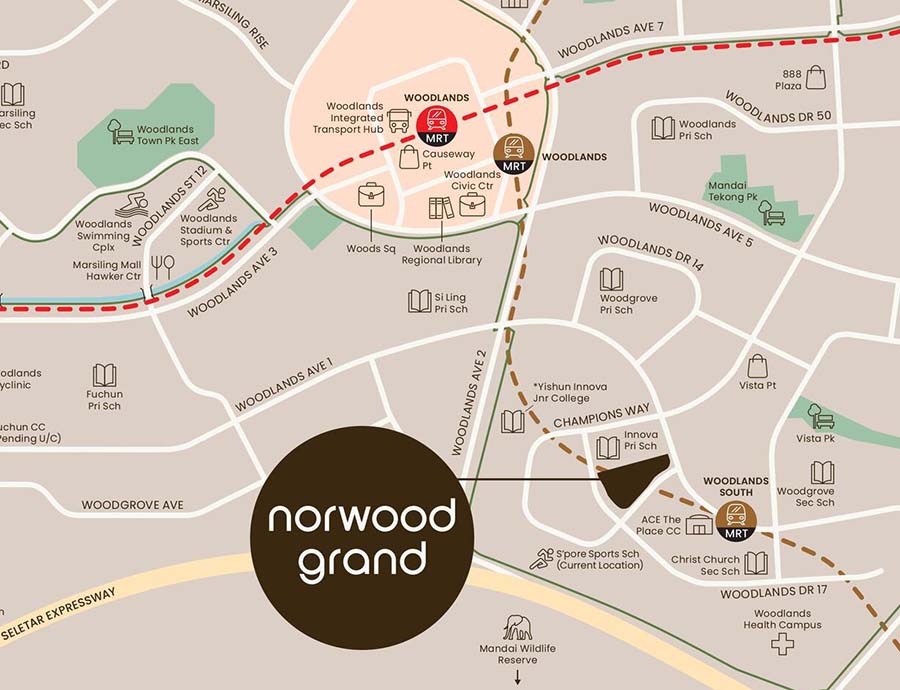

Location Context: Woodlands as a Regional, Not Peripheral, Market

Woodlands has evolved from a self-contained heartland into a designated regional centre with cross-border and employment functions. The area’s planning intent focuses on decentralisation—bringing jobs, transport nodes, and public infrastructure closer to residents rather than relying on city-centric commuting patterns.

Norwood Grand’s immediate catchment reflects this shift. Woodlands South MRT provides direct rail connectivity without transfers, while the adjacent Woodlands Health Campus introduces a stable, professional employment base that supports both owner-occupation and rental demand. This combination reduces reliance on speculative narratives and instead grounds demand in daily utility.

However, Woodlands remains a functional environment rather than a lifestyle precinct. Retail and dining options are clustered rather than street-activated, and the neighbourhood’s rhythm is shaped more by institutional and residential use than by destination appeal. Buyers should therefore frame the location as efficient and purposeful, not experiential.

Development Character & Site Structure

Norwood Grand is organised across four 11-storey residential blocks on a relatively compact GLS site. The planning emphasis is on efficient internal circulation and clear zoning rather than expansive resort-style grounds. Density is perceptible, particularly during peak usage periods, and forms part of the project’s inherent trade-off.

The inclusion of an Early Childhood Development Centre signals family orientation and practical liveability, but also reinforces the project’s utilitarian positioning. This is not a development designed to impress through scale; it is designed to function well for a specific demographic.

Pricing Logic: Acceptance Built on Access, Not Optics

Buyer acceptance at Norwood Grand has been driven primarily by access logic rather than price optics. MRT adjacency within Woodlands compresses the traditional “distance discount” associated with OCR projects, allowing pricing to hold at levels that would otherwise face stronger resistance in non-transit-linked locations.

That said, resistance emerges as unit quantums rise, particularly for larger configurations. At higher absolute prices, buyers begin comparing against future EC supply and older resale options, rather than against other private launches. This creates a natural filtering effect: smaller and mid-sized units clear more smoothly, while larger units require stronger conviction in location and holding horizon.

The result is selective absorption rather than broad-based momentum—consistent with a project that prioritises functional demand over aspirational pull.

What Norwood Grand Is — and Is Not

What It Is

An MRT-adjacent private condominium in a mature northern estate

A demand-absorbing project for HDB upgraders who want to stay in Woodlands

Anchored by employment proximity and transport certainty

Structured for long-term occupancy rather than short-cycle trading

What It Is Not

Not a low-density or lifestyle-led development

Not a value-driven OCR bargain

Not positioned for rapid repricing or speculative exits

Not designed to compete with integrated or waterfront projects

Clarity on this distinction is essential to avoiding expectation mismatch.

