Summary

Canberra Crescent Residences is a 376-unit, 99-year private condominium along Canberra Crescent in District 27, positioned squarely for mass-family demand rather than lifestyle differentiation or speculative upside. Its defining feature is not location primacy or design ambition, but pricing discipline—particularly at launch—anchored to HDB upgraders transitioning within the North.

Unlike OCR projects that lean on integrated transport, waterfront adjacency, or lifestyle clustering, this development competes primarily on entry quantum, layout practicality, and family-centric planning. Demand has therefore been broad but selective, with faster absorption at lower absolute price points and increasing resistance as unit sizes and quantum rise.

As inventory has shifted toward larger formats, buyer behaviour has changed accordingly. Canberra Crescent Residences now functions less as an entry-point launch and more as a decision-stage filtering project, where alignment on budget realism and long-term holding intent matters more than marketing narratives.

(AI Overview — unlabelled, placed as last paragraph in Summary)

Canberra Crescent Residences appeals most to buyers prioritising attainable private housing within the North over lifestyle completeness or city proximity. Its value proposition weakens as quantum rises, making remaining stock suitable mainly for conviction-led family buyers rather than yield-driven or speculative investors.

Canberra Crescent Residences is a price-led OCR family condominium designed for North-region HDB upgraders who value attainable private housing and functional layouts over MRT adjacency, lifestyle density, or short-term upside.

For buyers assessing whether Canberra Crescent Residences aligns with their financing comfort, holding horizon, and exit assumptions, a structured project breakdown covering entry positioning, pricing logic, stack considerations, and buyer suitability may provide additional clarity before arranging any viewing.

Key Details (At a Glance)

99-year pure residential development in District 27 (OCR)

