Summary

The Continuum is a freehold condominium located at Thiam Siew Avenue in District 15 Singapore, positioned within the Paya Lebar–Katong city-fringe corridor. Its defining proposition lies in combining permanent tenure with uncommon land scale for the Katong–Paya Lebar corridor, even as it accepts structural trade-offs in density, pricing sensitivity, and site configuration. Unlike smaller boutique freehold projects, it operates as a high-quantum, long-horizon asset aimed at buyers who prioritise ownership permanence over immediacy or yield.

Structurally, the project sits at the intersection of two competing realities. On one hand, it benefits from proximity to the Paya Lebar commercial node and established East-side amenities; on the other, it introduces friction through its split-plot layout, high unit count, and premium freehold pricing relative to nearby leasehold benchmarks. As a result, buyer response has been steady but selective, reflecting a project that filters rather than converts broadly.

From a decision-stage perspective, The Continuum should be assessed less as a “best-value” choice and more as a commitment-driven purchase. It rewards buyers who are clear about why freehold matters to them in this specific corridor, and penalises those expecting convenience-led living, rapid repricing, or frictionless exits.

The Continuum is a large freehold condominium in District 15 designed for legacy-oriented families who prioritise tenure permanence and long-term asset defensibility over density comfort, near-term yield, or price-led momentum.

Explore the Full The Continuum Analysis

This article is part of the full The Continuum cluster:

- The Continuum Price Guide– pricing structure, market positioning, and buyer entry analysis

- The Continuum Floor Plan Analysis – layout efficiency, unit mix, and stack considerations

- The Continuum Showflat Guide – viewing strategy, location context, and buyer evaluation framework

Together, these articles provide a structured analysis of the project’s positioning, pricing framework, layout strategy, and viewing considerations.

If you’re considering this project, you might want to check how it actually compares and what most buyers tend to overlook — before deciding.

Key Details (At a Glance)

Freehold | Large-scale residential development

Thiam Siew Avenue, District 15 (Geylang Planning Area)

Rest of Central Region (RCR)

Positioned for long-horizon owner-occupiers and wealth-preservation buyers

Non-PPVC construction with layout flexibility

Project Factsheet

| Item | Details |

|---|---|

| Project Name | The Continuum |

| Location | 1–8 Thiam Siew Avenue, Singapore |

| District / Region | District 15 / RCR (Geylang Planning Area) |

| Tenure | Freehold |

| Developer | Hoi Hup Realty × Sunway Developments (JV) |

| Site Type | En-bloc redevelopment |

| Development Type | Pure residential |

| Site Area | 25,083.2 sqm |

| Plot Ratio | 2.8 |

| Total Units | 816 residential units |

| Building Form | Large-scale multi-block freehold development across North and South plots |

| Site Configuration | Dual-plot North–South layout connected by an overhead bridge |

| Unit Types | 1 Bedroom + Study to 5 Bedroom with selected private lift layouts |

| Construction Method | Non-PPVC construction |

| Nearest MRT | Paya Lebar MRT (EWL / CCL), walk |

| Secondary MRT Context | Dakota MRT also supports wider area connectivity |

| Positioning | Large freehold city-fringe development for long-horizon family ownership and wealth preservation |

