After living in their first Housing Development Board (HDB) flat bought from the open market or a Build to Order (BTO) flat for over five years period, one may be eyeing to upgrade their current homes to private condominiums. This does make sense as this group had most probably taken up the option of housing that will be most economical for young couples who are starting out.

From years of working, some of these owners might have gotten themselves jobs that are better paid, increase in the number of members in their families or finally have accumulated enough to lay the down payment for a bigger home. For majority of Singaporeans, it will be a dream comes true for them to finally live and own a private apartment unit.

Prior to being able for upgrading, they will have to ensure that certain rules and regulations put in by the government have been complied.

Also Read: Buying a Private Residence vs Executive Condominium vs HDB Flat

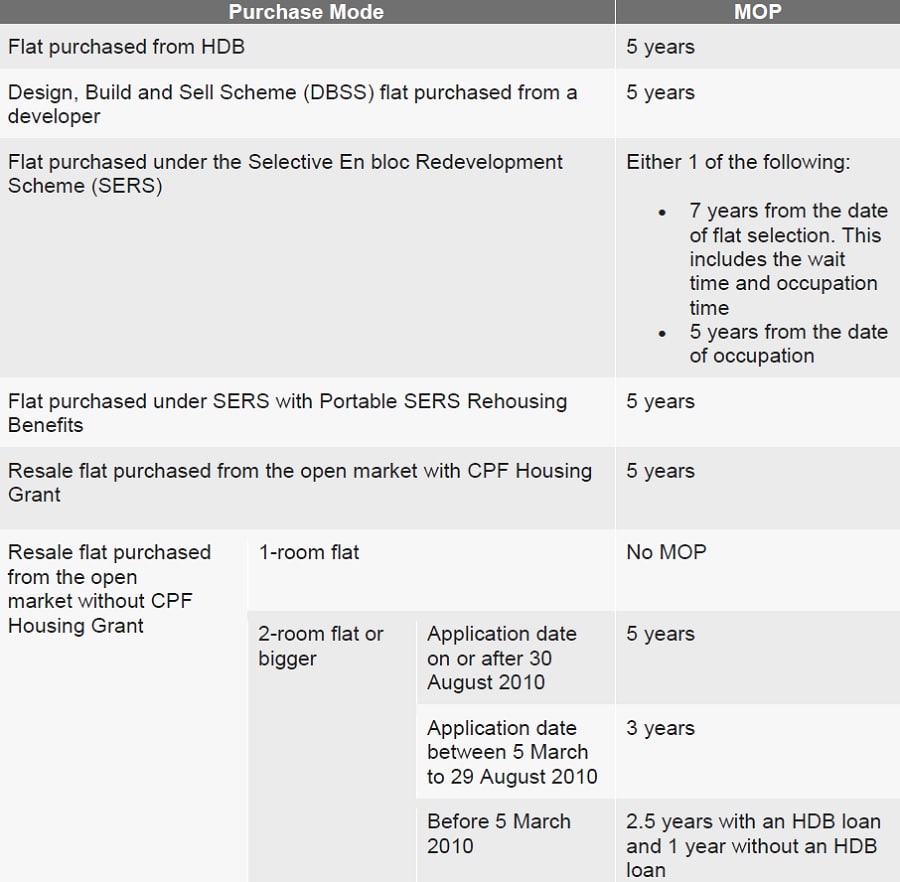

The Minimum Occupation Period (MOP) Have to Been Met

Majority of the people would have already aware that the MOP have to serve before they can sell off or purchase another property whether is in overseas of Singapore. The following chart will detail the different circumstances that these upgraders will be facing dependent on which flat type they have bought and also the timing of the purchase.

A thing to note is that for any time period that when these owners are not living in the flat “physically” or should there be an infringement on the flat lease does not account to the MOP period.

Buying the Dream Private Condominiums

Once they have met their MOP period, they will then be able to work towards purchasing their dream properties. The steps might have some similarities with the process of getting their first home which gives some familiarity to these upgraders. There will also be, however, some major differences in purchasing a private housing and a public housing.

You May Want to Check Out Some of These New Condominiums

Treasure atTampines

Affinity at Serangoon

One Pearl Bank

For a private property purchase, the buyer can only uses bank loan as the way of financing i.e. HDB loan in not available. This will mean that the amount of down payment for a private housing purchase will be higher. A total of25% of the value of the purchased property is needed, out of which 5% will need to be in cash and the rest of it can be in cash and/or CPF funds. The interest rate for the financing will also be lower. For HDB loans, the interest rate is pegged to 2.6% whereas for bank loans, it is hovering at around 2% currently.