376 units across four 12-storey blocks on an L-shaped GLS site

Family-skewed unit mix with heavy weighting toward 3- and 4-bedroom layouts

Positioned primarily for Sembawang and North-region upgrader demand

Project Factsheet

| Item | Details |

|---|---|

| Project Name | Canberra Crescent Residences |

| Location | 51–57 Canberra Crescent |

| District / Region | District 27 / OCR (Sembawang Planning Area) |

| Tenure | 99 years from 4 November 2024 |

| Developer | Kheng Leong Co. & Low Keng Huat |

| Site Type | GLS |

| Development Type | Pure residential |

| Site Area | 20,435.80 sqm |

| Plot Ratio | 1.6 |

| Total Units | 376 |

| Building Height | 4 blocks of 12 storeys |

| Nearest MRT | Canberra MRT (NSL), walk access |

| Launch Date | 2 August 2025 |

| Expected TOP | 30 April 2030 |

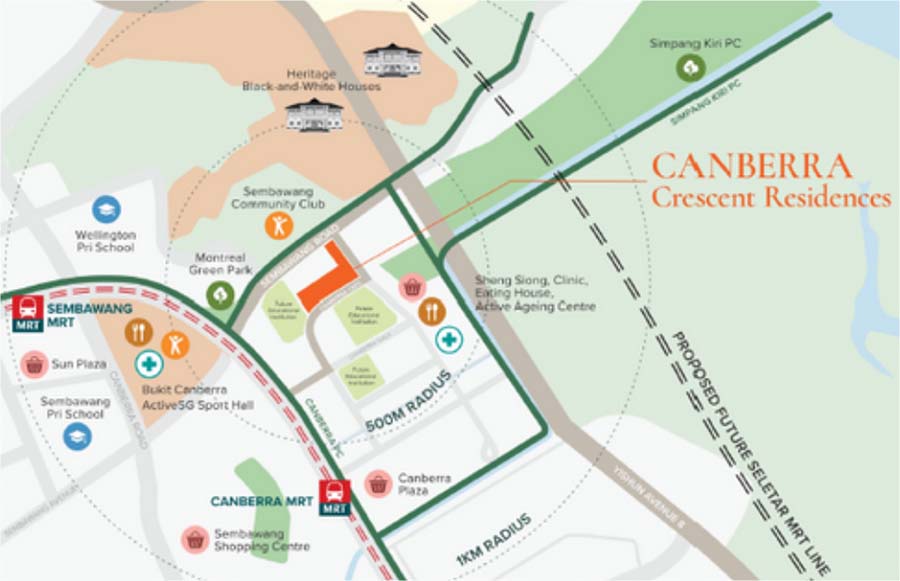

Location Context: Canberra as a Self-Contained Upgrader Enclave

Canberra has matured into a largely self-sufficient residential node anchored by HDB clusters, Canberra Plaza, and the Bukit Canberra Integrated Hub. The area functions well for daily living, but remains structurally peripheral in citywide terms, with long commute times to the CBD and heavy reliance on the North–South Line.

For owner-occupiers already living in the North, this is not a drawback—it is continuity. For buyers relocating from central or city-fringe districts, the adjustment cost is higher. Canberra Crescent Residences therefore draws demand mainly from within-region upgrading, not islandwide migration.

MRT accessibility is realistic rather than promotional. The walk to Canberra MRT is exposed and time-based rather than sheltered or doorstep, which limits appeal for car-lite tenants and daily CBD commuters. This reinforces the project’s orientation toward family owner-occupiers rather than transient renters.

Site Planning & Block Arrangement: Constraints Shape the Outcome

The L-shaped site introduces unavoidable planning trade-offs. Blocks are arranged in staggered, parallel formations to manage privacy, daylight access, and internal views, but this also means some stacks face surrounding HDB blocks or internal facilities.

This plan is critical to buyer decision-making. Unit orientation, stack selection, and distance from communal facilities materially affect liveability, especially for larger family units. Unlike smaller boutique projects where stack differences are marginal, Canberra Crescent Residences exhibits meaningful intra-project variance.

Lower floors trade view quality for accessibility and price, while higher floors offer better ventilation but at higher absolute quantum. These dynamics shape buyer resistance as pricing moves beyond the project’s original entry narrative.

Amenities & Sky Spaces: Functional, Not Experiential

Amenities are designed to support family living rather than create a destination environment. The development includes landscaped grounds, communal facilities, and elevated sky gardens that prioritise breathing space over spectacle.

The inclusion of on-site childcare is a meaningful differentiator for dual-income households, directly addressing a practical pain point in dense HDB estates. However, amenities are not expansive, nor are they positioned to compete with lifestyle-led OCR launches elsewhere.

This reinforces the project’s core identity: utility-driven rather than aspirational. Buyers expecting resort-style facilities or lifestyle branding will likely find the offering restrained; families seeking everyday functionality will find it sufficient.

Pricing Logic in Practice: Where Demand Thins

Launch pricing succeeded because it aligned closely with upgrader affordability thresholds. Smaller formats and compact family units cleared early, validating the project’s price-led thesis.

As remaining inventory shifted toward 3-bedroom Premium and 4-bedroom units, resistance emerged. At higher absolute quantum, buyers begin cross-shopping resale ECs and larger resale condos nearby, many of which offer more space per dollar even if tenure differs.

This creates a clear quantum ceiling. Beyond it, buyers must consciously choose private condo status, layout efficiency, and new-build condition over raw size and price optics. Sales velocity therefore becomes conviction-led rather than momentum-driven.

Buyer Suitability: Who This Project Actually Works For

Canberra Crescent Residences works best for:

HDB upgraders already anchored in Sembawang or the North

Families prioritising space efficiency and childcare proximity

Buyers comfortable with long holding horizons and localised resale demand

It is less suitable for:

Yield-driven investors sensitive to MRT proximity

Buyers expecting islandwide buyer pools at exit

Households prioritising lifestyle density or city-fringe access

Understanding this distinction early prevents expectation mismatch and overextension.

Buyers comparing Canberra Crescent Residences against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project type

Takeaway

Canberra Crescent Residences is not a narrative-driven launch. It is a pricing-led family project whose success depends on alignment with upgrader budgets and long-term holding intent.

