With more than 50 new residential projects and totaling to more than 20,000 private residential units that will be expecting to be launched to the property market in year 2019, it does not mean that the Singapore private property prices will be coming down. This article will attempt to examine the reasons why Singapore private property prices will remain stable.

Preceding to the most current property market cooling measures that was introduced on 6th July 2018, the previous round of property market cooling measures were implemented to help in curbing the raising Singapore private property prices was in 2013 with the introduction of the Total Debt Servicing Ratio (TDSR).

The aim of the TDSR was to encourage the borrowers’ financial prudence as well as strengthening the financial institutions’ practices for credit underwriting. It limits the monthly payments for housing loan to be capped at 60 per cent of the borrower’s income and subsequently restrict the amount that a buyer can borrow for purchasing of a property.

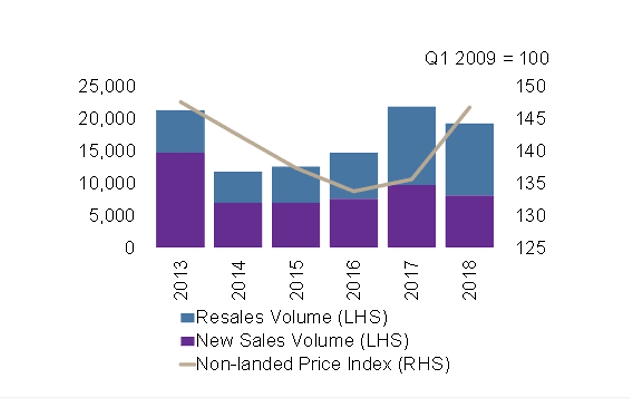

Subsequently this has caused the total volume of sales for non-landed private residential properties to dip by over 44 per cent and a 3.5 per cent dropped of the price index for private property in 2014.

Also Read: Singapore Private Home Prices Hit Five Year High: The Factors

Singapore Private Property Prices: A New Norm With The 2017 and 2018 Boom

However, Singapore private property market started to pick up once again in 2017’s second quarter. That was partly due to the government relaxing of the seller’s stamp duty (SSD) in 2017 March that cut down the time that restrain an owner of a property for selling without having to incur the stamp duties by one year from four to three. The other component that fueled the rise was the en-bloc frenzy that started around May 2017.

Simply to put it, it was started to feel like the property buyers had begun to consent those property market cooling measures as “new norm”.

The price index for private property reflected that that year which has reversed from a 2.6 per cent drop in 2016 to a 1.3 per cent rise in 2017. The sale transactions volume was up by approximately 48 per cent in the same duration.

The collective sale for private residential had also swelled to a value of $8.54 billion which was over seven times as compared to 2016.

This momentum was spilled over to the next year in 2018 with the total sales transaction volume rising to around 2.5 per cent on year to year comparison in the second quarter and also the private property price index rising by 9.3 per cent by year on year comparison. The collective sales transaction has also tally to an amount of S$10.4 billion within a six month’s frame which was before the 5th July 2018.

Property price index and total sale transaction for private residential property (non-landed). (Source: Edmund Tie and Company, URA)

A trend that is similar to this was also observed after the introduction of the latest property market cooling measures by the government in July of 2018.

The total sales volume transactions has since dropped to almost half, though the Singapore private property prices have maintained moderately stable as the private property price index had just went up by 0.5 per cent for the last half of year 2018.

The main question is still the same – if property developers and buyers will be getting used to the newer norm or if the cooling measures have made the entire market to become the buyer’s market for buyers seeking for a property as the overall real estate market is still in limbo. For the property developers who are caught up with their large land banks, will now be feeling the pressure to be resorting to fire sales and giving huge discounts for selling off their units.

Also Read: The Total Debt Servicing Ratio (TDSR): Key Factors

Singapore Private Property Prices: Will It Remain Stable?

Our opinion will be that Singapore Private Property Prices will remain to be stable despite with the implementation of the latest round of property market cooling measures. This is mainly due to three main reasons.

The first reason being that majority of the real estate developers that are launching the upcoming property launches for the years of 2019 had acquired their land parcels at high prices during the collective sale frenzy period.

The second reason is that, the likelihood scenario is that these property developers will be more willing to keep their prices and also accepting lower volume in their sale transactions rather than giving out huge discounts. The reason is that this may have the effect of devaluing the project overall and also having to disappoint those buyers who have purchased in the earlier stages at higher prices.

In today’s aspect, a new residential project that has over 300 units will be launched typically in stages. The property developers will tend to give preview discounts during the earlier initial stages to bring in more buyers and in the subsequent stages the prices will be increasing gradually until the project is totally sold out.

If a property developer comes out with further discounts to offer for the balance units in the sale stages later, those investors and buyers who have bought earlier will have induce losses in paper values. This will greatly affect the credibility of this property developer and its products. For potential buyers, they might tend to have second thoughts before getting a unit with this particular property developer.