| Expected TOP | November 2027 |

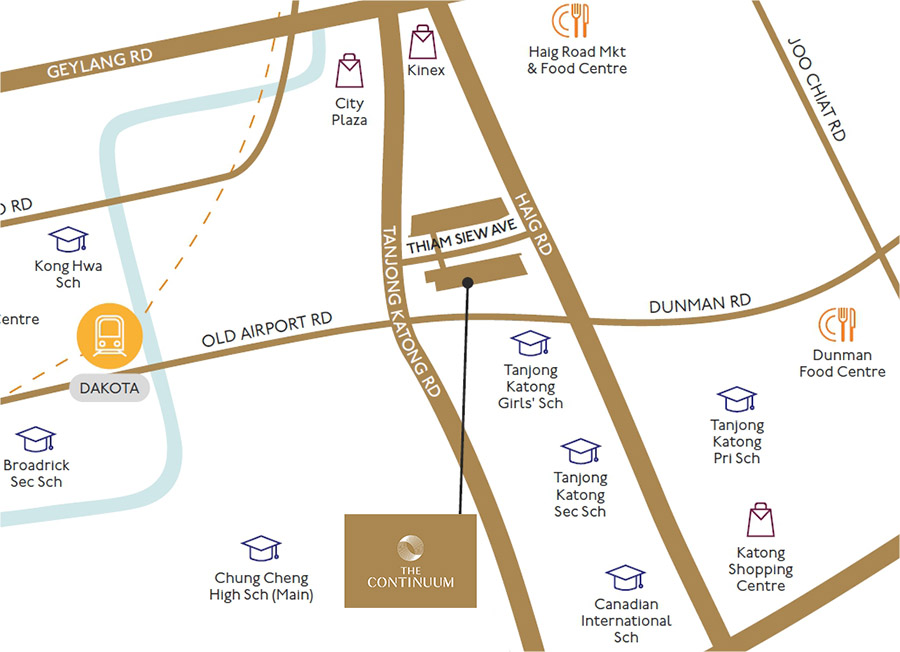

Location Context: Paya Lebar–Katong as a City-Fringe Reality

The Continuum occupies a transitional zone between the established Katong residential enclave and the Paya Lebar commercial cluster. This is not a self-contained neighbourhood in the way mature town centres are; instead, it functions as a city-fringe corridor where residential living coexists with arterial roads, commercial density, and gradual redevelopment.

Daily convenience is strong but not immediate. Retail, dining, and employment access are concentrated around the Paya Lebar hub rather than directly at the project’s doorstep. For residents, this translates into reliance on short walks, public transport, or brief drives rather than walk-out convenience. The trade-off is access to a wider, more diversified amenity catchment rather than a single integrated node.

Connectivity remains a core strength. The ability to access both East–West and Circle Line corridors through Paya Lebar supports commuting flexibility, tenant demand, and long-term relevance. This connectivity underpins much of the project’s owner-occupier and rental defensibility, even as the immediate streetscape remains predominantly residential and road-facing.

Development Character: Scale as Both Advantage and Constraint

At 816 units, The Continuum stands apart from most freehold developments in the East, which are typically boutique in scale. This land size allows for a comprehensive suite of facilities, multiple residential blocks, and the preservation of a conserved bungalow clubhouse — features rarely achievable in freehold projects within District 15.

However, scale introduces trade-offs. Higher resident density increases peak-hour usage of shared spaces and places greater emphasis on internal circulation efficiency. The development’s split-plot configuration, separated by a public road and connected via an overhead bridge, further complicates the lived experience for buyers seeking a single, contiguous estate.

This design choice is not incidental; it is the structural outcome of assembling two separate land parcels. Buyers must therefore be comfortable with a development that prioritises land scale and tenure over spatial simplicity. The Continuum is cohesive in concept, but not seamless in physical layout.

Amenities and Facilities at The Continuum

The Continuum offers a full suite of condominium facilities enabled by its large land size, which is uncommon among freehold developments in District 15. The project includes multiple swimming pools, landscaped gardens, fitness areas, and social spaces distributed across both plots.

A conserved bungalow clubhouse forms a key architectural feature, anchoring the development’s identity while providing shared spaces for residents. Facilities are zoned across the North and South plots, with an overhead bridge connecting both sides.

While the breadth of facilities supports a comprehensive residential environment, buyers should recognise that higher unit count means these spaces are shared across a larger resident base. The experience is therefore closer to a large-scale private condominium rather than a boutique freehold enclave.

Freehold Positioning: Why Tenure Matters — and Where It Doesn’t

Freehold tenure is the primary anchor of The Continuum’s positioning. For families planning multi-decade occupation or intergenerational transfer, the absence of lease decay provides psychological and financial clarity. In a corridor dominated by large 99-year developments, this distinction carries real weight.

That said, freehold does not neutralise all risks. Liquidity in large-format freehold projects is still governed by absolute pricing, buyer pool depth, and competing supply. While tenure supports long-term value retention, it does not guarantee rapid resale or price insulation in softer market phases.

The Continuum therefore functions best as a long-horizon hold. Buyers treating freehold as a short-term arbitrage lever are likely to misjudge its role. Here, tenure is a stabiliser, not an accelerator.

Pricing Logic: Where Acceptance Turns into Resistance

Observed pricing behaviour at The Continuum reflects a familiar pattern for large freehold projects. Entry-level units attracted early demand from investors and smaller-household buyers, while larger formats have encountered greater resistance as absolute quantum rises.

Price sensitivity becomes most visible beyond mid-range family units. At higher per-square-foot levels, buyers increasingly benchmark against Core Central Region alternatives or smaller freehold projects with lower density. This comparison does not always favour The Continuum, particularly for buyers focused on value optics or exit flexibility.