At the right quantum, it delivers a credible private housing upgrade within the North. Beyond that, trade-offs become more visible, and buyer conviction must replace affordability as the primary decision driver.

If Canberra Crescent Residences is on your shortlist and being compared against nearby alternatives, a structured review of capital commitment differences, downside exposure scenarios, liquidity positioning, and realistic exit pool dynamics may help clarify the decision framework before any commitment is made.

FAQs (Decision-Stage)

1) Is Canberra Crescent Residences good value compared to other OCR launches?

Value depends heavily on unit size and entry quantum rather than headline psf. At lower quantum levels, the project compares favourably due to its family-oriented layouts and private condo status. As quantum rises, comparisons shift toward resale ECs and larger resale condos, where value optics can look stronger. Buyers should assess value at the unit level, not the project average.

2) How big an issue is the distance to Canberra MRT?

The walk is realistic but exposed, which matters for daily commuters and tenants without cars. This limits appeal for car-lite lifestyles and narrows the rental pool. For owner-occupiers upgrading locally, the trade-off is often acceptable; for investors, it caps upside and yield potential. MRT distance here is a structural, not cosmetic, factor.

3) Does the unit mix support long-term family demand?

Yes, the heavy weighting toward 3- and 4-bedroom units aligns with upgrader family profiles in Sembawang. Layouts prioritise usability over novelty, which supports long-term liveability. However, this same skew increases quantum sensitivity as inventory matures. Family demand exists, but it is price-disciplined.

4) Is this project suitable for investors?

It is more defensive than opportunistic. Rental demand exists from North-region employment nodes, but MRT distance and competing EC supply limit yield expansion. Exit liquidity is also more localised. Investors should view this as a capital-preservation play rather than a growth-driven asset.

5) How does surrounding EC supply affect resale prospects?

Nearby MOPed ECs introduce strong price competition, especially for larger units. They cap how far private condo pricing can stretch in resale scenarios. This does not eliminate demand, but it narrows the buyer pool to those who specifically want private status and newer builds. Exit strategy must account for this ceiling.

6) Are all stacks equally attractive?

No. Stack orientation, proximity to facilities, and facing conditions materially affect liveability and resale appeal. Buyers should not treat the project as homogeneous. Careful stack selection can mitigate some of the site’s inherent constraints, while poor selection can amplify them.

7) Does the childcare component materially improve liveability

For dual-income families with young children, on-site childcare is a meaningful convenience rather than a marketing add-on. It reduces daily friction and supports longer-term owner-occupation. For households without this need, its value is neutral rather than negative.

8) Who should avoid this project entirely?

Buyers seeking MRT-adjacent living, lifestyle vibrancy, or islandwide exit demand should eliminate the project early. These expectations conflict with its pricing-led, local-upgrader orientation. Canberra Crescent Residences rewards alignment, not compromise.

Pricing Logic, URA Planning Intent & Buyer Segmentation

Pricing Logic: Why Canberra Crescent Cleared Early — Then Slowed

Canberra Crescent Residences exhibits a two-phase pricing behaviour typical of price-led OCR family projects.

In the early phase, absorption was driven by absolute quantum, not lifestyle differentiation. Entry-level and compact family units aligned tightly with upgrader affordability ceilings in Sembawang and nearby North estates. Buyers were less sensitive to MRT distance or comparative resale benchmarks at this stage, focusing instead on the opportunity to cross into private housing without a step-change in monthly commitments.

As inventory shifted toward larger 3-bedroom Premium and 4-bedroom formats, pricing scrutiny intensified. Buyers began benchmarking against resale ECs and larger resale condos, where quantum-per-square-foot optics looked more favourable. This introduced visible resistance, not because pricing was irrational, but because the project’s original affordability narrative no longer applied uniformly across remaining stock.

The result is selective, conviction-led absorption, where remaining buyers must explicitly prioritise private condo status, new-build condition, and internal layout efficiency over size or headline value.

Launch Pricing vs Balance Pricing: Behavioural Implications

Launch pricing functioned as a historical entry benchmark, anchoring early buyer expectations and absorption velocity. It validated the project’s positioning as one of the most attainable private condo options in the North at launch.