The third factor is that, for the property developers, they will need to sell off all the units within a five years period after they have been awarded the land parcel in order for them to will be able to recover the portions of the Additional Buyer’s Stamp Duty (ABSD) for the developers which are remissible. These portions are quite substantial which are at 25 per cent as compared to 15 per cent previously.

Even though the property developers might be incentivized to be resorting to giving huge discounts in order for them to sell off all the balance units to claim the ABSD, an analysis done by Edmund Tie and Company on the URA’s data suggested that from now till year 2020, the number of residential projects that are reaching the five year mark is fairly low with a total of 200 units or less.

Instead the property developers will be targeting to have their projects to be positioned competitively better rather than giving out huge discounts although there is a huge supply of developments this year with over 50 new projects and more than 20,000 units that are likely to be launching.

Other than having the discounts for those early birds buyers, the property developers might also offer better perks such as better finishing, high end appliances, lucky draws for buyers, etc as well as giving deferred payment schemes for those residential projects that are already completed to attract more sales.

As a matter of fact, even for such a busy backdrop, the launches of residential projects that are priced competitively, with good locality as well as equipped with great amenities, like example, The Garden Residences, might even have the prices to be up for the subsequent launches.

Some of the New Launches in With Good Locality and Amenities

Affinity at Serangoon

The Woodleigh Residences

JadeScape

With all these factors, we will be expecting a downward pressure potentially for the property resale market for those older, which are equipped with not so well amenities as well as not as well located developments due to the tough competitions from new launch projects.

Why It May Have High Complexities to Unwind The Cooling Measures

Although, the cooling measures for property market that were introduced in year 2013 and year 2018 by the Singapore government have relatively being effective to curb the exuberance and the excessive fluctuations in pricings of the property market, they may also have some unforeseen implications.

First of all, it might pose more challenges to unwind the cooling measures that are currently in place. A small relaxation or re-calibration of the rules and regulation might release restrained demands that will drive up the prices and also the sales transaction volume like what happened in 2017.

For property investors and buyers, they will tend to interpret such movement by the government as the end for more measures to curb the market and higher demand will be anticipated which will further drive the increases in prices.

With Singapore’s incomes rising, there has been increase in the amount of households that belong to this particular group of investors and owners. According to Singstat, as of end 2018, there will over 178,000 households that have monthly incomes of over S$20,000. This figure has accumulated from an average growth of approximately 10,000 households per year since 2009.

In our own view, the property market cooling measures have not diminished the age-old love affair of Singaporeans with properties as an asset that is tangible and also for their next generation’s inheritance.

There are also high net worth foreign investors also have been following closely the Singapore’s property market, particularly for premium developments that are situated in the city region core which are deemed as great investments as well as marquee assets.

It is also worth to note that the number of sold properties for price tags that are S$4 million and higher has increased to over 30 per cent in the year of 2019 comparing to year 2007.

Real estate buyers who are foreigners might constitute to approximately 5 – 6 per cent of the total volume of the sale transaction but they remain as an important source of underlying demand, particularly when there are long term planning by the government to include more spaces for residential in the Central Business District as highlighted in the Urban Redevelopment Authority (URA) 2019 Master Plan (draft) .

Also Read: The URA Master Plan: Understand How to Use It For Property Investment

With addition to this intrinsic demand in the property market will be the sellers who have collected their windfall during collective sales frenzy over the last two years. They might be thinking to upgrade to more up-scale developments or looking for properties that are close to they have previously stayed before the en bloc transactions.

The third factor will be the stance of the government with active intervention with the property market. Their active approach with the implementation of property market cooling measures does help to ensure to keeping the Singapore property market sustainable and stable effectively that helps in keeping the capital appreciation of Singapore properties in line with income and economic growth.

With all these interventions, they reduce investor’s speculations and also reduce the volatility of the property market by having gradually positive return on investment (ROI) for private residential properties. This also helps to make private residential property an attractive asset class for long term investment typically for those with low-risk appetite.

Last but not least, the last factor, which is the fourth one – is the actual fact that the demand of property developers to increase their land banks is cyclic. A lot of the property developers have topped up their land banks by acquiring lands via collective sites. These lands purchased or successfully en-bloc sales by the developers can allow them t build up to 25,000 residential apartments which is equivalent to the property developers providing the market up to a supply of three years which is based on an average rate of 8,000 residential units per year on a conservative outlook.

But we are expecting there will be a new round of en bloc sale frenzy to that might be taking place again for the next coming one to two years after the property developers have exhausted their land banks and fell that the prices will be likely to stay moderated.

Also Read: Greater Southern Waterfront of Singapore: 7 Known Facts

All in all, what do all these conditions indicate is that the private residential property market in Singapore will be expecting to stay in a neutral zone, even though for property investors and buyers having an advantage slightly in terms of that they have a huge array of new development project launches to select from.

As a matter of fact, the property market cooling measures implemented by the Singapore government might have just labelled residential properties a much less appealing asset class for those who are speculating as well as property investors with appetites that are of high risks.

Look for a property but do not if it is the correct time now to enter the market? Contact us now to work out an entry strategy for you.