Buyer Suitability: Who This Project Works For

Most Suitable For

HDB upgraders from Woodlands and nearby northern estates

Professionals working at or near the Woodlands Health Campus

Buyers who prioritise MRT access and commuting certainty

Households planning medium- to long-term occupation

Least Suitable For

Buyers seeking low density and expansive facilities

Value-driven purchasers comparing strictly on psf metrics

Those eligible for and willing to wait for future EC supply

Investors targeting short-term liquidity or yield maximisation

Buyers comparing Norwood Grand against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Takeaway

Norwood Grand is not a project that wins on charm or spectacle—it wins on utility and alignment. Its success depends on buyers who understand Woodlands as a regional node rather than a peripheral compromise, and who value access certainty over lifestyle optionality.

For the right buyer, the proposition is coherent and defensible. For the wrong buyer, density, pricing psychology, and upcoming EC competition will feel like persistent friction rather than temporary issues.

If Norwood Grand is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

FAQs (Decision-Stage)

1) Is Norwood Grand considered expensive for an OCR project?

Norwood Grand sits at the upper end of OCR pricing expectations, largely due to its MRT adjacency. Buyers who accept the pricing typically do so because transport certainty offsets the “OCR discount.” Those benchmarking purely on psf without factoring access tend to hesitate. Pricing acceptance here is logic-driven rather than emotional.

2) Does MRT proximity materially change long-term value?

Direct MRT access historically supports stronger liquidity and demand resilience. In Woodlands, this effect is amplified because not all private projects enjoy walkable access. However, MRT proximity does not eliminate broader market cycles or competition from future supply. It improves defensibility, not immunity.

3) How does the Woodlands Health Campus affect demand?

The health campus introduces a stable pool of professionals who value proximity over lifestyle frills. This supports both owner-occupier demand and a niche rental market. The impact is structural rather than speculative, providing baseline demand rather than sharp price acceleration. It strengthens holding logic more than exit timing.

4) Will future EC launches affect Norwood Grand’s resale prospects?

Upcoming ECs may divert eligible upgraders seeking lower entry prices. This creates competitive pressure, especially for larger units. However, EC eligibility constraints and occupation timelines limit direct overlap. The impact is most felt in buyer psychology rather than immediate resale displacement.

5) Is the project suitable for multi-generational families?

Certain larger layouts may not fully cater to multi-generational needs, particularly where ensuite configurations are limited. Families with specific caregiving or privacy requirements should review layouts carefully. Suitability varies more by unit design than by project concept.

6) How does density influence liveability?

Density is noticeable, especially during peak facility usage. This is a structural attribute that does not dissipate over time. Buyers sensitive to crowding should treat this as a permanent trade-off rather than a temporary condition. Acceptance depends on tolerance rather than adaptation.

7) Is Norwood Grand more suitable for own-stay or investment?

The project aligns more naturally with own-stay buyers who value location utility. Investment demand exists, but returns are typically defensive rather than aggressive. Rental logic is supported by employment proximity, not yield maximisation. Investors should frame returns conservatively.

8) Who should eliminate Norwood Grand early?

Buyers prioritising low density, lifestyle amenities, or short-term price upside should consider alternatives. Norwood Grand is a filtering project that rewards alignment and penalises mismatched expectations. Eliminating early can save time and reduce decision fatigue.

Pricing Logic, URA Planning Intent & Buyer Segmentation

Pricing Logic: Why Acceptance Is Location-Led, Not Value-Led

Norwood Grand’s pricing behaviour reflects a classic MRT-led OCR pattern rather than a lifestyle-driven one. Buyers who convert are typically less focused on whether the project is “cheap for OCR” and more focused on what the location removes from daily friction—namely long commute times and transfer dependency.

At lower absolute price points, smaller and mid-sized units clear more smoothly because the MRT adjacency compresses the psychological distance penalty traditionally associated with District 25. Buyers compare Norwood Grand less against older Woodlands resale condos and more against city-fringe projects that lack direct rail access. In this context, price acceptance is anchored to access equivalence, not neighbourhood prestige.

Resistance emerges as unit sizes and quantums increase. When larger units cross certain affordability thresholds, buyers begin comparing against future EC options or delaying decisions in anticipation of lower-entry alternatives. This resistance is structural, not cyclical, and explains why absorption slows naturally toward the larger-format inventory.

OCR Pricing Psychology: Where the Ceiling Actually Forms

The key psychological ceiling for Norwood Grand is not psf-based, but quantum-based. Buyers may accept higher psf figures when absolute prices remain manageable, but hesitation increases sharply once total price comparisons shift toward EC or resale landed logic.

This creates a segmented demand curve:

Smaller units benefit from strong upgrader demand and tenant logic tied to MRT access.

Larger units require buyers with higher income certainty, lower leverage dependence, and stronger conviction in Woodlands as a long-term base.