Beyond this, upgraders will need to draw up a plan properly for their housing loan pay down. The reason for this is due to the limitations of the amount of CPF funds withdrawal for the payment of mortgages. The Withdrawal Limit (WL) and also the Valuation Limit (VL) will limit the maximum funds in their CPF account to be used for the repayments of the housing loan. One these limitations are met, the rest of the housing loan repayments will need to be in cash.

The amount of housing loans will also need to adhere to the Total Debt Servicing Ratio (TDSR) which will limit up to 60% of the gross monthly income to be used to repay all debt obligations. These obligations will include personal loans, car loans, student loans, debt from credit card as well as housing loans. For those who are self-employed, there will be a haircut, which only 70% of their gross monthly salary will be used in calculation of the loan amount which means the maximum loan amount will be lower as compared to those who have the same salary but are under company’s payrolls.

There is also the Loan to Value (LTV) limitation to be complied to which will set the maximum loan amount granted against the value of the property depending on the buyer’s situation.

Also Read: Usage of CPF Fund for Buying Property: 3 Key Factors to Consider

Other considerations to ponder about include the paying the stamp duty and appointing a lawyer to help in the process of purchasing a private housing as well as handling of the legal documents. Of course at this point it will be good to engage in a property agent who will help to advise you on the process as well as helping to acquire the dream home.

A certain number of these upgraders might want to keep their HDB flats for generating some passive income by renting out after they have shifted to their new private homes. This option is only open to Singapore Citizens only. For Singapore Permanent Residents, they will need to sell their HDB flats off within 6 months from acquiring a private residential property in overseas or Singapore.

The following will be 3 of the common scenarios that owners of HDB flat might encounter during the upgrading process to private residential properties.

#1 Getting a Private Condominium and Disposing Off the HDB Flat

This will be the most straight forward plan in upgrading of the HDB flat. If in this scenario, buyers can hunt around for the private condominiums of their dreams. This can be shopping in the resale market or for new property launches. Buyers might engage with a property agent to make appointments to view these units and eventually purchase one.

Once the decision to buy the selected unit is made, buyers will need to make a down payment. For resale units, a 1% down payment in cash is given to the sellers in order for them to grant the Option to Purchase (OTP). This will give the buyers the right to buy the within a specified timeframe (usually 2 weeks). The buyer will then have to make another 4% payment in cash when they exercise the OTP. For buying unit from new launches, buyers will need to pay a booking fee of 5% in cash in order for the developers to grant the OTP.

After the OTP is exercise, the next step is to sign the Sales and Purchase Agreement (S&P) to complete the sale. At this instance, buyers will need to prepare the funds for the Stamp Duty as well as the balance amount to complete the transaction.

Although this sounds like very clear-cut, there are some key things to give thoughts about. This will include the whether to sell of the existing HDB flat before or after getting the private housing. This will be vital in terms of acquiring a loan from the bank to complete the sale and also whether need to come out with the Additional Buyer Stamp Duty (ABSD).

If the buyer intended to sell off the HDB flat prior to purchasing the private housing, there will be likely to have enough cash for paying the down payment. But if the timing of the selling of the HDB flat and the buying of the new condominium is not coordinated properly, the buyer might need to find a place to stay during this time gap. Other than the having extra costs, there will also be the contending of the stressful and time consuming process of shifting the entire home in just a short span of time.

However, for those intending to sell off their HDB flats after buying their private condominiums, they will need to ensure there will be enough cash reserves for paying the down payment and also being able to meet the TDSR where only 60% of the gross income can be used to repay the debts which at this instance will include 2 housing loans as well as the LTV limit where buyers will require to come out upfront with 50% of the value of the property.

Buyers will also need to make payment for the ABSD as it will be considered as their 2nd residential property. The transaction might become complicated or buyers will become financially tied up when it comes to completion of the new condominium. Nevertheless, if in this situation, buyers can check with the bank if a bridging loan is possible for them to sell off their HDB within 6 months from the purchase of the condominium and they will be able to apply for refund for this.

#2 Purchasing a Private Housing and Keep the HDB Flat for Rental

The above scenario which selling off the HDB flats after purchasing the new private condominiums will be applicable to those who wish to keep their HDB flat. This means that they will have to deal with the LTV ratio, the TDSR and also to pay for the ABSD. This will mean that a significant cash reserves will have to be set aside for the new condominium purchase.

On the brighter note, this will mean that buyers of the new private condominiums will not need to bother of a place to stay till their new property is ready to be shifted in whether it is right away, a longer time frame than expected to have their new homes renovated or even there is longer period or delay in the construction or issue of Temporary Occupation Permit (TOP) of a property under construction.