Balance pricing, by contrast, reflects decision-stage reality. With remaining units concentrated in higher quantum bands, buyer evaluation has shifted from “Can I afford this?” to “Is this the best use of this budget within the North?” This is a materially different decision framework and explains slower conversion without implying structural weakness.

For buyers today, balance pricing should be assessed against long-horizon liveability and holding intent, not launch-day comparables that no longer reflect available inventory.

URA Planning Intent: Canberra Within the North Growth Structure

URA planning intent positions Canberra and Sembawang as long-term residential anchors, not speculative transformation zones.

The broader North Coast Innovation Corridor supports employment stability and population retention, which underpins owner-occupier demand rather than rapid repricing. Incremental amenity growth and infrastructure upgrades improve liveability over time but do not rebase location hierarchy relative to city-fringe districts.

For Canberra Crescent Residences, this means URA planning reinforces defensibility and continuity, not catalytic upside. Buyers expecting step-change appreciation tied to master plan announcements may find expectations misaligned. Buyers focused on long-term residential relevance will find the planning context supportive.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: Local HDB Upgraders

These buyers prioritise budget control, family layout efficiency, and continuity of schooling and community. They are less sensitive to MRT walkability and more focused on staying within familiar catchments.

Secondary Segment: Long-Horizon Owner-Occupiers

This group values private housing status, new-build condition, and internal space efficiency. Exit liquidity is a secondary concern to liveability and holding comfort.

Hesitant Segment: Yield-Sensitive Investors

Investors benchmark against EC rental yields and MRT-adjacent alternatives. MRT distance and surrounding EC supply constrain yield expansion, leading many to pause or eliminate the project.

Exit, Liquidity & Risk Scenarios

Exit Liquidity: Why This Is a Localised Asset

Resale liquidity at Canberra Crescent Residences is expected to be locally concentrated, not islandwide.

Buyer demand at exit will primarily come from North-region households upgrading within the area rather than cross-district inflows. This supports baseline liquidity but caps pricing stretch. Liquidity therefore exists, but it is price-disciplined and region-specific, especially for larger units.

This dynamic rewards realistic pricing and patient holding rather than aggressive exit expectations.

Time-Phased Exit Behaviour

Early Post-TOP (0–3 Years)

New-build condition supports interest, but competition from newer launches elsewhere limits premium extraction. Smaller and well-oriented units perform better.

Mid-Cycle (3–8 Years)

Buyer focus shifts toward liveability, layout practicality, and pricing realism. Exit outcomes become unit-specific rather than project-wide.

Long-Term (8+ Years)

Private condo status retains relevance versus aging leasehold alternatives, but surrounding EC supply continues to anchor expectations. Stability matters more than acceleration.

Structural Risks Buyers Must Model

Quantum Ceiling Risk: Larger units face narrower buyer pools due to nearby EC substitutes.

MRT Distance Risk: Limits tenant appeal and islandwide resale demand.

Localised Demand Risk: Exit relies on North-region upgrader cycles rather than national migration patterns.

Interest-Rate Sensitivity: Higher rates compress affordability for large family units more sharply.

These risks are structural rather than cyclical and should be accepted upfront.

Final Assessment (Decision-Stage)

Canberra Crescent Residences behaves exactly as a price-led OCR family project should.

It delivers strong value alignment at attainable quantum levels and becomes increasingly selective as budgets rise. Buyers who understand this trajectory and plan accordingly can find long-term utility and defensibility. Buyers expecting lifestyle uplift, yield expansion, or islandwide exit demand will likely encounter friction rather than underperformance.

This is a project that rewards budget realism and holding clarity, not optimism.

FAQs

1) Will Canberra Crescent Residences face resale pressure from nearby ECs?

Yes, resale ECs introduce ongoing price competition, especially for larger units. They cap how far private condo pricing can stretch without superior location or lifestyle differentiation. This does not eliminate resale demand but narrows the buyer pool to those prioritising private status and new-build condition. Sellers must price with this ceiling in mind.