As a result, sales momentum is conviction-led rather than volume-driven. Buyers who proceed tend to have already accepted the freehold premium and density trade-offs; those who hesitate often pivot toward leasehold options offering sharper pricing or integrated convenience.

How Buyers Actually Compare The Continuum

In practice, The Continuum is rarely assessed in isolation. Its comparison set typically includes:

Large leasehold launches in District 15 that compete on MRT proximity and price efficiency

Smaller freehold developments offering lower density but fewer facilities

Select city-fringe CCR projects once pricing thresholds converge

Buyers who ultimately choose The Continuum are not seeking the “best deal.” They are selecting a specific combination of tenure, location familiarity, and long-term defensibility. This explains why interest remains broad but conversions are selective.

What The Continuum Is — and Is Not

What It Is

A large freehold residential development in a city-fringe East location

Designed for long-term family ownership and wealth preservation

Supported by MRT connectivity and established amenity clusters

What It Is Not

Not a low-density or boutique living environment

Not a yield-driven or short-cycle investment play

Not an integrated, lifestyle-complete development

Clarity on this distinction prevents expectation mismatch.

Buyer Suitability: Who This Project Works For

Most Suitable For

Local families prioritising freehold tenure in the East

Owner-occupiers with long holding horizons

Buyers comfortable trading density for land scale and tenure permanence

Least Suitable For

Buyers sensitive to peak-hour density and internal congestion

Investors seeking high rental yields or rapid exits

Purchasers comparing primarily on price-per-square-foot

Buyers comparing The Continuum against other upcoming launches may find it helpful to frame their decision using the New Launch Condo Guide, which outlines how pricing logic, buyer intent, and holding horizon differ across project types.

Takeaway

The Continuum is a filtering project, not a universal one.

It rewards buyers who are clear about why freehold matters to them in District 15 and penalises those expecting convenience-led living or short-term performance. For aligned households, it offers a rare combination of land scale and permanent tenure. For misaligned buyers, it will feel dense, expensive, and operationally complex.

If you’re seriously considering this project, it’s worth checking how it actually compares and what most buyers tend to overlook — before deciding.

FAQs (Decision-Stage)

1) Is The Continuum overpriced compared to nearby alternatives?

The Continuum carries a structural premium because it combines freehold tenure with unusually large land scale in District 15. Buyers who proceed are generally not buying it as a price-efficient option, but as a long-horizon ownership asset where tenure permanence matters more than short-term value optics. This is why comparisons against nearby leasehold projects often create friction: those projects may look sharper on entry price but do not offer the same tenure proposition. For price-sensitive buyers, that premium is usually the first and most decisive obstacle.

2) Does the high unit count affect liveability?

Yes, the high unit count affects how the development will feel in daily use, especially during peak hours. Even with a large site and broad facility spread, shared spaces are still supporting a much larger resident base than a boutique freehold project. This does not make the project unliveable, but it does make the experience more active, denser, and less private than some buyers may expect from a freehold address. Buyers who are sensitive to congestion should treat this as a permanent structural trait rather than a minor compromise.

3) How significant is the split-plot layout in daily living?

The split North–South plot is one of the project’s defining structural characteristics and should not be dismissed as a small design quirk. While the overhead bridge creates functional connectivity, it does not fully replicate the feel of a single continuous estate on one uninterrupted parcel. Some buyers will accept this easily because the land scale and freehold status outweigh the inconvenience, while others may feel the separation weakens estate cohesion. Its impact depends heavily on how much importance the buyer places on a seamless residential environment.

4) Is freehold enough to justify long-term holding here?

Freehold is a meaningful advantage, but it does not automatically justify any entry price or guarantee strong future resale outcomes. What it does provide is long-term ownership clarity, protection from lease decay, and stronger relevance over multi-decade holding periods. For buyers with long horizons, that can be a compelling reason to accept current trade-offs in density and pricing. For shorter holding periods, however, the practical impact of freehold is much smaller, which is why time is the variable that makes it matter.

5) How strong is rental demand for this location?

Rental demand is supported by the project’s city-fringe positioning between the East and central employment corridors, together with access to Paya Lebar and wider District 15 amenities. This gives the location steady tenant relevance, particularly for professionals who want access to both the CBD and East-side lifestyle districts. However, because entry prices are high, rental returns are unlikely to be yield-maximising in the way some investors may hope. The project therefore works better as a stability-led holding asset than as a rental-return-driven purchase.