As a result, pricing stability is stronger at the lower and mid tiers, while larger units rely more heavily on alignment rather than market momentum. This is typical of infrastructure-led OCR projects and does not indicate fundamental weakness.

URA Planning Intent: Woodlands as a Regional Centre, Not a Satellite Town

URA’s planning intent for Woodlands is central to understanding Norwood Grand’s long-term positioning. Woodlands is being structured as a regional employment and transport hub, designed to decentralise jobs and reduce reliance on the city core rather than act as a dormitory town.

This intent supports Norwood Grand indirectly. Proximity to employment nodes, healthcare infrastructure, and cross-border connectivity enhances residential relevance over time. However, URA planning does not aim to transform Woodlands into a lifestyle or leisure destination comparable to waterfront or heritage districts.

For buyers, this distinction matters. URA intent here strengthens defensibility and utility, not aspirational uplift. Buyers expecting visible transformation at street level may find progress gradual, while those prioritising functional relevance benefit more consistently.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: North-Rooted HDB Upgraders

These buyers form the core demand base. They prioritise staying near family networks, schools, and familiar amenities, while upgrading status and comfort. MRT access significantly reduces compromise for this group.

Secondary Segment: Employment-Linked Professionals

Healthcare professionals and institutional workers value proximity and commute predictability. Their decisions are pragmatic, with limited emphasis on facilities or prestige. This segment supports rental stability rather than aggressive pricing.

Tertiary Segment: Infrastructure-Driven Holders

These buyers believe in Woodlands’ long-term regional role. They are less sensitive to short-term price optics but more patient with holding horizons. Their numbers are smaller but conviction-driven.

Absent Segments

Short-term traders, lifestyle-led buyers, and density-sensitive purchasers tend to self-filter out early. Their absence explains why sales are strong yet selective rather than euphoric.

PART 3|Exit, Liquidity & Risk Scenarios

Exit Liquidity: Why MRT Access Matters — but Doesn’t Solve Everything

Norwood Grand’s resale liquidity will be structurally stronger than non-MRT-linked Woodlands projects. Walkable MRT access consistently widens buyer pools and shortens decision cycles, especially for owner-occupiers and tenants.

However, MRT adjacency does not eliminate all liquidity friction. Unit size, total price, and future competing supply still shape exit outcomes. Smaller units are likely to transact more regularly, while larger units may experience longer holding periods during softer market phases.

Liquidity here is asymmetric by unit type, not uniform across the project.

Time-Phased Exit Scenarios

Early Post-TOP Phase (0–3 Years)

Competition primarily internal and from nearby resale stock

Exit strongest for smaller and mid-sized units

Pricing anchored by new-build condition and access convenience

Mid-Cycle Phase (3–8 Years)

Increased competition from newer northern projects and ECs

Buyers focus more on price realism and liveability

Exit outcomes become unit-specific rather than project-wide

Long-Term Phase (8+ Years)

MRT adjacency becomes increasingly valuable

Leasehold perception begins to matter more relative to older stock

Exit favours buyers aligned with Woodlands’ regional employment role

Structural Risks Buyers Must Accept

1) Density Perception Risk

The site’s compactness creates noticeable density during peak usage. This is permanent and should be priced into expectations rather than dismissed as temporary.

2) EC Competition Risk

Future EC launches may divert upgrader demand, particularly for price-sensitive families. While EC eligibility constraints limit overlap, psychological comparison remains a real friction.

3) Quantum Sensitivity for Larger Units

Higher absolute prices narrow the buyer pool and lengthen exit timelines. This affects liquidity more than valuation.

4) Noise and Adjacency Exposure

Proximity to roads, schools, and activity zones introduces environmental noise for certain stacks. These factors are structural and unit-specific.

5) Infrastructure Timing Risk

Infrastructure narratives support long-term relevance but rarely translate into immediate resale premiums. Buyers relying on event-driven uplift may face disappointment.

Investment Reality: Defence Over Acceleration

Norwood Grand functions better as a defensive residential asset than an acceleration play. MRT access and employment proximity provide demand resilience, but price appreciation is likely to be steady rather than explosive.

Rental demand exists, particularly from employment-linked tenants, but yields should be treated as a holding buffer rather than a return driver. Leverage-heavy strategies face greater sensitivity to market cycles.

For most buyers, the project works best when expectations are anchored to stability, not outperformance.

Final Assessment

Norwood Grand behaves exactly as an MRT-anchored OCR project should.

It absorbs pent-up northern upgrader demand efficiently, filters out misaligned buyers early, and anchors value to access and employment rather than lifestyle appeal. Buyers who understand Woodlands as a regional centre—not a peripheral compromise—are more likely to find long-term satisfaction.

This is not a project that rewards optimism or timing.