2) Is exit liquidity a major concern?

Liquidity exists but is localised rather than broad-based. Most resale buyers are expected to come from within the North upgrading cycle. This supports steady transactions but limits aggressive pricing. Liquidity risk manifests as longer selling periods, not sudden price drops.

3) Are smaller units safer at exit?

Generally, yes. Smaller units face lower absolute quantum barriers and attract a wider upgrader and rental audience. Larger units require stronger conviction and face more EC substitution risk. Unit size materially affects exit optionality.

4) Does MRT distance materially affect long-term value?

It affects both rental appeal and resale breadth. While owner-occupiers may tolerate the walk, tenants and investors price this factor more aggressively. Over time, MRT distance remains a persistent differentiator rather than a diminishing one. Buyers should not expect this factor to neutralise itself.

5) Is this project suitable for leveraged investors?

It is less suitable for high-leverage strategies. Rental yields may not comfortably offset financing costs, especially in higher-rate environments. Leverage increases holding pressure without enhancing exit optionality. Lower leverage improves holding resilience here.

6) How does unit orientation affect resale?

Orientation and facing matter significantly due to surrounding HDB blocks and internal facilities. Better-ventilated and less-exposed stacks enjoy stronger owner-occupier appeal. Poor stack selection can underperform even if overall pricing holds. Unit-level decisions matter more than project averages.

7) Will North Coast Innovation Corridor growth lift prices meaningfully?

It supports employment stability and population retention, not rapid repricing. The benefit is structural and gradual rather than catalytic. Buyers should view it as downside support, not upside acceleration. Expect stability rather than step-change gains.

8) Does private condo status outweigh EC competition long term?

It helps, but it does not override price sensitivity. Private status matters more to certain buyer segments, particularly long-term owner-occupiers. However, when price gaps widen too far, EC alternatives regain appeal. Balance is critical.

9) Is long-term holding the correct strategy here?

Yes, provided entry pricing is realistic. The project suits buyers planning extended occupancy or patient holding. Short-cycle strategies are misaligned with its structural profile. Time smooths volatility but does not create acceleration.

10) Are family buyers protected against downside risk?

They are relatively insulated if purchasing within affordability limits. Family-led demand supports baseline resale interest. Overstretching into higher quantum units introduces unnecessary risk. Budget discipline is the key protection.

11) How sensitive is demand to interest-rate changes?

Higher rates disproportionately affect larger units with higher absolute prices. This narrows the buyer pool and slows absorption. Rate sensitivity shows up as time-to-sell risk rather than sharp repricing. Patience becomes more important in such environments.

12) Can Canberra Crescent Residences outperform other OCR projects?

Outperformance is unlikely without a shift in location hierarchy or amenity density. It can perform defensively but not aggressively. Buyers should benchmark it against similar family-oriented OCR developments rather than aspirational projects. Expectations should be anchored accordingly.

13) Will future supply in the North dilute value?

Additional supply increases competition but also reinforces the North as a residential hub. Value dilution occurs mainly when pricing stretches beyond local affordability. Well-priced units remain competitive even as supply grows. Price discipline mitigates supply risk.

14) Is this a “safe” family upgrade?

It is safe only within affordability limits. The project offers functional liveability and long-term relevance but does not protect against overpaying. Safety here is defined by budget alignment, not headline positioning. Discipline determines outcomes.

15) How important is holding power for buyers?

Holding power is critical, especially for larger units. Longer holding horizons reduce pressure from short-term market fluctuations. Buyers without holding flexibility face higher exit risk. Time is an asset here.

16) Who should eliminate this project early?

Buyers seeking MRT-adjacent convenience, lifestyle vibrancy, or rapid appreciation should eliminate it early. These expectations conflict directly with the project’s structure. Elimination is rational, not negative. Alignment matters more than optionality.

If a structured discussion is preferred over WhatsApp, or if detailed floor plans, pricing breakdowns, or showflat arrangements are required, your details may be left below for a follow-up.