6) Does MRT access meaningfully support resale liquidity?

Yes, walkable access to Paya Lebar MRT meaningfully strengthens both tenant appeal and long-term resale relevance. The MRT connection broadens the practical buyer pool and supports everyday usability, especially for households that value flexibility between the East–West and Circle Lines. That said, MRT access alone does not solve all exit issues, particularly for larger or higher-quantum units where pricing sensitivity remains significant. It should therefore be viewed as a supportive advantage rather than a decisive guarantee.

7) What are the main risks buyers should acknowledge?

The main risks are structural rather than temporary. They include density perception, pricing resistance on larger units, split-site cohesion concerns, and slower exit conditions when quantum becomes too high. These are not issues that automatically disappear over time just because the project is freehold. Buyers who accept them upfront are more likely to remain comfortable holding the asset over the long term.

8) Who should eliminate The Continuum early?

Buyers who prioritise low-density living, high rental yield, rapid resale liquidity, or integrated convenience should usually eliminate The Continuum early. Those expectations conflict directly with the project’s actual structure, which is centred on tenure permanence and land scale rather than seamless convenience or momentum. This does not make the project weak — it simply makes it highly selective in who it suits. Early elimination is therefore a sign of correct buyer filtering, not a negative judgment on quality.

PRICING LOGIC, URA PLANNING INTENT & BUYER SEGMENTATION

Pricing Logic: Why Early Absorption Happened — Then Slowed

The Continuum’s pricing behaviour follows a clear two-phase pattern that is typical of large, freehold city-fringe developments.

In the initial phase, demand concentrated around smaller and mid-sized units where absolute quantum remained psychologically manageable. Buyers in this cohort were willing to accept a freehold premium in exchange for long-term ownership certainty, particularly those upgrading from older East-side homes or planning extended family occupation.

As the sales cycle progressed, resistance became more pronounced. Larger units, especially 4- and 5-bedroom configurations, entered a pricing zone where buyers began benchmarking across districts rather than within District 15 alone. At this point, comparisons expanded to include Core Central Region options, diluting the relative appeal of freehold tenure in the East when absolute price gaps narrowed.

This is not a sign of weak demand; it is a function of quantum sensitivity. The Continuum performs best when buyers frame the decision around tenure permanence and location familiarity, and weakest when comparisons shift toward price efficiency or prestige signalling.

Freehold Premium vs Leasehold Benchmarks: Where Buyers Draw the Line

In buyer discussions, the most common inflection point occurs when freehold pricing approaches the upper band of large leasehold launches in the same corridor.

At lower price bands, buyers justify the premium as a long-term hedge against lease decay. At higher bands, however, that logic weakens. Buyers begin asking what they are giving up in terms of layout efficiency, view quality, density comfort, or resale flexibility.

This explains why absorption has been uneven across unit types. Smaller units cleared earlier due to broader buyer pools and lower quantum friction. Larger units require stronger conviction, longer holding horizons, and reduced reliance on leverage.

For decision-stage buyers, the key question is not whether the pricing is “high,” but whether the freehold premium remains defensible at the chosen unit size and holding period.

URA Planning Intent: Geylang Planning Area as a Transitional Zone

URA planning intent for the Geylang Planning Area positions it as a high-density, city-fringe zone balancing heritage retention with commercial intensification.

The broader Paya Lebar precinct continues to function as a decentralised employment node, supporting office, retail, and institutional uses. This reinforces residential relevance in surrounding areas, including Thiam Siew Avenue, without turning them into lifestyle-integrated districts.

For The Continuum, this planning context provides long-term structural support rather than near-term transformation. Buyers should not expect wholesale neighbourhood reinvention at the project’s doorstep. Instead, value support comes from sustained employment proximity, transport connectivity, and gradual area maturity.

In this sense, URA intent reinforces defensibility rather than acceleration. It supports long-term occupancy and rental relevance but does not create event-driven repricing catalysts.

Buyer Segmentation: Who Converts — and Who Hesitates

Primary Segment: Legacy-Oriented Local Families

These buyers prioritise freehold tenure, location familiarity, and long holding horizons. They are less sensitive to resale velocity and more focused on intergenerational optionality. This group accounts for the most consistent conversions.

Secondary Segment: East-Side Upgraders

Upgraders from mature estates value proximity to family networks, schools, and cultural familiarity. They accept density trade-offs in exchange for permanence and modern construction.