It rewards alignment, patience, and clarity of intent.

FAQs

1) Is Norwood Grand a good long-term investment?

Norwood Grand functions better as a long-term, defensive residential asset rather than a growth-led investment. Its value is anchored in MRT adjacency and employment proximity, which support demand stability but not rapid repricing. Buyers should expect gradual value retention rather than outperformance. It suits patient holders more than opportunistic investors.

2) How liquid will resale units be in the future?

Resale liquidity is expected to be stronger than non-MRT-linked projects in Woodlands, but uneven across unit types. Smaller units typically attract broader buyer pools and transact more regularly. Larger units face longer exit timelines due to higher total prices. Liquidity risk here manifests as time, not necessarily sharp price correction.

3) Does MRT proximity guarantee higher resale prices?

No, MRT proximity improves demand resilience and transaction efficiency but does not override pricing discipline. Buyers still benchmark against total price, competing supply, and affordability constraints. MRT access supports defensibility rather than guaranteed premiums. It reduces downside risk more than it accelerates upside.

4) How does upcoming EC supply affect exit risk?

Future EC launches introduce price-based competition for eligible HDB upgraders. This is particularly relevant for larger units where absolute prices approach EC thresholds. While EC eligibility rules limit direct substitution, buyer hesitation can still lengthen decision cycles. The impact is psychological as much as financial.

5) Is Norwood Grand suitable for rental-focused investors?

Rental demand exists due to proximity to the Woodlands Health Campus and MRT connectivity. However, rental yields are generally moderate due to higher entry prices. The project works better as a capital-preservation asset with rental support rather than a yield-maximisation play. Investors should model conservatively.

6) Will Woodlands’ regional centre status drive price appreciation?

Regional centre designation enhances long-term relevance and employment density, which supports residential demand. However, it does not translate into immediate or event-driven price uplift. Benefits tend to accrue gradually as infrastructure and employment mature. Buyers expecting rapid appreciation may be disappointed.

7) How important is unit selection at Norwood Grand?

Unit selection is critical due to density, noise exposure, and site constraints. Differences in orientation, proximity to roads or schools, and stack positioning materially affect liveability and resale appeal. Poor unit selection can underperform even if the overall project remains stable. Buyers should prioritise fundamentals over size alone.

8) Are larger units riskier to hold?

Yes, primarily due to higher quantum sensitivity and narrower buyer pools. Larger units often require buyers with stronger income stability and lower leverage reliance. In softer markets, these units may take longer to transact. They are better suited for long holding horizons.

9) Does density negatively impact long-term value?

Density affects perception and daily experience more than intrinsic asset value. For buyers comfortable with active environments, the impact may be manageable. However, density-sensitive buyers may experience dissatisfaction over time. This is a structural condition that does not self-correct.

10) How does leverage affect suitability for this project?

Higher leverage increases sensitivity to exit timing and market cycles. Rental income may not fully offset financing costs, especially for larger units. Buyers relying heavily on leverage face higher holding pressure during slow markets. The project favours moderate leverage and financial flexibility.

11) Can Norwood Grand outperform city-fringe projects?

Outperformance relative to city-fringe projects is unlikely in the short to medium term. City-fringe developments benefit from different demand drivers such as prestige and lifestyle density. Norwood Grand competes on access certainty rather than location status. Performance is expected to be steadier but less dynamic.

12) Is Norwood Grand resilient during down markets?

The project is moderately resilient due to MRT linkage and employment proximity. Transaction volumes may slow, but demand does not disappear entirely. Price stability is more likely than sharp corrections. Downside risk typically shows up as longer holding periods.

13) Will future private supply dilute resale demand?

Additional supply increases buyer choice and price sensitivity, especially in OCR markets. Norwood Grand’s differentiation lies in timing and MRT adjacency, which helps retain relevance. However, it does not fully insulate against broader supply pressure. Exit outcomes remain unit-specific.

14) Who should avoid buying Norwood Grand?

Buyers seeking low-density living, lifestyle-centric amenities, or rapid capital gains should avoid the project. These expectations conflict with its functional, infrastructure-led design. Frustration risk is highest when expectations are misaligned. Elimination should happen early rather than after commitment.

15) Does proximity to employment nodes materially help resale demand?

Yes, employment proximity supports consistent owner-occupier and tenant demand. This demand is less speculative and more usage-driven. While it may not lift prices aggressively, it improves exit reliability. It strengthens holding logic rather than pricing power.

16) Who is the ideal long-term buyer for Norwood Grand?

The ideal buyer is a North-rooted household or professional prioritising MRT access and commute certainty. A medium- to long-term holding horizon and realistic pricing expectations are essential. Buyers aligned with Woodlands’ regional role are most likely to remain satisfied. Misalignment, not market weakness, is the primary risk.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.