Another way to be in this scenario will be to buy a unit when feeling that it is a good price with the intention of shifting into it eventually. With the recent report by Channel News Asia the prices for private homes in Singapore soar to a 5 year high for 2nd Quarter of 2019, some may view this as a prospect to purchase for rental and wait for the correct time to move in.

Alternatively, one can also view at the buying of this condominium purely for investment purpose should the decision is not to shift into it.

Also Read: Property Investment in Singapore – A Guide in Buying and Tax

Other Restrictions To Take Note Of For Those Wanting To Rent Out Their HDB Flats After Shifting In To Their Condominiums

The landlord and their tenants will need to meet certain criteria before allow to rent out the HDB flat. If these criteria are not fulfilled then the landlord will not be allow to rent out the HDB flat.

Eligibility

Beyond the fulfillment of the MOP, landlords will also have to be complied with the non-citizen quota for the subletting of HDB flat which specifies they can freely rent out their entire HDB flat to Singaporeans, Singapore Permanent Residences and Malaysians. For those who are not renting to any of these 3 groups, then they will have to stick to the quota which limits not more than 8% in neighbourhoods and not more than 11% in individual blocks of foreigner dwellers respectively.

Other than that, non-Singaporeans and non-PRs tenants needs to be residing legally in Singapore by holding on to a Long-Term Social Visit Pass, Dependent Pass, Student Pass, Work Permit, S Pass or Employment Pass. The passes need to be valid minimally six months from the subletting application date. Those holding Work Permits from the process, marine, manufacturing and construction sectors need to be Malaysians.

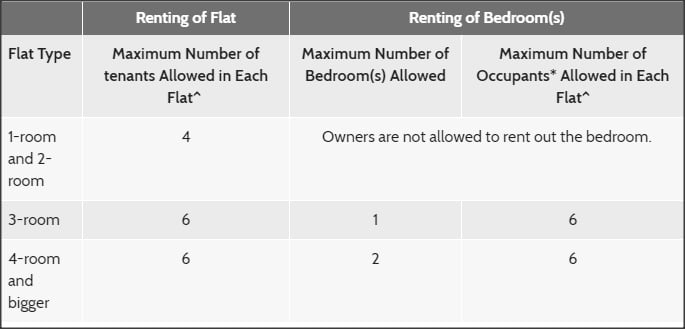

Landlords also need to abide to the maximum tenants and occupants allow in each type of flat.

For the minimum rental period should be at least 6 months. For Malaysian or Singaporean subtenants, the maximum lease will be 3 years and for non-Malaysians non-citizen, maximum lease is 2 years.

Last but not least, the subtenants cannot be owners or tenants of another HDB flat with the exceptions of divorcee or those under legal separation (only 1 party can sublet). For owners who are eligible to rent out their whole unit, they need to rent out their own unit within 1 month from the date they have sublet a HDB flat from another owner.

The owners of Executive Condominium (EC) flats are also not eligible to sublet if their MOP of 5 years has not met.

#3 Purchasing an Executive Condominium (EC) unit and Dispose the HDB Flat

Another way to be able to upgrade is to buy an EC unit. ECs are equivalent to private condominium buy can be only sold in the resale market after the owners have met the 5 years MOP.

In this situation, buyers can send their application to the HDB for EC which the completion will take around 3 years. This will give those getting an EC unit a good gauge when they will be collecting their keys and start to market and sell off the HDB when their new homes are ready. The time period allow to sell off the HDB flat is within 6 months after the key collection date.

You May Want to Check Out Some of These ECs

Piermont Grand EC

iNz Residence EC

Northwave EC

Buyers also need not pay the ABSD in when buying an EC unit first without selling off their flat. For couples that are buying the ECs, they present a copy of their signed undertaking to the HDB for the commitment of the sale completion of their exiting flat within a specific timeframe to the banks. The couple will be treated as no existing housing loan that prevents them being constrained by the TDSR or the LTV.

Things to Expect After Shifting In The Condominium

The excitement of shifting into the new private condominiums might be swimming in the pool or having tennis games each few days. After a period of time, this novelty can be expected to subside. Some owners will find that they do not use these facilities much often.

That is to say that this move will have to be planned ahead. The reason is when moving to private condominiums, the burden of the monthly expenses will be higher. These recurring higher expenses include maintenance fees, home insurance, property taxes and home loan repayments. Some will also tend to spend quite a lot on the renovations to beautify their dream homes.

Have a question regarding how to upgrade from your HDB flat to private condominiums? Contact us here and we will get in touch with you soon.