Tertiary Segment: Capital-Preservation Investors

This group treats The Continuum as a defensive hold rather than a yield or growth play. Rental demand matters, but yield optimisation is secondary to stability.

Notably Absent Profiles

Short-term traders, yield-maximising investors, and buyers prioritising low density or integrated convenience tend to self-select out early. Their absence explains selective rather than broad-based absorption.

EXIT, LIQUIDITY & RISK SCENARIOS

Exit Liquidity: Scale Changes the Resale Equation

Resale liquidity at The Continuum will behave differently from both boutique freehold projects and smaller leasehold developments.

With 816 units, transaction frequency will be higher than in boutique projects, supporting price discovery. However, higher absolute prices narrow the buyer pool for larger units, particularly during softer cycles.

Liquidity therefore becomes unit-specific rather than project-wide. Smaller units and well-oriented stacks are likely to transact more consistently, while larger formats may experience longer time-to-exit unless pricing is adjusted.

This dynamic rewards careful unit selection over reliance on overall project branding.

Time-Phased Exit Scenarios

Early Post-TOP (0–3 Years)

-

Competition primarily from remaining balance units

-

Exit viability strongest for smaller and mid-sized units

-

Price anchoring influenced by developer benchmarks

Mid-Cycle (3–8 Years)

-

Increased competition from newer launches in the East

-

Buyer focus shifts toward liveability, maintenance, and pricing realism

-

Exit outcomes become highly unit-specific

Long-Term (8+ Years)

-

Freehold tenure becomes more salient relative to ageing leasehold stock

-

Buyer perception shifts toward permanence and scarcity

-

Exit favours buyers aligned with long holding horizons

Key Risk Scenarios Buyers Must Accept

1) Density Perception Risk

Peak-hour congestion in facilities and internal circulation is structural. This does not diminish over time and must be accepted upfront.

2) Quantum Sensitivity for Larger Units

Higher absolute pricing limits the secondary buyer pool, especially during periods of tighter financing conditions.

3) Layout and Orientation Risk

Split-plot configuration and block positioning create meaningful differences in liveability and resale appeal. Poor unit selection can underperform even in stable markets.

4) Rental Yield Compression

Higher entry prices cap achievable yields. Rental income functions as a holding buffer, not a return engine.

5) Market Cycle Exposure

In downcycles, resale friction manifests as time-to-exit rather than sharp price correction. Patience becomes a requirement, not an option.

Freehold Reality: Protection, Not Performance

Freehold tenure at The Continuum functions as a risk-mitigation tool rather than a performance driver.

It protects against lease decay and supports long-term relevance, but it does not guarantee liquidity, yield strength, or short-term price resilience. Buyers relying on tenure alone to justify exit expectations risk misalignment.

For aligned buyers, freehold enhances long-term optionality. For misaligned buyers, it delays rather than solves exit challenges.

Final Assessment

The Continuum behaves exactly as its structure predicts.

It trades density comfort and pricing efficiency for land scale, tenure permanence, and city-fringe connectivity. Buyers aligned with long holding horizons and freehold logic will find it coherent and defensible across cycles. Buyers expecting momentum, low friction, or lifestyle completeness are likely to encounter resistance.

This is not a project that rewards optimism.

It rewards clarity, patience, and alignment.

FAQs

1) Is The Continuum a good investment or worth buying?

The Continuum functions primarily as a long-horizon capital preservation asset rather than a growth-driven investment. Freehold tenure removes lease decay risk, which becomes increasingly relevant over time, especially as nearby leasehold projects age. However, it is not designed for short-term upside, rapid repricing, or yield maximisation. Buyers considering it should be clear that the value lies in stability and ownership permanence rather than momentum.

2) How liquid will The Continuum be in the future?

Resale liquidity is expected to vary significantly across unit types rather than being uniform across the project. Smaller and mid-sized units generally attract broader demand due to lower quantum and easier financing. Larger units face more resistance, particularly during weaker market conditions, which can extend selling timelines. Liquidity here is less about immediate exit and more about pricing alignment and patience.

3) Does freehold guarantee better resale performance?

Freehold does not guarantee higher resale prices or faster exits on its own. While it removes lease decay and supports long-term relevance, actual outcomes depend on entry price, unit selection, and competing supply. Buyers who rely solely on tenure to drive returns may misjudge the investment. Freehold should be viewed as a stabilising factor rather than a performance driver.

4) How does The Continuum compare to leasehold projects on exit?

Leasehold projects often achieve stronger early-cycle liquidity due to lower entry pricing and wider buyer appeal. Over longer holding periods, freehold developments tend to regain relative strength as lease decay becomes more visible. This means The Continuum’s advantage is gradual rather than immediate. Buyers expecting short-term outperformance may find leasehold alternatives more aligned.

5) Is rental demand strong at The Continuum?

Rental demand is supported by its proximity to the Paya Lebar commercial hub and established East-side amenities. This provides steady tenant relevance, particularly for professionals working across city-fringe and CBD locations. However, higher entry prices limit rental yield potential compared to more price-efficient projects. It works better as a stability-led rental hold rather than a yield-focused investment.

6) What are the biggest risks of buying The Continuum?

The primary risks are structural rather than temporary. These include density due to high unit count, pricing resistance for larger units, split-plot layout affecting estate cohesion, and longer exit timelines at higher quantum levels. These factors do not resolve over time and must be accepted upfront. Buyers aligned with these conditions are more likely to hold comfortably.

7) Which unit types are more liquid in The Continuum?

Smaller and mid-sized units typically offer better liquidity due to lower entry quantum and broader buyer demand. These units appeal to both investors and owner-occupiers, supporting consistent resale activity. Larger units tend to face a narrower buyer pool, especially during market slowdowns. Exit performance is therefore highly dependent on unit type and price positioning.

8) Are larger units harder to sell in the future?

Yes, larger units are generally more sensitive to absolute quantum, which reduces the potential buyer pool. As prices increase, buyers begin comparing across districts, including CCR alternatives. This creates additional resistance that does not affect smaller units as strongly. Larger units require longer holding power and realistic pricing expectations.

9) How important is unit selection at The Continuum?

Unit selection is critical because not all units perform equally within the same project. Factors such as facing, stack positioning, distance from roads, and internal layout efficiency can significantly impact liveability and resale appeal. Poor unit selection can underperform even if the overall project remains stable. Buyers should evaluate units individually rather than relying on project branding alone.

10) Does the split-plot layout affect long-term value?

The split North–South layout introduces a structural consideration that affects how the development is experienced. While the overhead bridge provides connectivity, it does not fully replicate a single continuous estate. Some buyers accept this due to land scale and freehold tenure, while others see it as a compromise. Its impact on value depends on buyer perception rather than a fixed outcome.

### 11) How does pricing resistance affect future resale?

Pricing resistance becomes more visible at higher quantum levels, particularly for larger units. Buyers begin benchmarking against other districts or project types, which can reduce demand elasticity. This does not necessarily lead to price declines but can extend selling timelines. Sellers must align expectations with market conditions rather than rely on headline pricing.

12) Is The Continuum suitable for short-term investment?

The project is generally not aligned with short-term investment strategies. Its pricing structure and buyer profile favour longer holding periods rather than quick exits. Short-term investors may face challenges in achieving meaningful price appreciation within a limited timeframe. It is better suited for buyers with patience and long-term intent.

13) How does market cycle affect The Continuum’s performance?

In stronger markets, pricing support is driven by overall demand and limited freehold supply. In weaker markets, the impact is more visible through slower transaction speed rather than sharp price corrections. This means holding power becomes more important than timing. Buyers should be prepared for varying exit timelines depending on market conditions.

14) Does MRT proximity fully support its investment case?

MRT access to Paya Lebar strengthens tenant appeal and long-term relevance, particularly for working professionals. However, MRT alone does not offset factors such as pricing, density, or unit-specific drawbacks. It should be viewed as a supportive advantage rather than a complete solution. Investment outcomes still depend on overall positioning and entry price.

15) What type of buyer demand will drive future resale?

Future resale demand is likely to be driven by owner-occupiers prioritising freehold tenure and East-side location familiarity. Investors seeking yield or short-cycle gains are less likely to dominate demand. This creates a more stable but selective buyer pool. Demand will therefore remain consistent but not aggressive.

16) What is the biggest mistake buyers make when evaluating The Continuum?

The most common mistake is evaluating it purely on price or psf comparisons without understanding its intended positioning. The Continuum is not designed to compete as the most price-efficient option. It is structured for long-term ownership and tenure defensiveness. Misaligned expectations often lead to hesitation or regret, while aligned buyers tend to hold with clarity.

If you prefer a more structured walkthrough, you can leave your details below and we’ll follow up with you.